Advertisement

- United Kingdom

- /

- Wireless Telecom

- /

- LSE:VOD

Does Vodafone’s 39.7% Rally Signal More Upside for the Telecom Giant in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

How Has Vodafone Been Performing Lately?

Vodafone Group has quietly staged a notable share price recovery, and those returns are exactly why investors are starting to ask whether the current price still represents value or if most of the upside has already been captured. Before looking at the numbers, it helps to understand how the stock has behaved over different time frames.

Over the past year, Vodafone shares have delivered a gain of 39.7%, with most of that momentum building more recently. The stock is up 1.1% over the last week and 10.0% over the past month, contributing to a 38.4% rise year to date. This marks a strong turnaround compared with its 5.7% gain over five years.

This performance suggests the market is beginning to reassess Vodafone, potentially reflecting changing expectations around its strategy, capital allocation, and portfolio of assets. The key question for investors now is whether this rerating is justified by fundamentals or if sentiment has run ahead of reality.

The rest of this article will examine Vodafone's valuation from several angles, including discounted cash flow, multiples versus peers, and a breakdown of its intrinsic value drivers. It will also hint at a more narrative-driven way of understanding valuation that we will return to at the end.

Find out why Vodafone Group's 39.7% return over the last year is lagging behind its peers.

Approach 1: Vodafone Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and then discounting those back to a present value. For Vodafone Group, the model used is a 2 Stage Free Cash Flow to Equity approach, which focuses on cash available to shareholders after necessary reinvestment and debt servicing.

Vodafone generated trailing twelve month free cash flow of about €7.7 billion, providing a base for projections. Analyst estimates, supplemented by Simply Wall St extrapolations beyond the usual five year horizon, suggest free cash flow moderates to around €3.3 billion by 2030 as growth normalizes. Each of these future yearly figures is discounted back to today to account for risk and the time value of money.

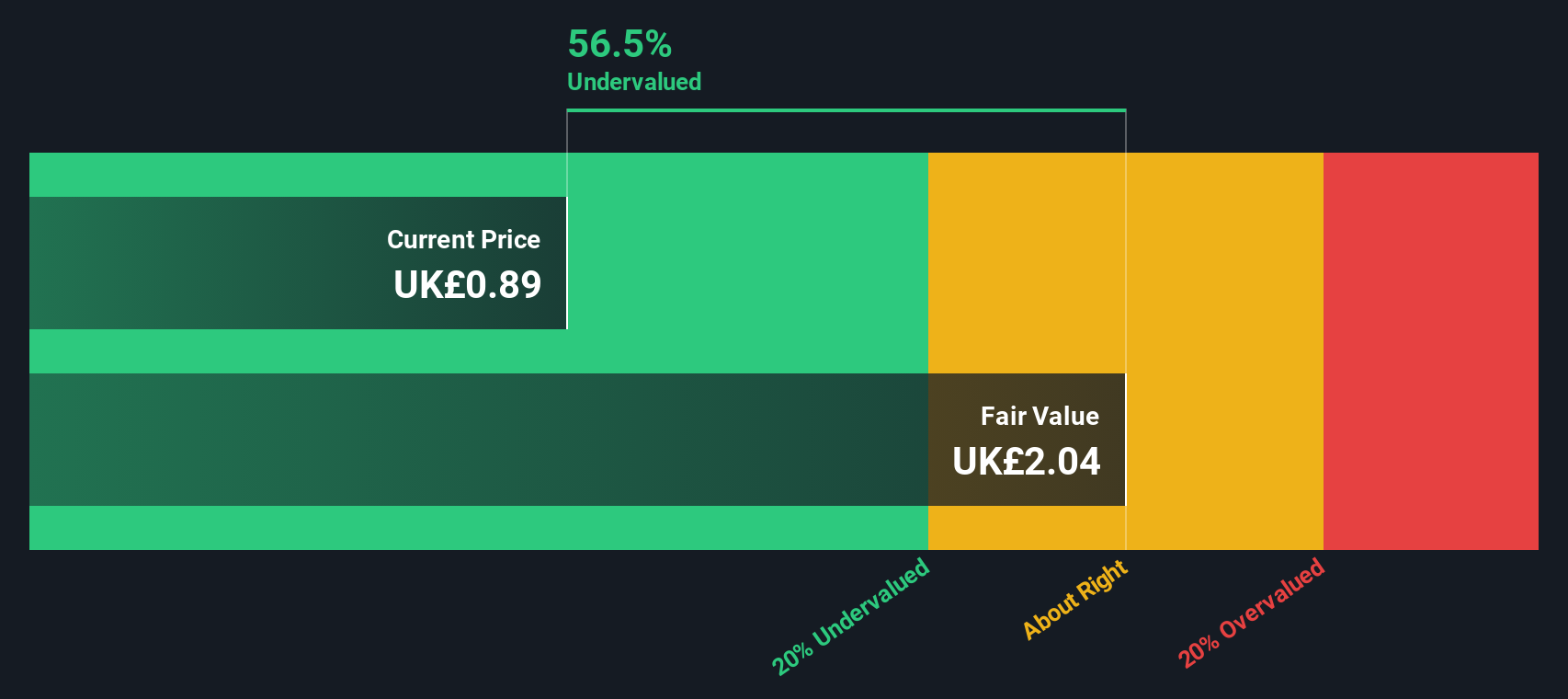

Putting those projections together, the model arrives at an intrinsic value of roughly €2.32 per share. Compared with the current market price, this implies Vodafone trades at around a 59.0% discount to its estimated fair value. This indicates potential upside if the cash flow assumptions prove broadly accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vodafone Group is undervalued by 59.0%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Vodafone Group Price vs Sales

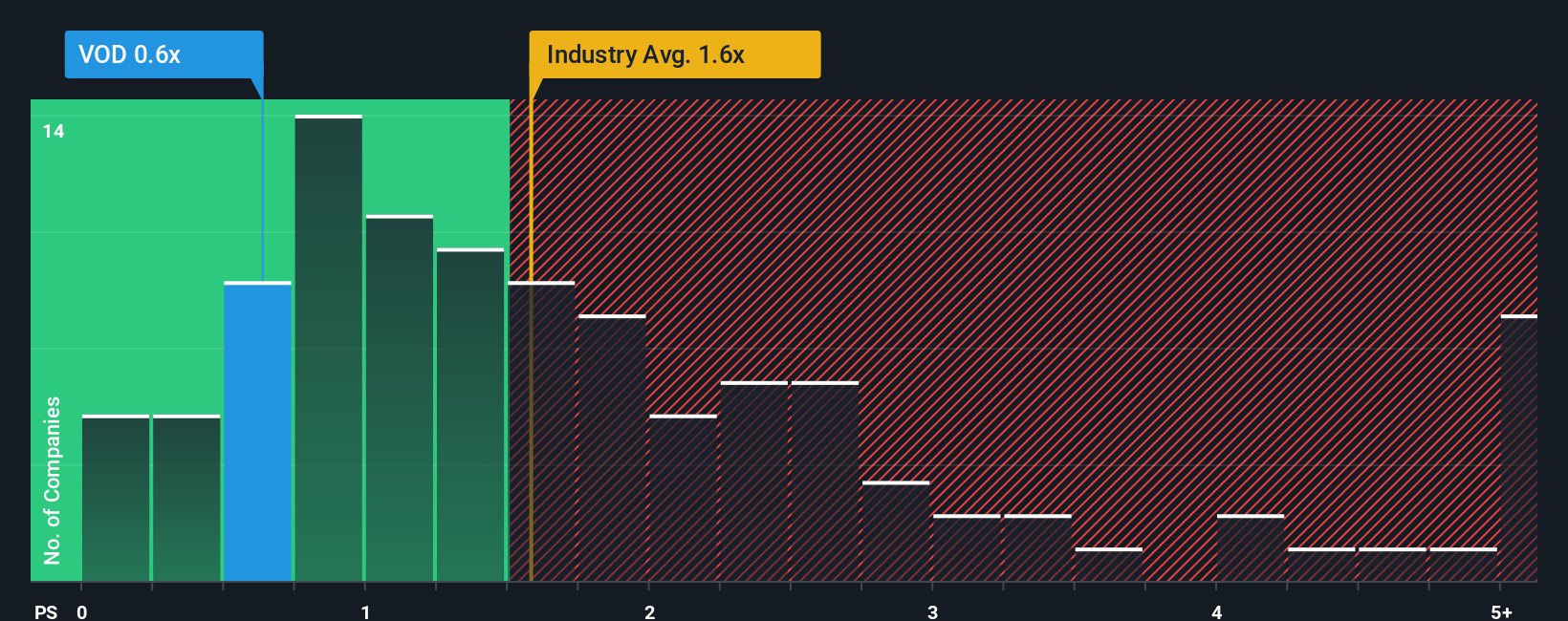

For companies like Vodafone that are in capital intensive, often lower margin industries, the price to sales multiple is a useful way to cut through accounting noise and focus on how much investors are paying for each unit of revenue. While earnings can swing with restructuring charges or depreciation, sales tend to be more stable and reflective of the scale of the underlying business.

In general, faster growing and less risky companies tend to trade on higher price to sales multiples. Slower growth or higher risk typically pushes that multiple down. Vodafone currently trades on a price to sales ratio of about 0.67x, which is well below the Wireless Telecom industry average of around 1.59x and the broader peer group at roughly 2.03x. On those simple comparisons alone, the shares appear inexpensive.

However, Simply Wall St goes a step further by estimating a Fair Ratio. This is the price to sales multiple Vodafone might reasonably deserve once you factor in its growth outlook, profitability, risk profile, industry positioning and size. For Vodafone, that Fair Ratio is 1.54x, above the current 0.67x, which suggests the stock trades at a notable discount even after adjusting for its specific characteristics.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vodafone Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, an easy tool on Simply Wall St's Community page that lets you attach a clear story to your numbers by linking your view of a company’s future revenue, earnings and margins to a financial forecast and an implied fair value. You can then compare that fair value with today’s share price to decide whether to buy or sell, while the Narrative automatically updates when new news or earnings arrive. For example, one Vodafone Group Narrative might lean bullish by assuming revenue grows a little faster, margins expand with German efficiency gains and digital partnerships, and the shares justify a fair value close to the top end of recent analyst targets around £1.36. A more cautious Narrative might focus on German competitive pressures, restructuring risks and slower margin improvement, leading to a fair value nearer the lower end of targets around £0.60. This illustrates how different but clearly defined perspectives can coexist and be tracked side by side.

Do you think there's more to the story for Vodafone Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:VOD

Vodafone Group

Provides telecommunication services in Germany, the United Kingdom, rest of Europe, Turkey, and South Africa.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

42 followersusers have followed this narrative

6 commentsusers have commented on this narrative

14 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative