Advertisement

- United Kingdom

- /

- Metals and Mining

- /

- LSE:FRES

There Could Be A Chance Fresnillo plc's (LON:FRES) CEO Will Have Their Compensation Increased

Key Insights

- Fresnillo's Annual General Meeting to take place on 20th of May

- Salary of US$1.28m is part of CEO Octavio Alvidrez's total remuneration

- The overall pay is 62% below the industry average

- Fresnillo's EPS declined by 31% over the past three years while total shareholder return over the past three years was 44%

Shareholders will probably not be disappointed by the robust results at Fresnillo plc (LON:FRES) recently and they will be keeping this in mind as they go into the AGM on 20th of May. This would also be a chance for them to hear the board review the financial results, discuss future company strategy to further improve the business and vote on any resolutions such as executive remuneration. We have prepared some analysis below and we show why we think CEO compensation looks decent with even the possibility for a raise.

See our latest analysis for Fresnillo

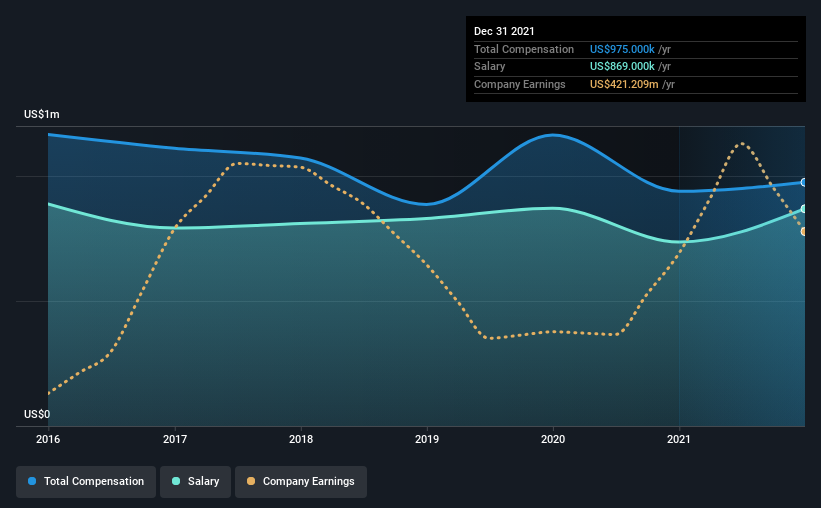

How Does Total Compensation For Octavio Alvidrez Compare With Other Companies In The Industry?

According to our data, Fresnillo plc has a market capitalization of UK£7.4b, and paid its CEO total annual compensation worth US$2.0m over the year to December 2024. We note that's an increase of 49% above last year. We note that the salary portion, which stands at US$1.28m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the British Metals and Mining industry with market capitalizations over UK£6.1b, the reported median total CEO compensation was US$5.4m. In other words, Fresnillo pays its CEO lower than the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$1.3m | US$1.1m | 63% |

| Other | US$766k | US$259k | 37% |

| Total Compensation | US$2.0m | US$1.4m | 100% |

Speaking on an industry level, nearly 65% of total compensation represents salary, while the remainder of 35% is other remuneration. Our data reveals that Fresnillo allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Fresnillo plc's Growth

Over the last three years, Fresnillo plc has shrunk its earnings per share by 31% per year. Its revenue is up 29% over the last year.

The reduction in EPS, over three years, is arguably concerning. On the other hand, the strong revenue growth suggests the business is growing. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Fresnillo plc Been A Good Investment?

Most shareholders would probably be pleased with Fresnillo plc for providing a total return of 44% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 2 warning signs for Fresnillo that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:FRES

Fresnillo

Fresnillo plc mines, develops, and produces non-ferrous minerals in Mexico.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor