Advertisement

- United Kingdom

- /

- Hospitality

- /

- AIM:COM

Health Check: How Prudently Does Comptoir Group (LON:COM) Use Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Comptoir Group PLC (LON:COM) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Comptoir Group

What Is Comptoir Group's Net Debt?

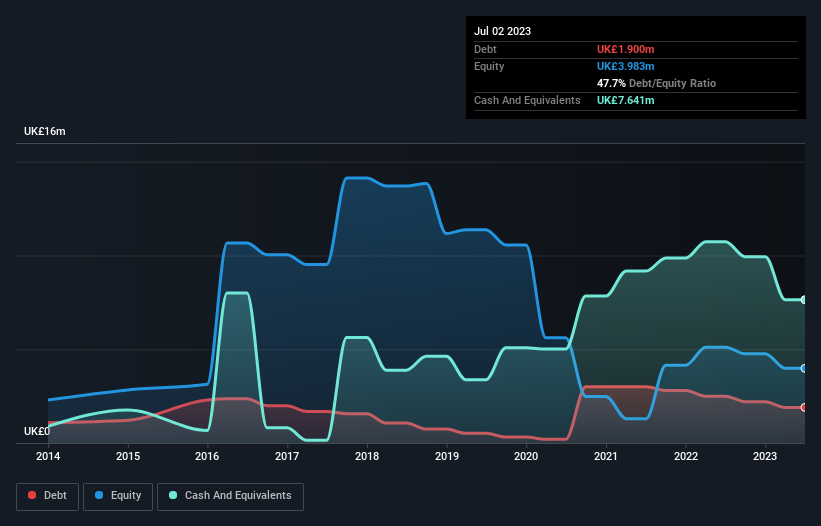

As you can see below, Comptoir Group had UK£1.90m of debt at July 2023, down from UK£2.50m a year prior. But it also has UK£7.64m in cash to offset that, meaning it has UK£5.74m net cash.

How Strong Is Comptoir Group's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Comptoir Group had liabilities of UK£7.56m due within 12 months and liabilities of UK£17.4m due beyond that. Offsetting these obligations, it had cash of UK£7.64m as well as receivables valued at UK£1.38m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£15.9m.

The deficiency here weighs heavily on the UK£9.20m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Comptoir Group would likely require a major re-capitalisation if it had to pay its creditors today. Comptoir Group boasts net cash, so it's fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Comptoir Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Comptoir Group wasn't profitable at an EBIT level, but managed to grow its revenue by 6.0%, to UK£31m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Comptoir Group?

Although Comptoir Group had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of UK£742k. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. Given the lack of transparency around future revenue (and cashflow), we're nervous about this one, until it makes its first big sales. To us, it is a high risk play. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Comptoir Group you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:COM

Comptoir Group

Owns and operates restaurants under the Comptoir Libanais and Shawa brand names in the United Kingdom.

Good value with mediocre balance sheet.

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on Evaxion ·

The "AI-Immunology" Asymmetric Opportunity – Validated by Merck (MSD)

Fair Value:US$15.8565.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on POET Technologies ·

The Hidden Gem of AI Hardware – Solving the Data Center Bottleneck

Fair Value:US$17.3773.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Recursion Pharmaceuticals ·

Moving from "Science Fiction" to "Science Fact" – A Bullish Valuation Case

Fair Value:US$12.4965.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

110 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

943 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative