Advertisement

- United Kingdom

- /

- Software

- /

- AIM:PULS

Market Sentiment Around Loss-Making Access Intelligence Plc (LON:ACC)

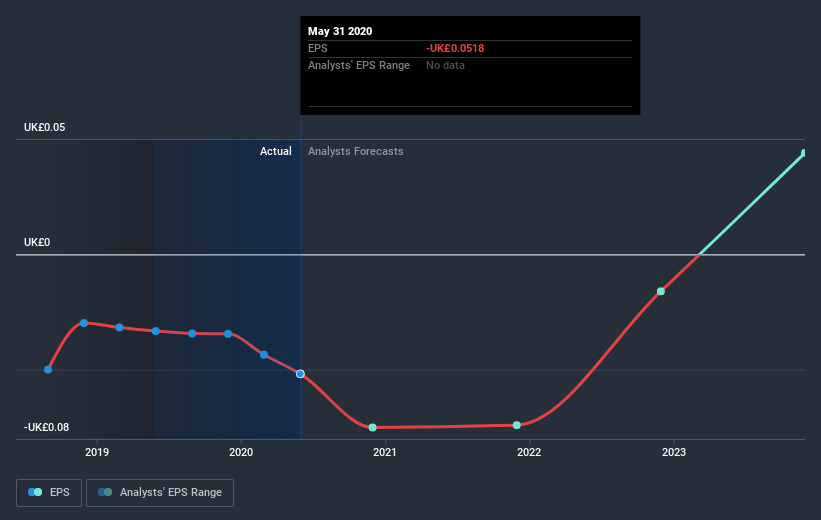

With the business potentially at an important milestone, we thought we'd take a closer look at Access Intelligence Plc's (LON:ACC) future prospects. Access Intelligence Plc, together with its subsidiaries, provides software as a service (SaaS) products to blue-chip enterprises, communications agencies, public sector bodies, and not-for-profit organizations in the United Kingdom, European Union, and internationally. The UK£63m market-cap company posted a loss in its most recent financial year of UK£2.2m and a latest trailing-twelve-month loss of UK£3.5m leading to an even wider gap between loss and breakeven. As path to profitability is the topic on Access Intelligence's investors mind, we've decided to gauge market sentiment. We've put together a brief outline of industry analyst expectations for the company, its year of breakeven and its implied growth rate.

See our latest analysis for Access Intelligence

Expectations from some of the British Software analysts is that Access Intelligence is on the verge of breakeven. They anticipate the company to incur a final loss in 2022, before generating positive profits of UK£3.8m in 2023. So, the company is predicted to breakeven approximately 3 years from today. In order to meet this breakeven date, we calculated the rate at which the company must grow year-on-year. It turns out an average annual growth rate of 55% is expected, which is extremely buoyant. If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Given this is a high-level overview, we won’t go into details of Access Intelligence's upcoming projects, but, take into account that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one aspect worth mentioning. The company has managed its capital prudently, with debt making up 0.1% of equity. This means that it has predominantly funded its operations from equity capital, and its low debt obligation reduces the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Access Intelligence, so if you are interested in understanding the company at a deeper level, take a look at Access Intelligence's company page on Simply Wall St. We've also compiled a list of pertinent aspects you should look at:

- Valuation: What is Access Intelligence worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Access Intelligence is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Access Intelligence’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

When trading Access Intelligence or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About AIM:PULS

Pulsar Group

Provides software-as-a-service products and services to consumer brands and blue-chip enterprises, marketing agencies, and public sector organizations.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

WI

WisetoWealth on PayPal Holdings ·

The Underrated Transformation of a Digital Payments Giant

Fair Value:US$90.3137.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on Terra Balcanica Resources ·

The C$4M Explorer Positioned to Become Europe's First Antimony Mine

Fair Value:CA$0.487.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_6nroa on Charter Communications ·

Charter is undervalued - Here's why.

Fair Value:US$87.0741.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

81 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

185 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0