Advertisement

- United Kingdom

- /

- Software

- /

- LSE:BYIT

Exploring European Undervalued Small Caps With Insider Action In July 2026

In recent weeks, European markets have been navigating geopolitical tensions and energy market volatility, with key indices like the STOXX Europe 600 experiencing declines. Despite these challenges, certain small-cap stocks in Europe may present opportunities for investors, particularly those showing insider action that could indicate confidence in their growth potential. Identifying such stocks requires careful consideration of market conditions and company fundamentals to assess their true value amidst broader economic uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.1x | 4.4x | 44.93% | ★★★★★★ |

| Eurocell | 11.2x | 0.3x | 49.23% | ★★★★★☆ |

| Nederman Holding | 17.4x | 0.8x | 35.34% | ★★★★★☆ |

| NoHo Partners Oyj | 16.6x | 0.4x | 35.03% | ★★★★★☆ |

| GB Group | NA | 1.8x | 40.15% | ★★★★★☆ |

| Bytes Technology Group | 19.3x | 4.5x | 6.30% | ★★★★☆☆ |

| Bilia | 16.3x | 0.3x | 39.49% | ★★★★☆☆ |

| Volati | 8.2x | 0.2x | 4.34% | ★★★★☆☆ |

| CVS Group | 53.8x | 1.3x | 46.13% | ★★★☆☆☆ |

| KlaraBo Sverige | 7.5x | 2.9x | -201.49% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

Ashtead Technology Holdings (LSE:AT.)

Simply Wall St Value Rating: ★★★★★★

Overview: Ashtead Technology Holdings specializes in providing equipment and services for the oil well sector, with a market capitalization of approximately £0.27 billion.

Operations: The company generates revenue primarily from Oil Well Equipment & Services, with a notable gross profit margin of 74.38% as of December 2025. Operating expenses, including general and administrative costs, are significant components affecting profitability.

PE: 10.7x

Ashtead Technology Holdings, a European small-cap company, is drawing attention for its potential value. Despite relying entirely on external borrowing, indicating higher risk funding with no customer deposits, the firm is in a strong financial position and anticipates earnings growth of 9% annually. Insider confidence was demonstrated through share purchases in early 2026. With Q1 results released on June 9, the company continues to showcase its resilience and potential for future growth within its industry.

