Advertisement

- United Kingdom

- /

- Basic Materials

- /

- LSE:BREE

UK Penny Stocks With Market Caps Under £2B To Consider

Simply Wall St

Reviewed by Simply Wall St

The UK stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting global economic pressures. In such a climate, investors often seek opportunities in lesser-known areas of the market that may offer growth potential despite broader uncertainties. Penny stocks, while an older term, still represent intriguing investment prospects when they are backed by strong financials and fundamentals.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Rewards & Risks |

| Croma Security Solutions Group (AIM:CSSG) | £0.84 | £11.57M | ✅ 3 ⚠️ 3 View Analysis > |

| Ultimate Products (LSE:ULTP) | £0.72 | £60.67M | ✅ 4 ⚠️ 3 View Analysis > |

| LSL Property Services (LSE:LSL) | £2.95 | £304.36M | ✅ 5 ⚠️ 1 View Analysis > |

| Warpaint London (AIM:W7L) | £3.98 | £321.53M | ✅ 4 ⚠️ 3 View Analysis > |

| Foresight Group Holdings (LSE:FSG) | £3.955 | £446M | ✅ 4 ⚠️ 1 View Analysis > |

| Polar Capital Holdings (AIM:POLR) | £4.085 | £393.78M | ✅ 3 ⚠️ 2 View Analysis > |

| Impax Asset Management Group (AIM:IPX) | £1.71 | £218.49M | ✅ 2 ⚠️ 3 View Analysis > |

| Begbies Traynor Group (AIM:BEG) | £0.99 | £157.89M | ✅ 4 ⚠️ 2 View Analysis > |

| QinetiQ Group (LSE:QQ.) | £4.22 | £2.31B | ✅ 4 ⚠️ 1 View Analysis > |

| Van Elle Holdings (AIM:VANL) | £0.39 | £42.2M | ✅ 5 ⚠️ 2 View Analysis > |

Click here to see the full list of 398 stocks from our UK Penny Stocks screener.

Let's review some notable picks from our screened stocks.

Impax Asset Management Group (AIM:IPX)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Impax Asset Management Group Plc is a publicly owned investment manager with a market cap of £218.49 million.

Operations: The company generates revenue of £170.11 million from its investment management operations.

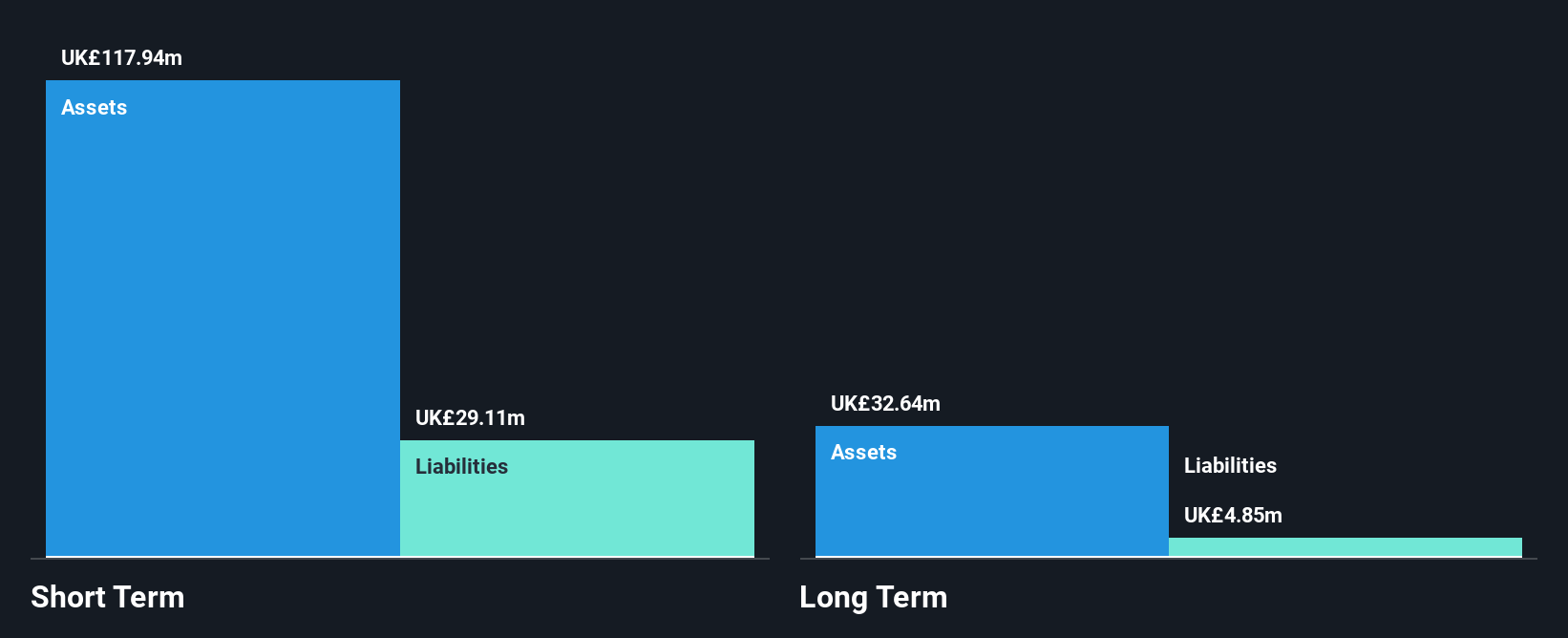

Market Cap: £218.49M

Impax Asset Management Group, with a market cap of £218.49 million, stands out for its strong financial structure as it operates debt-free and has short-term assets (£147.2M) comfortably covering liabilities. Despite high-quality earnings and a robust return on equity (27.8%), the company faces challenges with declining earnings forecasts over the next three years and recent negative earnings growth (-7%). The dividend yield is high at 16.14%, though not well covered by earnings, raising sustainability concerns. Additionally, while trading significantly below estimated fair value, its share price remains volatile compared to peers in the UK market.

- Click here and access our complete financial health analysis report to understand the dynamics of Impax Asset Management Group.

- Explore Impax Asset Management Group's analyst forecasts in our growth report.

Volex (AIM:VLX)

Simply Wall St Financial Health Rating: ★★★★☆☆

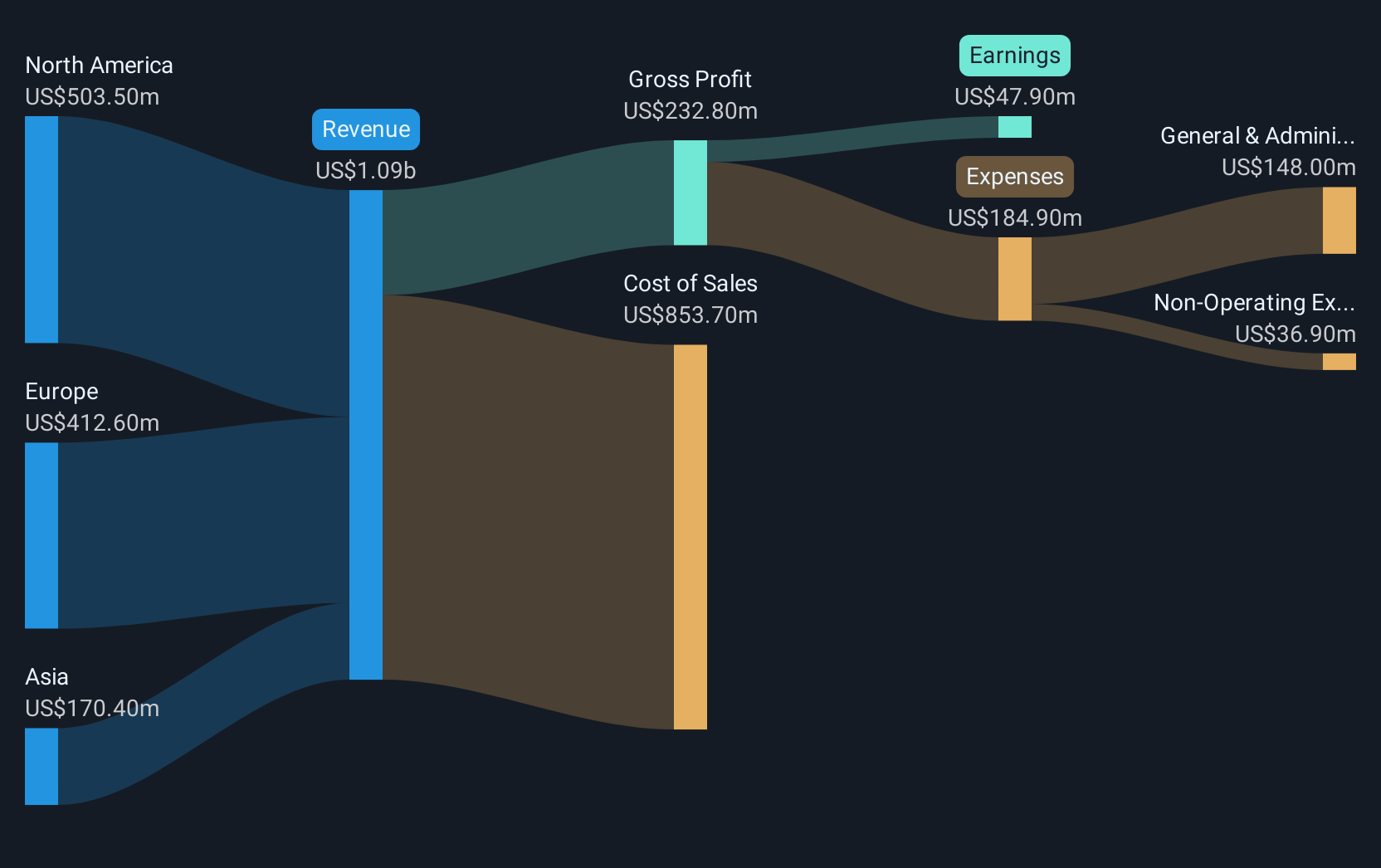

Overview: Volex plc manufactures and sells power and data cables across North America, Europe, and Asia with a market cap of £494.78 million.

Operations: The company generates revenue from three key regions: $197.3 million in Asia, $421.2 million in Europe, and $415 million in North America.

Market Cap: £494.78M

Volex plc, with a market cap of £494.78 million, is navigating the penny stock landscape with both opportunities and challenges. The company has experienced strong earnings growth at 22.1% over the past year, surpassing industry averages, and forecasts suggest continued profit expansion at 11.9% annually. Despite trading below fair value estimates and having well-covered interest payments by EBIT (3.8x), Volex's high net debt to equity ratio (42.9%) raises caution about its financial leverage. Recent guidance indicates robust revenue growth expectations for 2025; however, ongoing patent litigation poses potential risks to its operations in key markets like North America.

- Click here to discover the nuances of Volex with our detailed analytical financial health report.

- Gain insights into Volex's outlook and expected performance with our report on the company's earnings estimates.

Breedon Group (LSE:BREE)

Simply Wall St Financial Health Rating: ★★★★☆☆

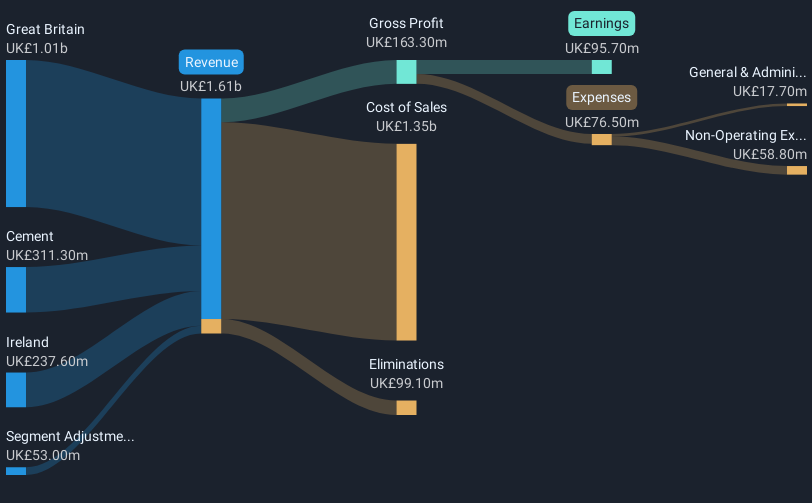

Overview: Breedon Group plc, with a market cap of £1.58 billion, operates in the quarrying, manufacture, and sale of construction materials and building products primarily in the United Kingdom and internationally.

Operations: The company's revenue is derived from its operations in Cement (£309.2 million), Ireland (£233.4 million), Great Britain (£997.4 million), and the United States (£132.5 million).

Market Cap: £1.58B

Breedon Group plc, with a market cap of £1.58 billion, presents a mixed picture in the penny stock arena. Recent acquisitions contributed to revenue growth in Q1 2025 despite weather-related challenges, yet net income decreased from £105.5 million to £96.2 million year-over-year. The company's earnings have grown significantly over the past five years but faced negative growth last year, complicating comparisons with industry averages. While Breedon's interest payments are well-covered by EBIT and its debt is satisfactorily managed by cash flow, concerns arise from its low return on equity and unstable dividend history amidst trading below fair value estimates.

- Get an in-depth perspective on Breedon Group's performance by reading our balance sheet health report here.

- Examine Breedon Group's earnings growth report to understand how analysts expect it to perform.

Summing It All Up

- Embark on your investment journey to our 398 UK Penny Stocks selection here.

- Looking For Alternative Opportunities? The end of cancer? These 23 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Breedon Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:BREE

Breedon Group

Engages in the quarrying, manufacture, and sale of construction materials and building products primarily in the United Kingdom and internationally.

Very undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor