- United Kingdom

- /

- Pharma

- /

- AIM:HCM

HUTCHMED (China) Limited's (LON:HCM) P/S Is Still On The Mark Following 31% Share Price Bounce

HUTCHMED (China) Limited (LON:HCM) shareholders are no doubt pleased to see that the share price has bounced 31% in the last month, although it is still struggling to make up recently lost ground. Looking further back, the 18% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

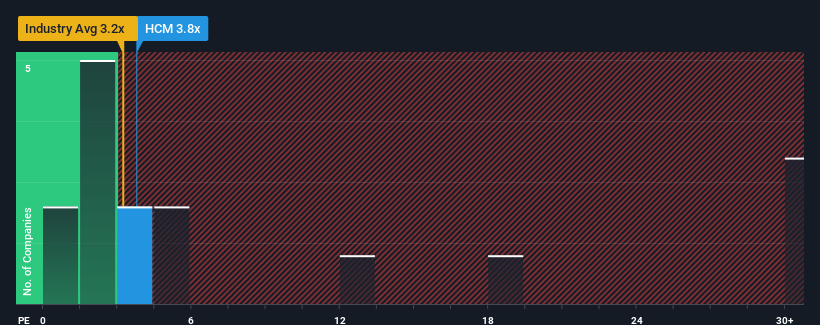

In spite of the firm bounce in price, it's still not a stretch to say that HUTCHMED (China)'s price-to-sales (or "P/S") ratio of 3.8x right now seems quite "middle-of-the-road" compared to the Pharmaceuticals industry in the United Kingdom, where the median P/S ratio is around 3.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for HUTCHMED (China)

What Does HUTCHMED (China)'s Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, HUTCHMED (China) has been doing relatively well. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on HUTCHMED (China) will help you uncover what's on the horizon.How Is HUTCHMED (China)'s Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like HUTCHMED (China)'s to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 97% last year. Pleasingly, revenue has also lifted 268% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 7.3% per annum as estimated by the analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 7.1% each year, which is not materially different.

With this in mind, it makes sense that HUTCHMED (China)'s P/S is closely matching its industry peers. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On HUTCHMED (China)'s P/S

HUTCHMED (China) appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at HUTCHMED (China)'s revenue growth estimates show that its P/S is about what we expect, as both metrics follow closely with the industry averages. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

Having said that, be aware HUTCHMED (China) is showing 1 warning sign in our investment analysis, you should know about.

If you're unsure about the strength of HUTCHMED (China)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if HUTCHMED (China) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:HCM

HUTCHMED (China)

HUTCHMED (China) Limited, together with its subsidiaries, discovers, develops, and commercializes targeted therapeutics and immunotherapies to treat cancer and immunological diseases in Hong Kong, the United States, and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Community Narratives