Advertisement

- United Kingdom

- /

- Metals and Mining

- /

- AIM:BMN

We Think Bushveld Minerals (LON:BMN) Has A Fair Chunk Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Bushveld Minerals Limited (LON:BMN) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Bushveld Minerals

What Is Bushveld Minerals's Debt?

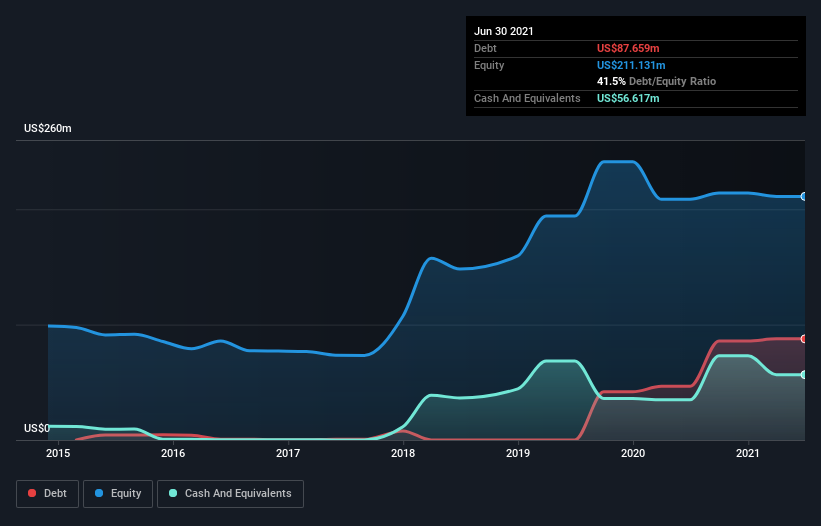

As you can see below, at the end of June 2021, Bushveld Minerals had US$87.7m of debt, up from US$46.5m a year ago. Click the image for more detail. However, it also had US$56.6m in cash, and so its net debt is US$31.0m.

A Look At Bushveld Minerals' Liabilities

We can see from the most recent balance sheet that Bushveld Minerals had liabilities of US$48.1m falling due within a year, and liabilities of US$96.6m due beyond that. Offsetting this, it had US$56.6m in cash and US$16.0m in receivables that were due within 12 months. So it has liabilities totalling US$72.0m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Bushveld Minerals is worth US$158.8m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Bushveld Minerals's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Bushveld Minerals wasn't profitable at an EBIT level, but managed to grow its revenue by 15%, to US$94m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months Bushveld Minerals produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable US$39m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through US$48m of cash over the last year. So suffice it to say we consider the stock very risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 4 warning signs with Bushveld Minerals (at least 2 which are a bit unpleasant) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Bushveld Minerals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:BMN

Bushveld Minerals

Operates as an integrated primary vanadium and energy storage solutions provider for the steel, energy, and chemical industries in South Africa, Europe, Asia, the United States, and internationally.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor