Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that TheWorks.co.uk plc (LON:WRKS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for TheWorks.co.uk

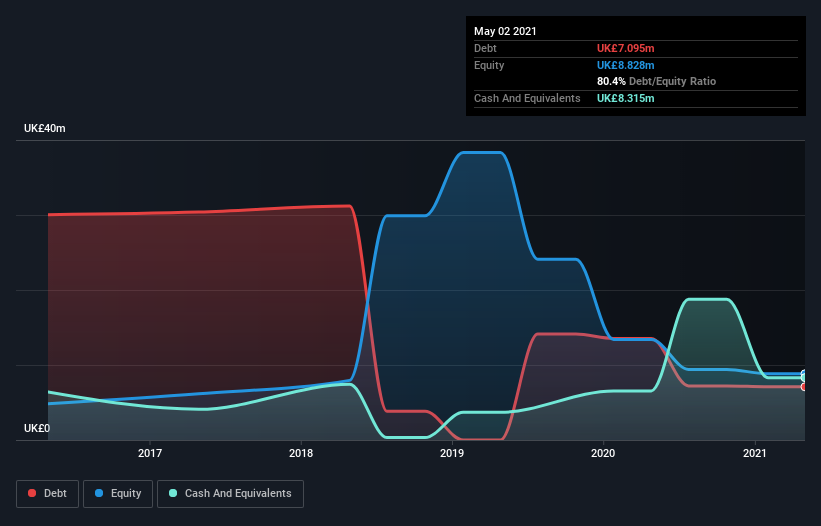

How Much Debt Does TheWorks.co.uk Carry?

As you can see below, TheWorks.co.uk had UK£7.10m of debt at May 2021, down from UK£13.5m a year prior. But on the other hand it also has UK£8.32m in cash, leading to a UK£1.22m net cash position.

How Strong Is TheWorks.co.uk's Balance Sheet?

The latest balance sheet data shows that TheWorks.co.uk had liabilities of UK£67.2m due within a year, and liabilities of UK£104.4m falling due after that. On the other hand, it had cash of UK£8.32m and UK£4.26m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£159.0m.

The deficiency here weighs heavily on the UK£32.0m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, TheWorks.co.uk would likely require a major re-capitalisation if it had to pay its creditors today. TheWorks.co.uk boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if TheWorks.co.uk can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year TheWorks.co.uk had a loss before interest and tax, and actually shrunk its revenue by 20%, to UK£181m. We would much prefer see growth.

So How Risky Is TheWorks.co.uk?

While TheWorks.co.uk lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow UK£28m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. We're not impressed by its revenue growth, so until we see some positive sustainable EBIT, we consider the stock to be high risk. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that TheWorks.co.uk is showing 2 warning signs in our investment analysis , you should know about...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading TheWorks.co.uk or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if TheWorks.co.uk might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:WRKS

TheWorks.co.uk

Engages in the retailing of art and craft products, stationery, toys, games, books, gifts, and seasonal products in the United Kingdom and Ireland.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor