Advertisement

- United Kingdom

- /

- Diversified Financial

- /

- LSE:WPS

3 UK Stocks Estimated Up To 46.9% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom's FTSE 100 index has recently faced downward pressure, influenced by weak trade data from China and its ongoing economic challenges. As the market navigates these global headwinds, identifying undervalued stocks can present opportunities for investors seeking to capitalize on discrepancies between current market prices and intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| QinetiQ Group (LSE:QQ.) | £3.928 | £7.81 | 49.7% |

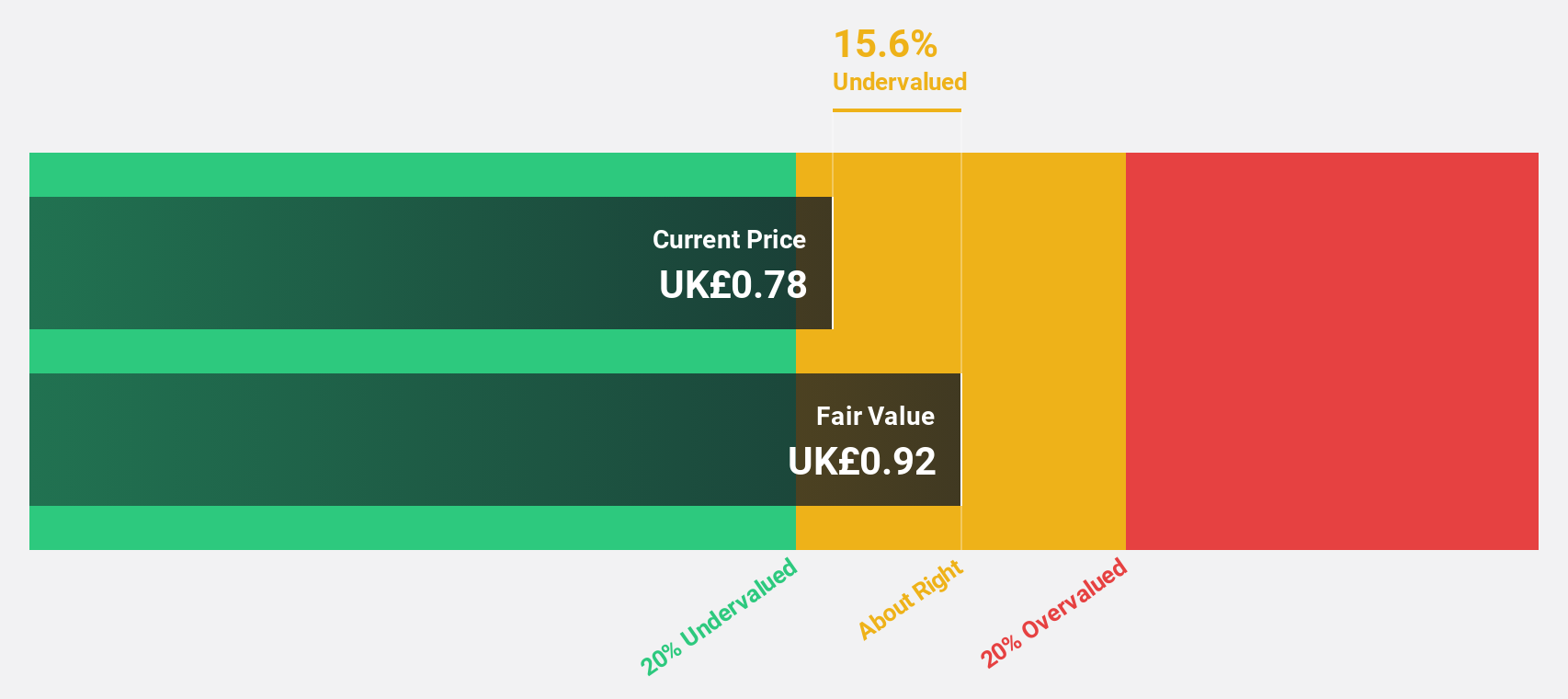

| Gaming Realms (AIM:GMR) | £0.352 | £0.66 | 46.4% |

| Informa (LSE:INF) | £7.886 | £14.49 | 45.6% |

| M&C Saatchi (AIM:SAA) | £1.655 | £3.12 | 46.9% |

| Duke Capital (AIM:DUKE) | £0.28 | £0.54 | 48.2% |

| Itim Group (AIM:ITIM) | £0.47 | £0.90 | 47.8% |

| TI Fluid Systems (LSE:TIFS) | £1.978 | £3.83 | 48.3% |

| Vanquis Banking Group (LSE:VANQ) | £0.592 | £1.13 | 47.8% |

| Optima Health (AIM:OPT) | £1.71 | £3.34 | 48.9% |

| Crest Nicholson Holdings (LSE:CRST) | £1.734 | £3.23 | 46.3% |

Here's a peek at a few of the choices from the screener.

CVS Group (AIM:CVSG)

Overview: CVS Group plc operates in veterinary services, pet crematoria, online pharmacy, and retail sectors, with a market cap of £726.01 million.

Operations: The company's revenue is primarily generated from its Veterinary Practices (£600.50 million), Online Retail Business (£48.50 million), Laboratories (£30.90 million), and Crematoria services (£12.20 million).

Estimated Discount To Fair Value: 44.2%

CVS Group is trading at £10.12, significantly below its estimated fair value of £18.15, indicating potential undervaluation based on cash flows. Despite a decline in net income to £11.2 million for the half-year ending December 31, 2024, CVS's earnings are forecast to grow by 21% annually over the next three years—surpassing UK market expectations. However, profit margins have decreased from last year and interest payments are not well covered by earnings.

- Our growth report here indicates CVS Group may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of CVS Group stock in this financial health report.

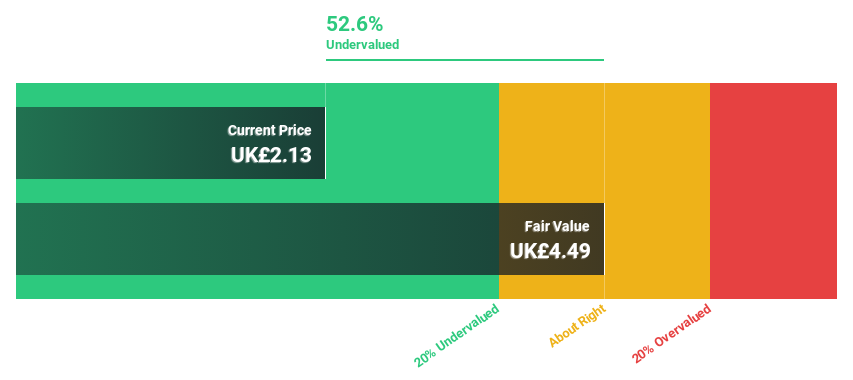

M&C Saatchi (AIM:SAA)

Overview: M&C Saatchi plc offers advertising and marketing communications services across the UK, Europe, the Middle East, Africa, Asia Pacific, and the Americas with a market cap of £202.34 million.

Operations: M&C Saatchi plc generates revenue through its advertising and marketing communications services across various regions including the UK, Europe, the Middle East, Africa, Asia Pacific, and the Americas.

Estimated Discount To Fair Value: 46.9%

M&C Saatchi is trading at £1.66, significantly below its estimated fair value of £3.12, highlighting potential undervaluation based on cash flows. The company returned to profitability with a net income of £14.73 million in 2024 and earnings are forecast to grow by 26.35% annually over the next three years, outpacing the UK market average growth rate of 14.2%. However, revenue is expected to decline by 15.8% per year over the same period.

- According our earnings growth report, there's an indication that M&C Saatchi might be ready to expand.

- Click here to discover the nuances of M&C Saatchi with our detailed financial health report.

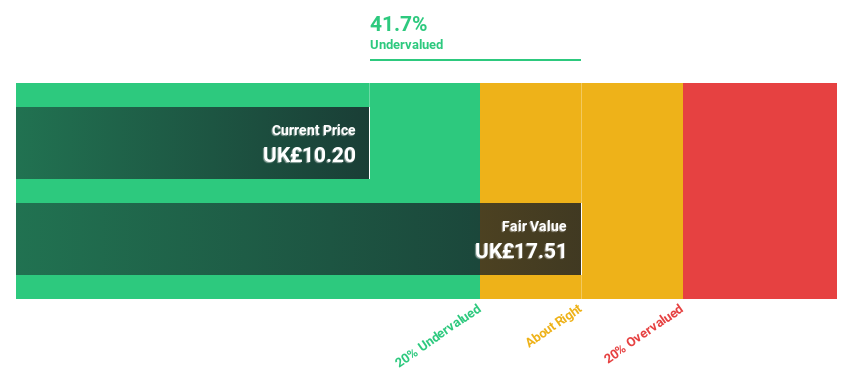

W.A.G payment solutions (LSE:WPS)

Overview: W.A.G payment solutions plc operates an integrated payments and mobility platform targeting the commercial road transportation industry primarily in Europe, with a market cap of £408.17 million.

Operations: The company generates revenue from its Payment Solutions segment, which accounts for €2.11 billion, and its Mobility Solutions segment, contributing €125.60 million.

Estimated Discount To Fair Value: 33.8%

W.A.G payment solutions is trading at £0.59, over 20% below its estimated fair value of £0.89, suggesting it may be undervalued based on cash flows. The company turned profitable in 2024 with a net income of €2.7 million and earnings are projected to grow significantly by 35.37% annually over the next three years, surpassing the UK market's average growth rate of 14.1%. However, revenue is forecast to decline by a very large percentage annually during this period.

- Our expertly prepared growth report on W.A.G payment solutions implies its future financial outlook may be stronger than recent results.

- Take a closer look at W.A.G payment solutions' balance sheet health here in our report.

Make It Happen

- Gain an insight into the universe of 53 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W.A.G payment solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:WPS

W.A.G payment solutions

Operates integrated payments and mobility platform that focuses on the commercial road transportation industry primary in Europe.

Very undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.3% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|33.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|27.0% undervalued

MA

Community Contributor