- United Kingdom

- /

- Consumer Durables

- /

- AIM:AIEA

3 Promising UK Penny Stocks With Market Caps Under £60M

Reviewed by Simply Wall St

The UK market has recently experienced some turbulence, with the FTSE 100 index closing lower due to weak trade data from China, highlighting global economic interdependencies. Despite these broader market challenges, certain investment opportunities remain compelling. Penny stocks, while a somewhat outdated term, continue to offer potential for growth when backed by strong financial health and strategic positioning. In this context, we will explore several UK penny stocks that demonstrate promising financial strength and potential for long-term success.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Financial Health Rating |

| ME Group International (LSE:MEGP) | £2.01 | £757.4M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.966 | £152.38M | ★★★★★★ |

| Polar Capital Holdings (AIM:POLR) | £4.87 | £469.45M | ★★★★★★ |

| Foresight Group Holdings (LSE:FSG) | £3.71 | £425.03M | ★★★★★★ |

| Stelrad Group (LSE:SRAD) | £1.40 | £178.29M | ★★★★★☆ |

| Secure Trust Bank (LSE:STB) | £3.52 | £67.13M | ★★★★☆☆ |

| Luceco (LSE:LUCE) | £1.20 | £185.07M | ★★★★★☆ |

| Next 15 Group (AIM:NFG) | £3.63 | £361.03M | ★★★★☆☆ |

| On the Beach Group (LSE:OTB) | £2.35 | £392.43M | ★★★★★★ |

| Tristel (AIM:TSTL) | £4.25 | £202.69M | ★★★★★★ |

Click here to see the full list of 468 stocks from our UK Penny Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

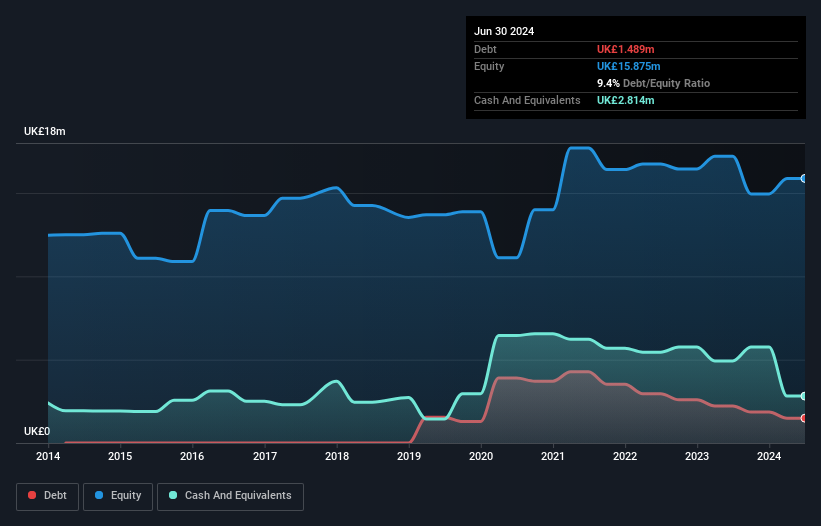

AIREA (AIM:AIEA)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: AIREA plc, with a market cap of £7.33 million, designs, manufactures, and sells floor coverings in the United Kingdom and internationally through its subsidiaries.

Operations: The company generates revenue from its Textile Manufacturing segment, which amounts to £20.55 million.

Market Cap: £7.33M

AIREA plc, with a market cap of £7.33 million, shows a mixed financial picture. The company's short-term assets comfortably cover both its short and long-term liabilities, and it holds more cash than total debt. However, AIREA's net profit margin has declined significantly from the previous year and earnings growth has been negative over the past five years. While its debt is well covered by operating cash flow, the dividend yield of 2.89% is not supported by earnings or free cash flows. Additionally, the board lacks experience with an average tenure under two years, which may impact strategic direction.

- Get an in-depth perspective on AIREA's performance by reading our balance sheet health report here.

- Explore historical data to track AIREA's performance over time in our past results report.

Nexteq (AIM:NXQ)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Nexteq plc is a business-to-business technology design and supply chain partner for industrial equipment manufacturers across North America, Europe, Asia, Australia, the rest of the United Kingdom, and internationally with a market cap of £38.76 million.

Operations: The company's revenue is derived from its Quixant segment, which generated $65.87 million, and its Densitron segment, which brought in $40.42 million.

