Advertisement

- United Kingdom

- /

- Diversified Financial

- /

- AIM:FNX

Exploring Three Undiscovered UK Stocks In July 2024

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom stock market has shown steady growth, rising 7.6% over the past year, with a flat performance in the last week and expectations for earnings to grow by 13% annually. In this context, identifying stocks that have not yet caught the attention of the broader market can offer unique opportunities for investors looking for potential growth in a generally ascending market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| Georgia Capital | NA | -27.80% | 18.94% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Fix Price Group | 43.59% | 12.53% | 23.49% | ★★★★★☆ |

| Ros Agro | 57.18% | 17.80% | 18.35% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Bioventix (AIM:BVXP)

Simply Wall St Value Rating: ★★★★★★

Overview: Bioventix PLC specializes in the creation, manufacturing, and supply of sheep monoclonal antibodies for diagnostic uses globally, with a market capitalization of £215.31 million.

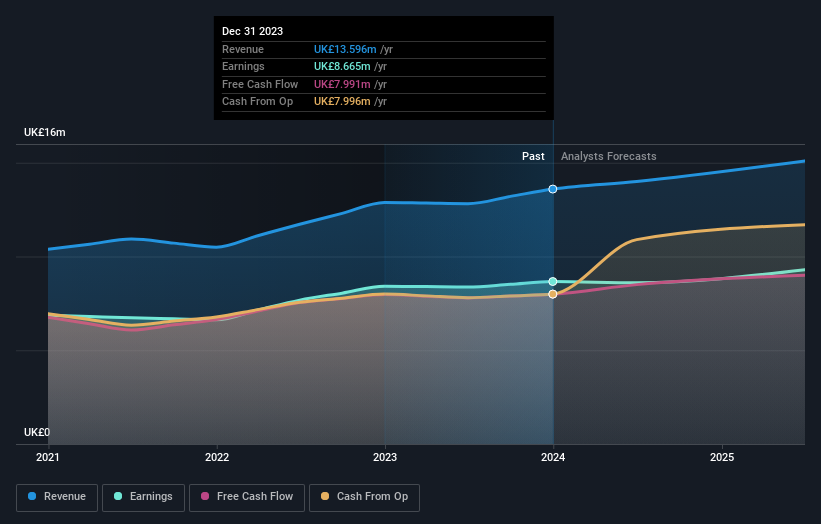

Operations: The entity generates revenue through its biotechnology operations, achieving a gross profit of £12.75 million on revenues of £13.60 million, reflecting a high gross profit margin of approximately 93.75%. This efficiency underscores the company's ability to manage production costs effectively while maintaining robust profitability in its niche market.

Bioventix, a lesser-known yet promising player in the biotech sector, showcases robust financial and operational health. With no debt and earnings growth outpacing the industry at 3% compared to 2.9%, it stands out for its efficiency. The company's price-to-earnings ratio of 24.8x, significantly lower than the industry average of 33.1x, suggests good value. Forecasted annual earnings growth of approximately 5% further highlights its potential as an undiscovered gem in the UK market.

Bioventix (AIM:BVXP)

Simply Wall St Value Rating: ★★★★★★

Overview: Bioventix PLC specializes in the creation, manufacturing, and supply of sheep monoclonal antibodies for diagnostic uses globally, with a market capitalization of £215.31 million.

Operations: The entity generates revenue through its biotechnology operations, achieving a gross profit of £12.75 million on revenues of £13.60 million, reflecting a high gross profit margin of approximately 93.75%. This efficiency underscores the company's ability to manage production costs effectively while maintaining robust profitability in its niche market.

Bioventix, a lesser-known yet promising player in the biotech sector, showcases robust financial and operational health. With no debt and earnings growth outpacing the industry at 3% compared to 2.9%, it stands out for its efficiency. The company's price-to-earnings ratio of 24.8x, significantly lower than the industry average of 33.1x, suggests good value. Forecasted annual earnings growth of approximately 5% further highlights its potential as an undiscovered gem in the UK market.

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc is a management consultancy firm operating in the United Kingdom, the United States, and other international markets, with a market capitalization of £253.65 million.

Operations: The company generates its revenue primarily through management consulting services, achieving a gross profit margin of 34.07% in the most recent fiscal period. Its cost of goods sold was £56.621 million, with operating expenses amounting to £8.607 million during the same timeframe.

Elixirr International, a standout among UK's lesser-known entities, trades at 60.1% below its fair value, showcasing significant investment appeal. With a robust earnings growth of 33.9% last year—surpassing the industry average by nearly 33%—and an anticipated annual growth rate of about 9%, Elixirr demonstrates strong financial health and potential for sustained profitability. Moreover, the company is debt-free and has managed to maintain high-quality earnings without diluting shareholder value over the past year, despite significant insider selling in recent months. These attributes position Elixirr as a compelling choice for those seeking undiscovered gems with promising futures.

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc is a management consultancy firm operating in the United Kingdom, the United States, and other international markets, with a market capitalization of £253.65 million.

Operations: The company generates its revenue primarily through management consulting services, achieving a gross profit margin of 34.07% in the most recent fiscal period. Its cost of goods sold was £56.621 million, with operating expenses amounting to £8.607 million during the same timeframe.

Elixirr International, a standout among UK's lesser-known entities, trades at 60.1% below its fair value, showcasing significant investment appeal. With a robust earnings growth of 33.9% last year—surpassing the industry average by nearly 33%—and an anticipated annual growth rate of about 9%, Elixirr demonstrates strong financial health and potential for sustained profitability. Moreover, the company is debt-free and has managed to maintain high-quality earnings without diluting shareholder value over the past year, despite significant insider selling in recent months. These attributes position Elixirr as a compelling choice for those seeking undiscovered gems with promising futures.

Fonix Mobile (AIM:FNX)

Simply Wall St Value Rating: ★★★★★★

Overview: Fonix Mobile plc operates in the United Kingdom, offering mobile payments, messaging, and managed services tailored for sectors including media, charity, gaming, ticketing, and mobility. The company has a market cap of £236.06 million.

Operations: This entity generates revenue primarily through facilitating mobile payments and messaging services, achieving a gross profit of £16.47 million on revenues of £71.76 million in the most recent fiscal period. The gross profit margin for this period stood at 22.95%.

