- United Kingdom

- /

- Oil and Gas

- /

- AIM:YCA

Spotlighting 3 Undiscovered Gems in the United Kingdom

Reviewed by Simply Wall St

The United Kingdom's FTSE 100 index has recently faced downward pressure due to weak trade data from China, highlighting the interconnectedness of global markets and the challenges that can arise from economic slowdowns in major economies. Despite these broader market headwinds, there are still opportunities to be found within the UK market, particularly among small-cap stocks that can offer unique growth potential and resilience in diverse economic conditions. In this article, we will spotlight three undiscovered gems in the United Kingdom that exhibit promising characteristics such as strong fundamentals, innovative business models, and potential for long-term growth.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

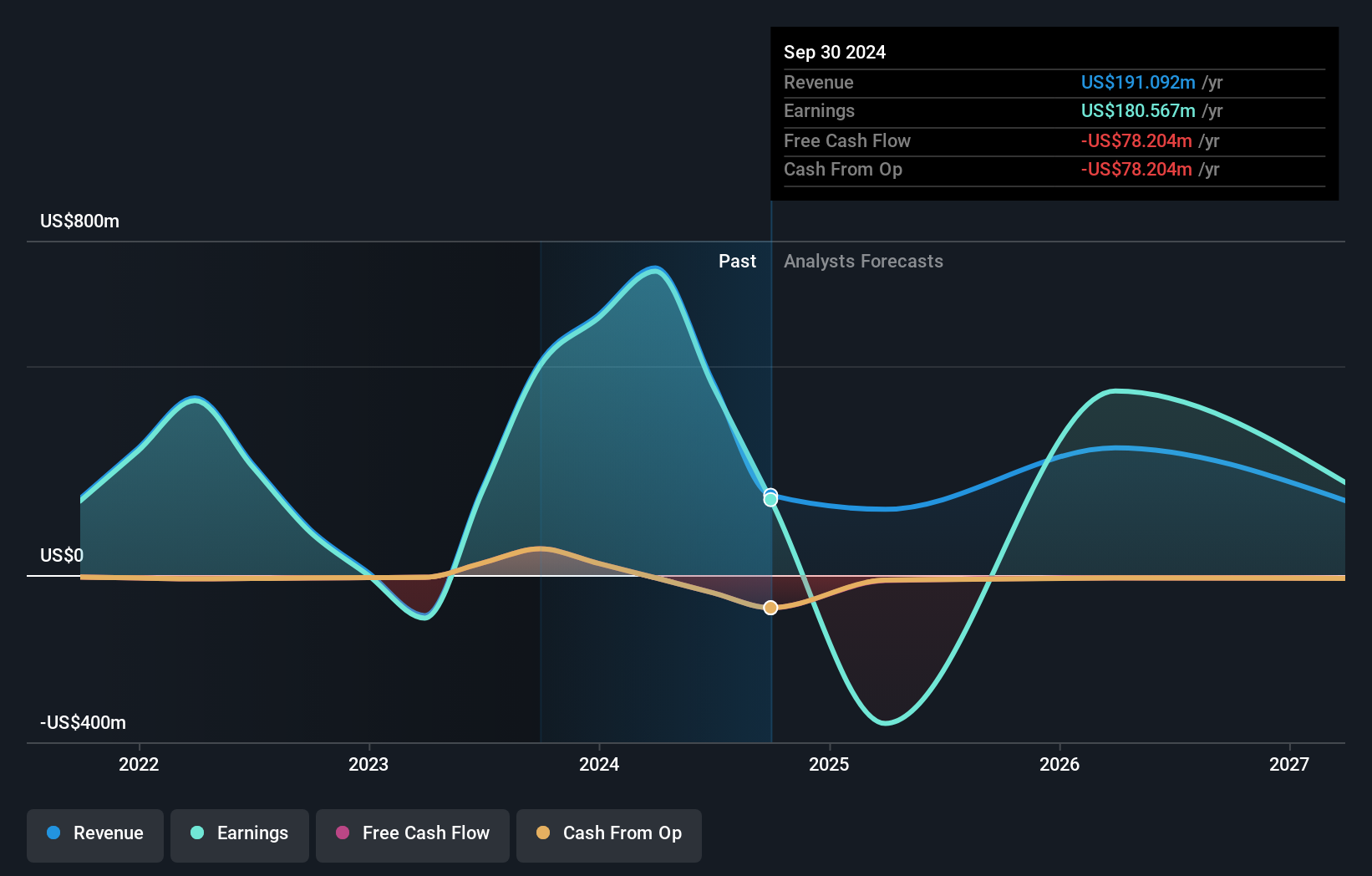

Yellow Cake (AIM:YCA)

Simply Wall St Value Rating: ★★★★★★

Overview: Yellow Cake plc operates in the uranium sector with a market cap of £1.14 billion.

Operations: Yellow Cake plc generates revenue primarily from holding U3O8 for long-term capital appreciation, amounting to $735.02 million.

Yellow Cake, a small cap in the UK market, has shown significant progress recently. The company reported revenue of US$735.02 million for the year ending March 31, 2024, compared to negative revenue of US$96.9 million previously. Net income surged to US$727.01 million from a net loss of US$102.94 million last year. Despite shareholder dilution over the past year, it trades at a favorable price-to-earnings ratio of 2.1x against the UK market's 16.5x and boasts high-quality non-cash earnings.

- Dive into the specifics of Yellow Cake here with our thorough health report.

Evaluate Yellow Cake's historical performance by accessing our past performance report.

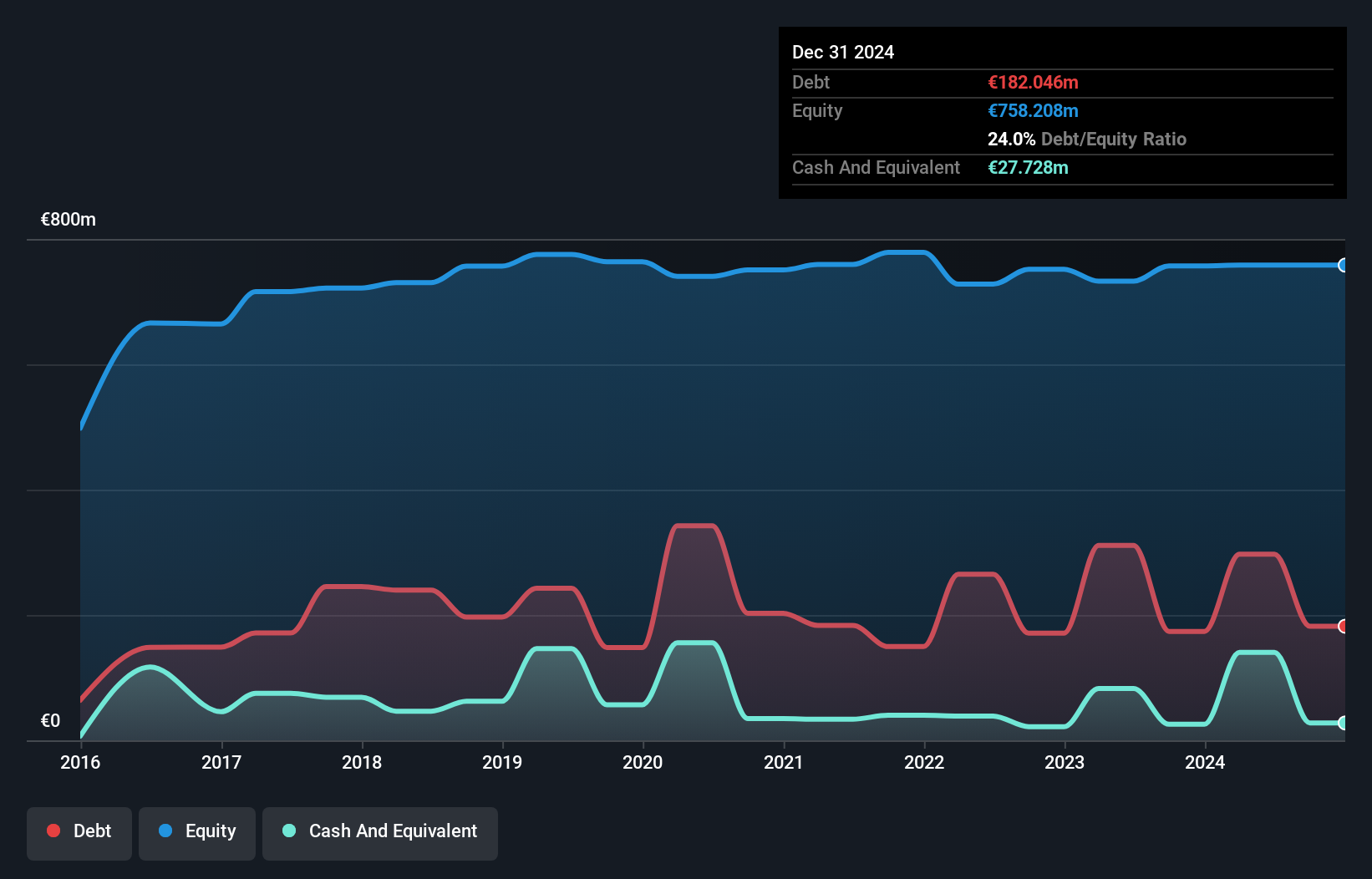

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cairn Homes plc, with a market cap of £980.21 million, operates as a home and community builder in Ireland.

Operations: Cairn Homes generates revenue primarily from building and property development, amounting to €813.40 million. The company has a market cap of £980.21 million.

Cairn Homes, a notable player in the UK housing market, reported strong earnings growth of 49.5% over the past year, significantly outpacing the Consumer Durables industry average. The company’s net debt to equity ratio stands at a satisfactory 20.7%, and its interest payments are well covered by EBIT with a 9.5x coverage. Recently, Cairn repurchased shares worth €70 million and announced an interim dividend of €0.038 per share, reflecting robust financial health and shareholder returns.

- Click here to discover the nuances of Cairn Homes with our detailed analytical health report.

Examine Cairn Homes' past performance report to understand how it has performed in the past.

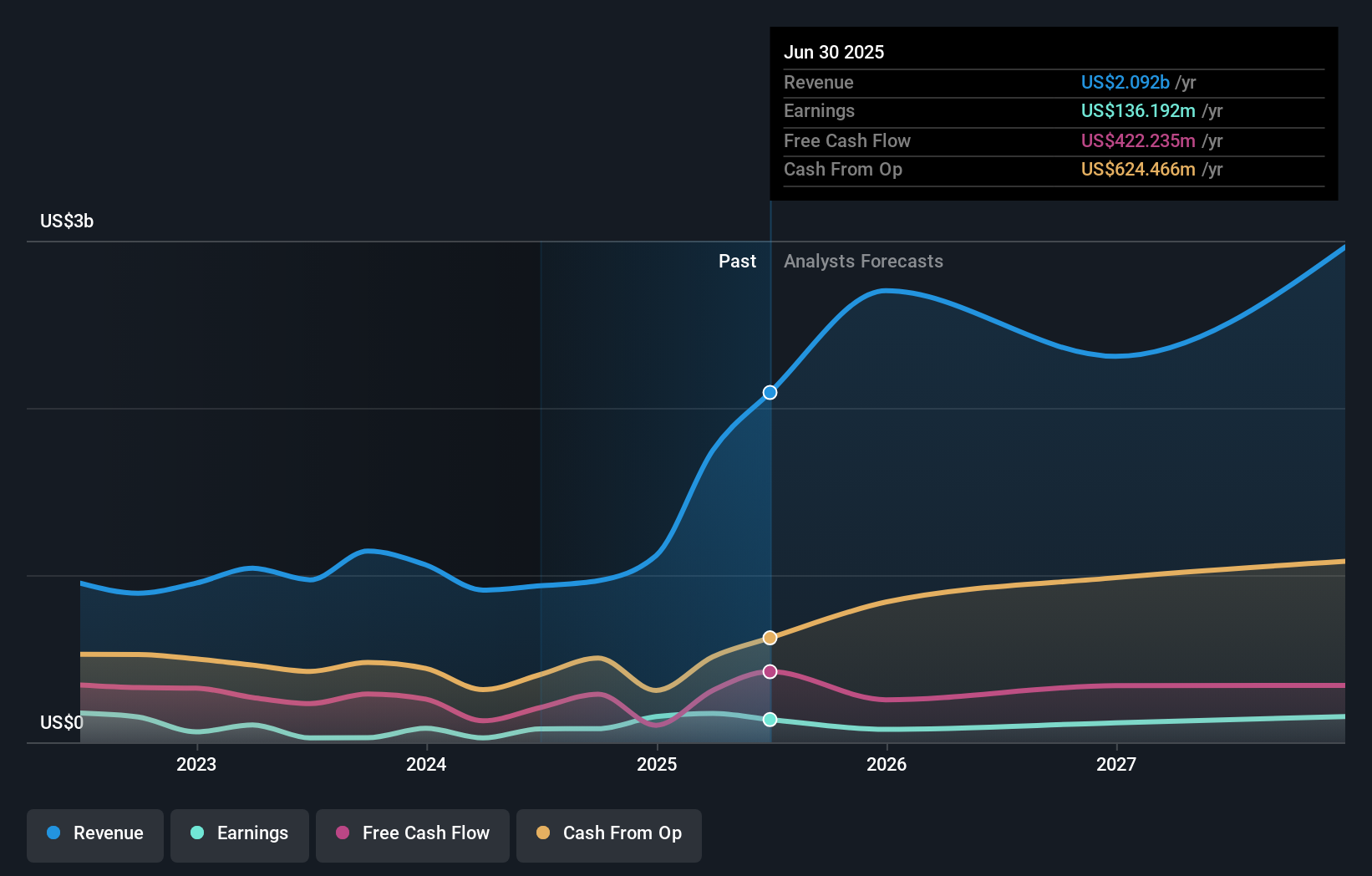

Seplat Energy (LSE:SEPL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Seplat Energy Plc is involved in oil and gas exploration, production, and gas processing activities across Nigeria, the Bahamas, Italy, Switzerland, Barbados, and England with a market cap of £1.11 billion.

Operations: Seplat Energy generates revenue primarily from oil ($815.03 million) and gas ($120.87 million). The company's net profit margin is 14.5%.

Seplat Energy, a mid-sized player in the UK oil and gas sector, saw its earnings grow by 207.6% over the past year, significantly outperforming the industry average of -56%. The company's EBIT covers interest payments 5.8 times over, indicating strong financial health. Seplat's net debt to equity ratio stands at a satisfactory 20.6%, though it has increased from 20.6% to 41.5% over five years. Recent production averaged 48,407 boepd for H1 2024, down from last year's 50,805 boepd but sales rose to US$241.82 million in Q2 compared to US$216 million a year ago.

- Delve into the full analysis health report here for a deeper understanding of Seplat Energy.

Review our historical performance report to gain insights into Seplat Energy's's past performance.

Key Takeaways

- Take a closer look at our UK Undiscovered Gems With Strong Fundamentals list of 80 companies by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:YCA

Flawless balance sheet and fair value.