- United Kingdom

- /

- Metals and Mining

- /

- AIM:HUM

Will Weakness in Hummingbird Resources PLC's (LON:HUM) Stock Prove Temporary Given Strong Fundamentals?

It is hard to get excited after looking at Hummingbird Resources' (LON:HUM) recent performance, when its stock has declined 14% over the past three months. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Particularly, we will be paying attention to Hummingbird Resources' ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Hummingbird Resources

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hummingbird Resources is:

23% = US$37m ÷ US$162m (Based on the trailing twelve months to June 2020).

The 'return' is the profit over the last twelve months. That means that for every £1 worth of shareholders' equity, the company generated £0.23 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

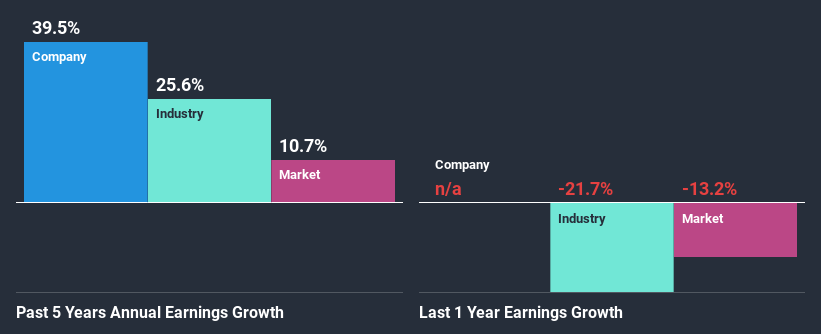

A Side By Side comparison of Hummingbird Resources' Earnings Growth And 23% ROE

Firstly, we acknowledge that Hummingbird Resources has a significantly high ROE. Additionally, the company's ROE is higher compared to the industry average of 17% which is quite remarkable. So, the substantial 40% net income growth seen by Hummingbird Resources over the past five years isn't overly surprising.

As a next step, we compared Hummingbird Resources' net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 26%.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Hummingbird Resources''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Hummingbird Resources Using Its Retained Earnings Effectively?

Summary

Overall, we are quite pleased with Hummingbird Resources' performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. That being so, a study of the latest analyst forecasts show that the company is expected to see a slowdown in its future earnings growth. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you’re looking to trade Hummingbird Resources, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hummingbird Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About AIM:HUM

Hummingbird Resources

Engages in the exploration, evaluation, and development of mineral properties in Liberia, Mali, and Guinea.

Slight and slightly overvalued.