- United Kingdom

- /

- Wireless Telecom

- /

- LSE:AAF

Does Airtel Africa (LON:AAF) Deserve A Spot On Your Watchlist?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it completely lacks a track record of revenue and profit. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Airtel Africa (LON:AAF). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

See our latest analysis for Airtel Africa

How Fast Is Airtel Africa Growing?

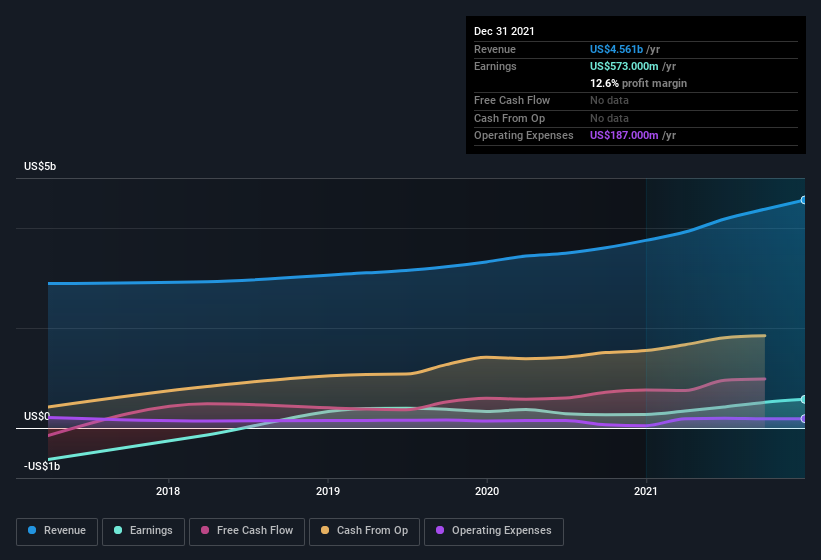

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS). Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Airtel Africa managed to grow EPS by 8.7% per year, over three years. That growth rate is fairly good, assuming the company can keep it up.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. The good news is that Airtel Africa is growing revenues, and EBIT margins improved by 4.5 percentage points to 33%, over the last year. Ticking those two boxes is a good sign of growth, in my book.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. To that end, right now and today, you can check our visualization of consensus analyst forecasts for future Airtel Africa EPS 100% free.

Are Airtel Africa Insiders Aligned With All Shareholders?

Like that fresh smell in the air when the rains are coming, insider buying fills me with optimistic anticipation. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Airtel Africa top brass are certainly in sync, not having sold any shares, over the last year. But the bigger deal is that the Independent Non-Executive Director, Ravi Rajagopal, paid US$50k to buy shares at an average price of US$1.40.

Is Airtel Africa Worth Keeping An Eye On?

As I already mentioned, Airtel Africa is a growing business, which is what I like to see. Not every business can grow its EPS, but Airtel Africa certainly can. The cherry on top is that we have an insider buying shares. That encourages me further to keep an eye on this stock. We don't want to rain on the parade too much, but we did also find 2 warning signs for Airtel Africa that you need to be mindful of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Airtel Africa, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:AAF

Airtel Africa

Provides telecommunications and mobile money services in Nigeria, East Africa, and Francophone Africa.

Undervalued with high growth potential.