Advertisement

- United Kingdom

- /

- Energy Services

- /

- LSE:GMS

Gulf Marine Services PLC's (LON:GMS) Price Is Right But Growth Is Lacking After Shares Rocket 26%

Despite an already strong run, Gulf Marine Services PLC (LON:GMS) shares have been powering on, with a gain of 26% in the last thirty days. The last 30 days were the cherry on top of the stock's 387% gain in the last year, which is nothing short of spectacular.

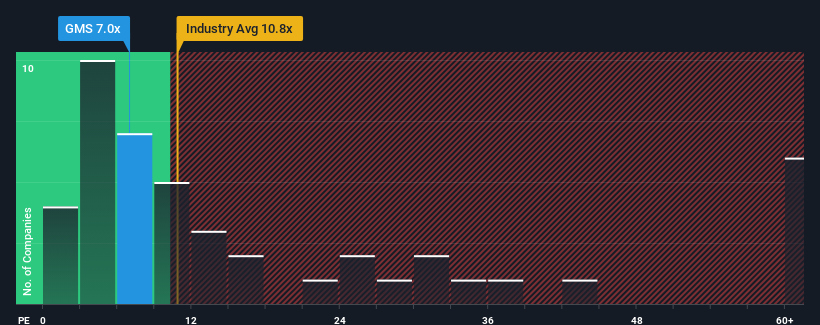

In spite of the firm bounce in price, given about half the companies in the United Kingdom have price-to-earnings ratios (or "P/E's") above 17x, you may still consider Gulf Marine Services as a highly attractive investment with its 7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been pleasing for Gulf Marine Services as its earnings have risen in spite of the market's earnings going into reverse. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Gulf Marine Services

Is There Any Growth For Gulf Marine Services?

The only time you'd be truly comfortable seeing a P/E as depressed as Gulf Marine Services' is when the company's growth is on track to lag the market decidedly.

Taking a look back first, we see that the company grew earnings per share by an impressive 63% last year. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 4.2% per year during the coming three years according to the three analysts following the company. That's shaping up to be materially lower than the 13% per annum growth forecast for the broader market.

In light of this, it's understandable that Gulf Marine Services' P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Gulf Marine Services' P/E

Gulf Marine Services' recent share price jump still sees its P/E sitting firmly flat on the ground. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Gulf Marine Services' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Gulf Marine Services (1 is potentially serious!) that you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:GMS

Gulf Marine Services

Operates self-propelled self-elevating support vessels (SESVs) in the United Arab Emirates, the Kingdom of Saudi Arabia, Qatar, and Europe.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor