Advertisement

- United Kingdom

- /

- Retail Distributors

- /

- LSE:INCH

Increases to Inchcape plc's (LON:INCH) CEO Compensation Might Cool off for now

Key Insights

- Inchcape's Annual General Meeting to take place on 9th of May

- Total pay for CEO Duncan Tait includes UK£859.0k salary

- The total compensation is 1,439% higher than the average for the industry

- Inchcape's EPS grew by 72% over the past three years while total shareholder return over the past three years was 7.5%

CEO Duncan Tait has done a decent job of delivering relatively good performance at Inchcape plc (LON:INCH) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 9th of May. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Inchcape

Comparing Inchcape plc's CEO Compensation With The Industry

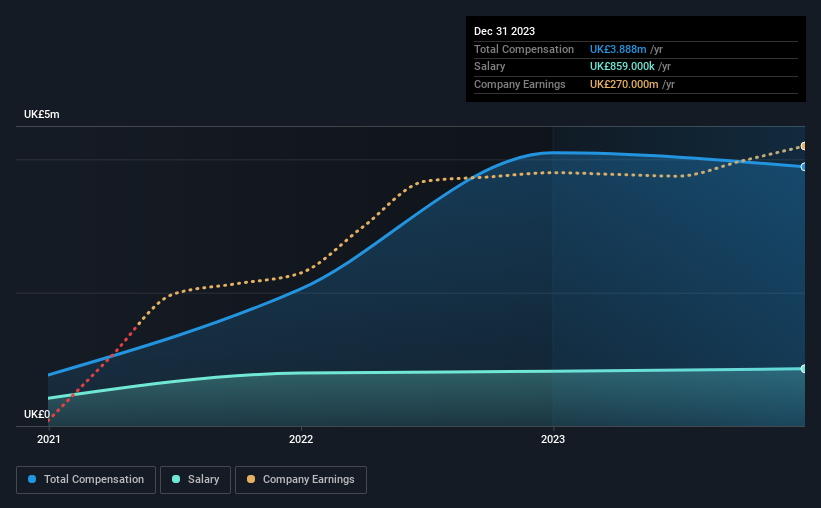

Our data indicates that Inchcape plc has a market capitalization of UK£3.1b, and total annual CEO compensation was reported as UK£3.9m for the year to December 2023. That's slightly lower by 5.1% over the previous year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at UK£859k.

For comparison, other companies in the British Retail Distributors industry with market capitalizations ranging between UK£1.6b and UK£5.1b had a median total CEO compensation of UK£253k. Accordingly, our analysis reveals that Inchcape plc pays Duncan Tait north of the industry median. What's more, Duncan Tait holds UK£2.9m worth of shares in the company in their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | UK£859k | UK£820k | 22% |

| Other | UK£3.0m | UK£3.3m | 78% |

| Total Compensation | UK£3.9m | UK£4.1m | 100% |

On an industry level, around 56% of total compensation represents salary and 44% is other remuneration. Inchcape sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Inchcape plc's Growth

Over the past three years, Inchcape plc has seen its earnings per share (EPS) grow by 72% per year. In the last year, its revenue is up 41%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Inchcape plc Been A Good Investment?

Inchcape plc has not done too badly by shareholders, with a total return of 7.5%, over three years. It would be nice to see that metric improve in the future. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 2 warning signs for Inchcape you should be aware of, and 1 of them is concerning.

Important note: Inchcape is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:INCH

Undervalued with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor