- United Kingdom

- /

- Basic Materials

- /

- LSE:FORT

Does Forterra's (LON:FORT) CEO Salary Compare Well With The Performance Of The Company?

Stephen Harrison became the CEO of Forterra plc (LON:FORT) in 2016, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Forterra pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

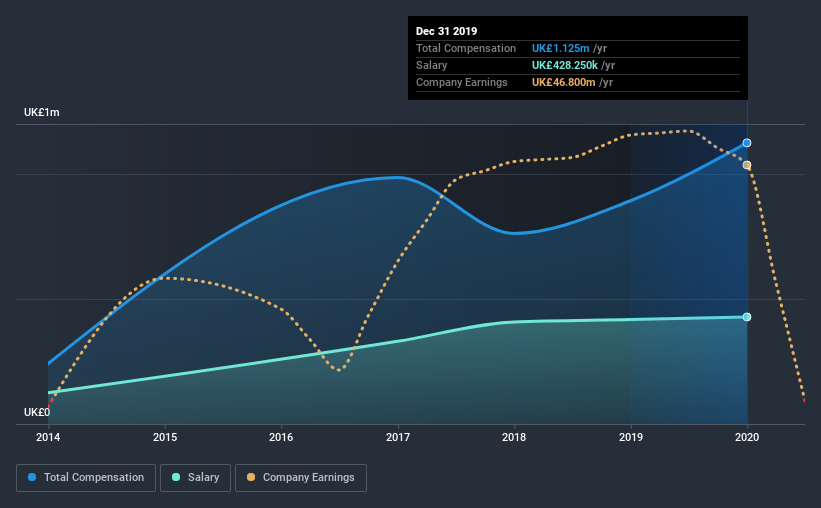

View our latest analysis for Forterra

Comparing Forterra plc's CEO Compensation With the industry

Our data indicates that Forterra plc has a market capitalization of UK£534m, and total annual CEO compensation was reported as UK£1.1m for the year to December 2019. Notably, that's an increase of 26% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at UK£428k.

For comparison, other companies in the same industry with market capitalizations ranging between UK£299m and UK£1.2b had a median total CEO compensation of UK£584k. Hence, we can conclude that Stephen Harrison is remunerated higher than the industry median. Furthermore, Stephen Harrison directly owns UK£435k worth of shares in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | UK£428k | UK£418k | 38% |

| Other | UK£696k | UK£475k | 62% |

| Total Compensation | UK£1.1m | UK£893k | 100% |

Talking in terms of the industry, salary represented approximately 43% of total compensation out of all the companies we analyzed, while other remuneration made up 57% of the pie. Forterra sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Forterra plc's Growth

Forterra plc has reduced its earnings per share by 18% a year over the last three years. Its revenue is down 19% over the previous year.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Forterra plc Been A Good Investment?

With a three year total loss of 14% for the shareholders, Forterra plc would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we touched on above, Forterra plc is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Unfortunately, this doesn't look great when you see shareholder returns have been negative over the last three years. Arguably worse, we've been waiting for positive EPS growth for the last three years. Considering such poor performance, we think shareholders might be concerned if the CEO's compensation were to grow.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 3 warning signs (and 1 which is a bit concerning) in Forterra we think you should know about.

Important note: Forterra is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you’re looking to trade Forterra, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:FORT

Forterra

Engages in the manufacture and sale of building products in the United Kingdom.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Community Narratives