Market Cap: £38.76M

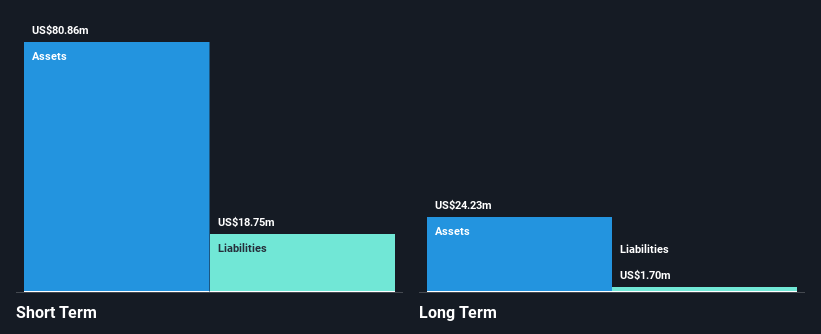

Nexteq plc, with a market cap of £38.76 million, presents a complex financial landscape for investors in penny stocks. Despite having high-quality past earnings and significant profit growth over the past five years, the company faces challenges with declining net profit margins and forecasted earnings declines averaging 96.2% annually over the next three years. Recent leadership changes see Matt Staight stepping in as CFO amid efforts to manage costs following lowered revenue guidance for 2024. Positively, Nexteq's debt is well covered by operating cash flow and short-term assets exceed both short-term and long-term liabilities, indicating solid financial management despite volatility concerns.

- Unlock comprehensive insights into our analysis of Nexteq stock in this financial health report.

- Assess Nexteq's future earnings estimates with our detailed growth reports.

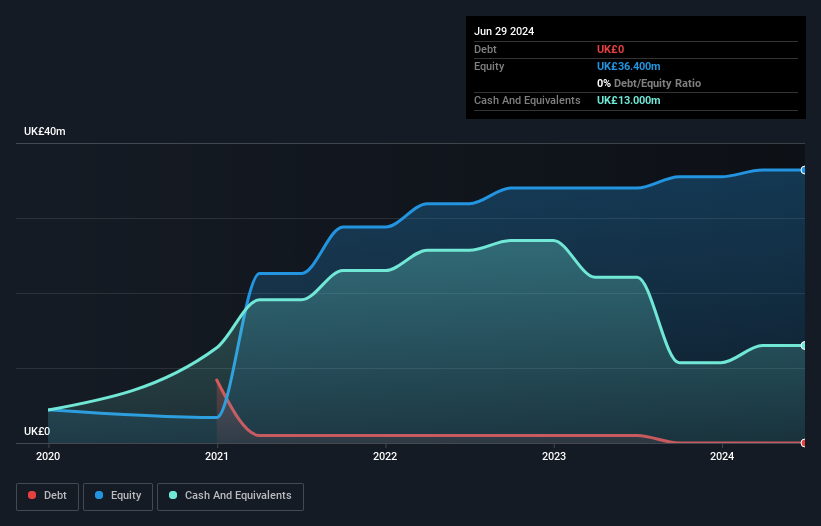

National World (LSE:NWOR)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: National World Plc operates in the United Kingdom, offering news and information services through a range of multimedia publications and websites, with a market cap of £59.96 million.

Operations: The company generates revenue of £95.6 million from identifying and acquiring investment projects.

Market Cap: £59.96M

National World Plc, with a market cap of £59.96 million, offers intriguing prospects for penny stock investors despite recent challenges. The company has seen significant earnings growth over the past five years but faced negative earnings growth last year and declining net profit margins from 4.2% to 2.5%. Its financial stability is supported by short-term assets exceeding liabilities and no debt burden, although volatility remains high. Recent developments include Media Concierge's proposal to acquire the remaining stake in National World at a premium price, which could provide shareholders an opportunity to realize their investment value if approved in Q1 2025.

- Take a closer look at National World's potential here in our financial health report.

- Gain insights into National World's outlook and expected performance with our report on the company's earnings estimates.

Make It Happen

- Navigate through the entire inventory of 468 UK Penny Stocks here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:AIEA

AIREA

Engages in the design, manufacture, and sale of floor coverings in the United Kingdom and internationally.

Flawless balance sheet slight.

Market Insights

Community Narratives