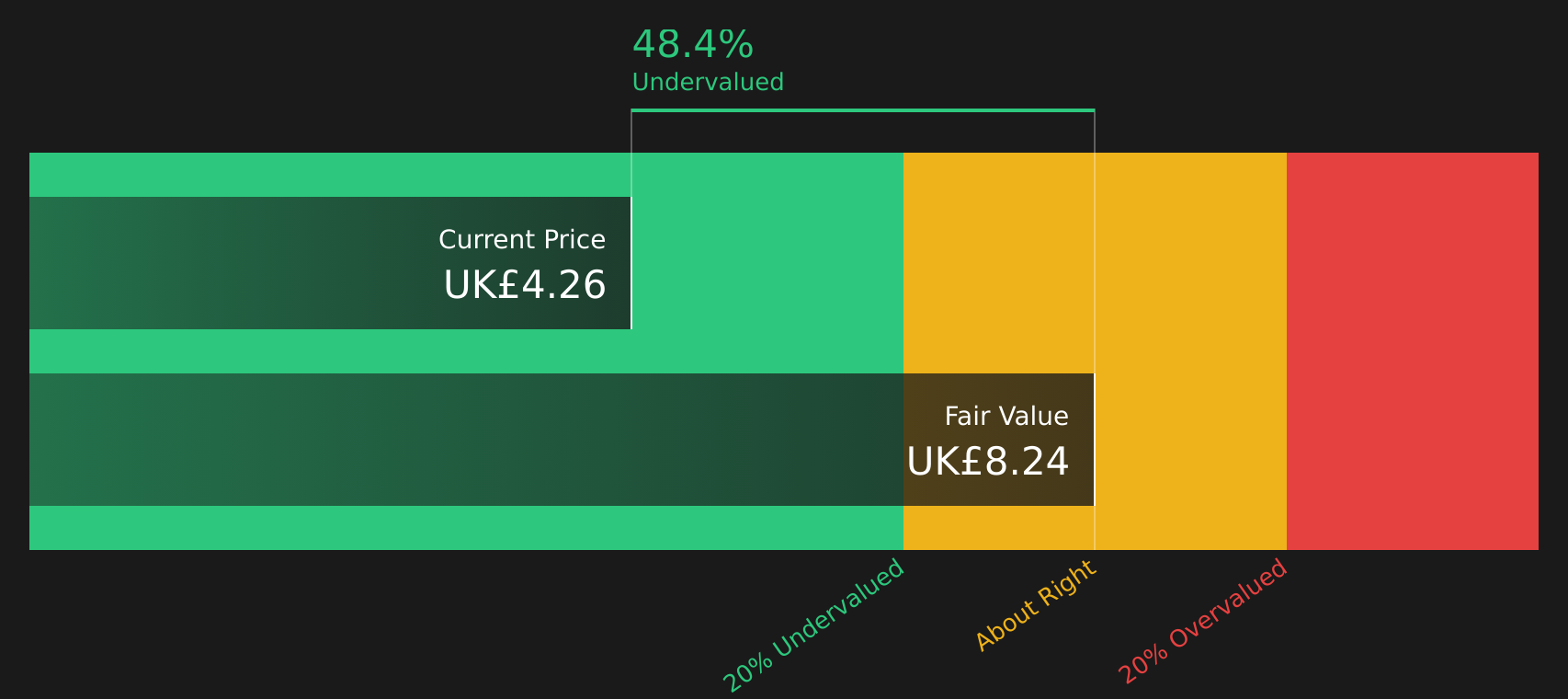

Bytes Technology Group (LSE:BYIT)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bytes Technology Group is an IT solutions provider with a focus on delivering software, security, and cloud services, and it has a market cap of approximately £1.2 billion.

Operations: The company generates revenue primarily from its IT Solutions Provider segment, with a recent revenue figure of £220.56 million. Over time, the gross profit margin has shown an upward trend, reaching 75.86% in the latest period. Operating expenses and non-operating expenses contribute significantly to overall costs, impacting net income margins which have also increased over time to 23.25%.

PE: 19.3x

Bytes Technology Group, a dynamic player in the tech sector, is capturing attention with its strategic moves. The company recently announced a £25 million share repurchase program, reflecting its commitment to enhancing shareholder value. Insider confidence is evident as key figures have been purchasing shares over recent months. Despite earnings showing a slight dip from £54.84 million to £51.28 million for the year ended February 2026, the firm's growth prospects remain promising with projected revenue increases and strategic leadership changes aimed at driving future expansion.

- Unlock comprehensive insights into our analysis of Bytes Technology Group stock in this valuation report.

Gain insights into Bytes Technology Group's past trends and performance with our Past report.

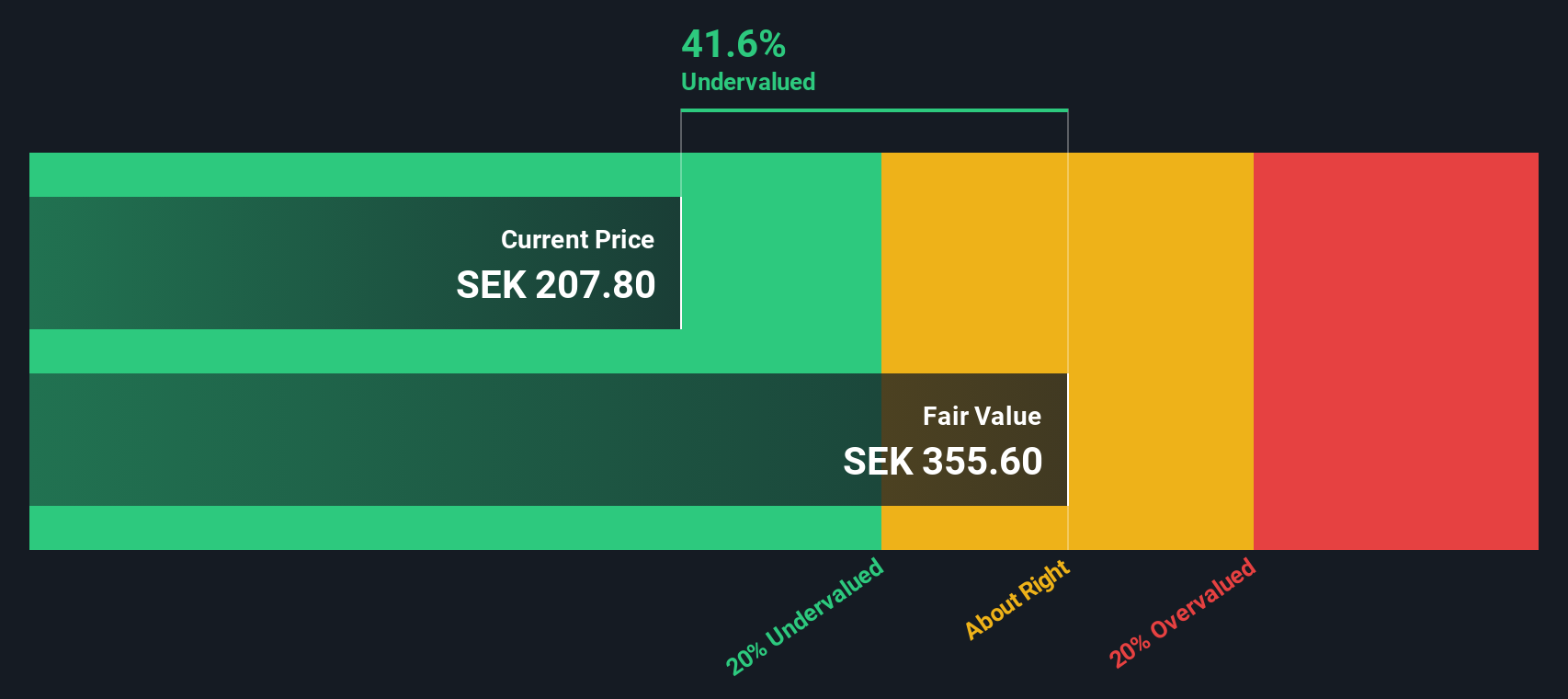

Inwido (OM:INWI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Inwido operates in the window and door manufacturing industry, serving various segments including East, West, E-Commerce, and Scandinavia with a market capitalization of approximately SEK 7.32 billion.

Operations: Inwido generates revenue primarily from its East, West, E-Commerce, and Scandinavia segments. The company reported a gross profit margin of 25.09% as of the latest period. Operating expenses include significant allocations to sales and marketing, research and development, and general administrative activities.

PE: 20.0x

Inwido, a European company in the window and door industry, has recently shown promising financial performance. Their Q2 2026 earnings revealed sales of SEK 2,720.5 million and net income of SEK 197.1 million, both up from last year. Insider confidence is evident as an independent director increased their stake by over 215%, investing approximately SEK 173.68 million. Despite relying on external borrowing for funding, the company's projected annual earnings growth of nearly 18% suggests potential for value appreciation in this segment.

Where To Now?

- Navigate through the entire inventory of 56 Undervalued European Small Caps With Insider Buying here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bytes Technology Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:BYIT

Bytes Technology Group

Offers software, security, AI, and cloud services in the United Kingdom, Europe, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DA

danmad on Cobram Estate Olives ·

More than just olive oil on the shelf

Fair Value:AU$3.64.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$76.85149.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

91 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0