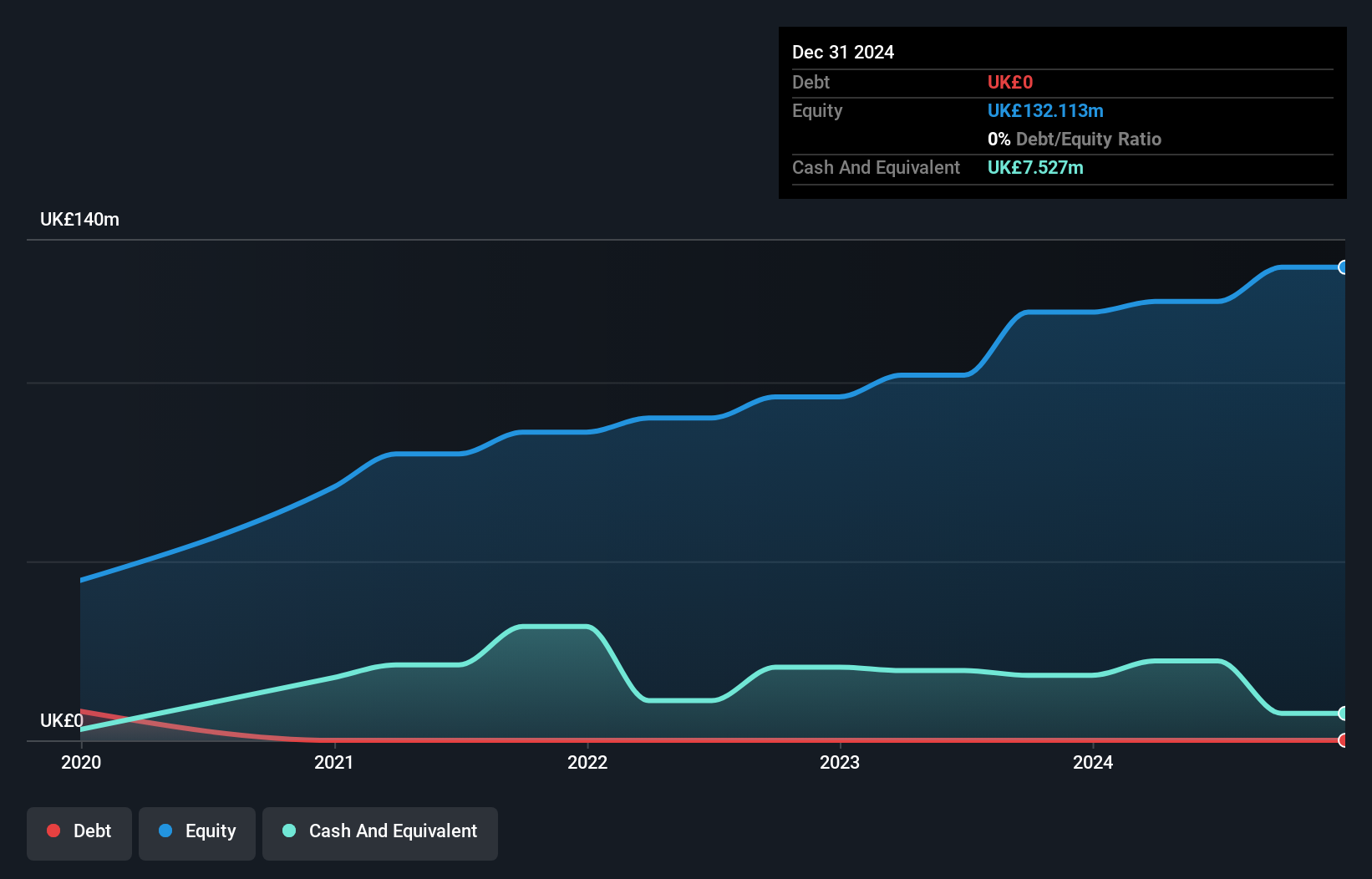

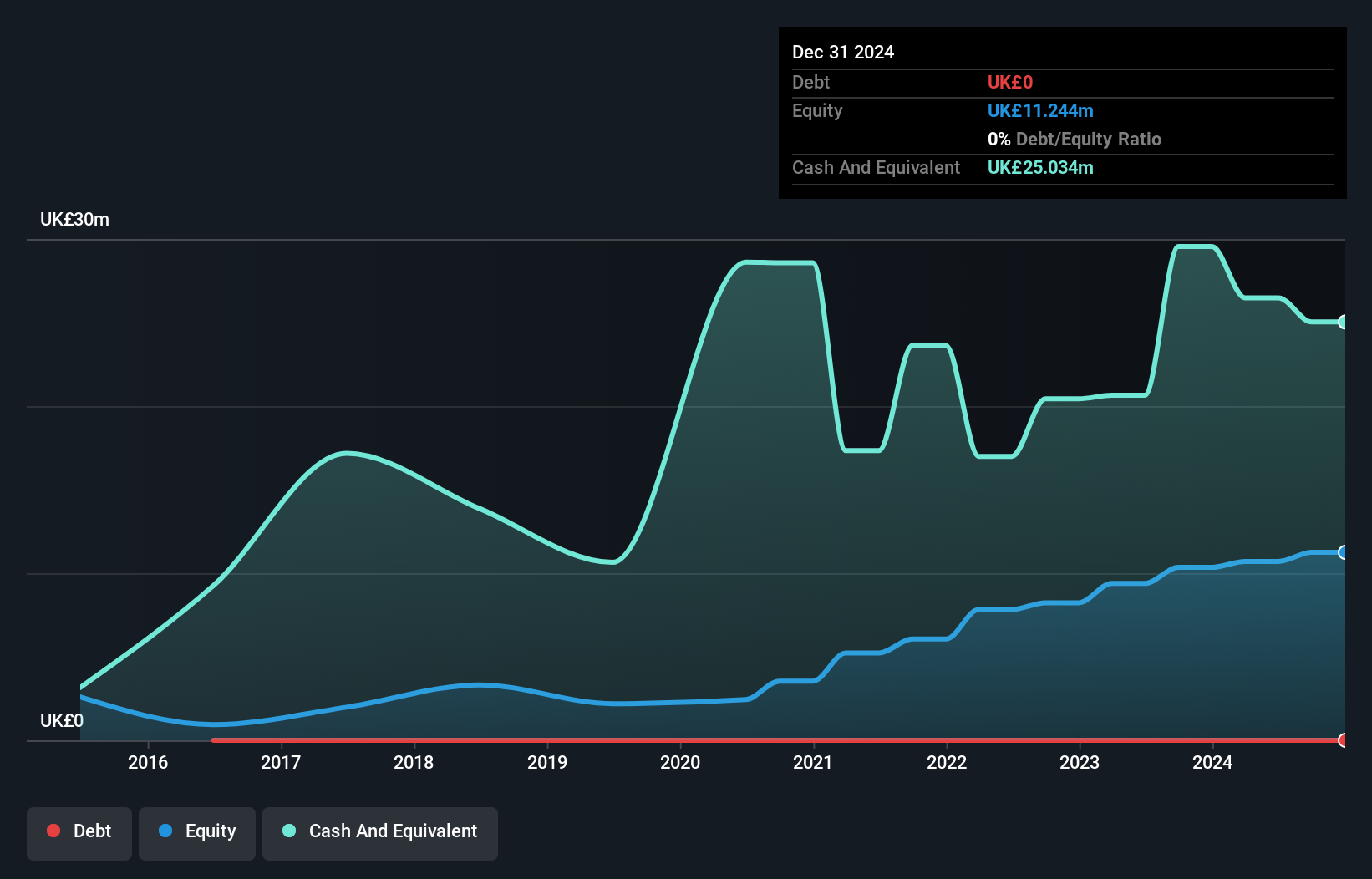

Fonix Mobile, a standout in the Diversified Financial sector, has showcased a robust performance with earnings up by 13% over the past year. With no debt on its books and positive free cash flow, Fonix is well-positioned for sustained growth. The company's recent £15 million equity offering highlights its proactive approach to capital management. Outpacing industry trends where others saw declines of 12%, Fonix's strategic financial health continues to attract attention.

- Click to explore a detailed breakdown of our findings in Fonix Mobile's health report.

Evaluate Fonix Mobile's historical performance by accessing our past performance report.

Fonix Mobile (AIM:FNX)

Simply Wall St Value Rating: ★★★★★★

Overview: Fonix Mobile plc operates in the United Kingdom, offering mobile payments, messaging, and managed services tailored for sectors including media, charity, gaming, ticketing, and mobility. The company has a market cap of £236.06 million.

Operations: This entity generates revenue primarily through facilitating mobile payments and messaging services, achieving a gross profit of £16.47 million on revenues of £71.76 million in the most recent fiscal period. The gross profit margin for this period stood at 22.95%.

Fonix Mobile, a standout in the Diversified Financial sector, has showcased a robust performance with earnings up by 13% over the past year. With no debt on its books and positive free cash flow, Fonix is well-positioned for sustained growth. The company's recent £15 million equity offering highlights its proactive approach to capital management. Outpacing industry trends where others saw declines of 12%, Fonix's strategic financial health continues to attract attention.

- Click to explore a detailed breakdown of our findings in Fonix Mobile's health report.

Evaluate Fonix Mobile's historical performance by accessing our past performance report.

Next Steps

- Explore the 79 names from our UK Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:FNX

Fonix

Provides mobile payments and messaging, and managed services for media, charity, gaming, e-mobility, and other digital service businesses in the United Kingdom.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|43.3% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|50.1% undervalued

TO

Community Contributor