Advertisement

- United Kingdom

- /

- Luxury

- /

- LSE:DOCS

Investors one-year losses continue as Dr. Martens (LON:DOCS) dips a further 3.2% this week, earnings continue to decline

Dr. Martens plc (LON:DOCS) shareholders should be happy to see the share price up 18% in the last month. But that doesn't change the reality of under-performance over the last twelve months. The cold reality is that the stock has dropped 46% in one year, under-performing the market.

Since Dr. Martens has shed UK£48m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

See our latest analysis for Dr. Martens

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

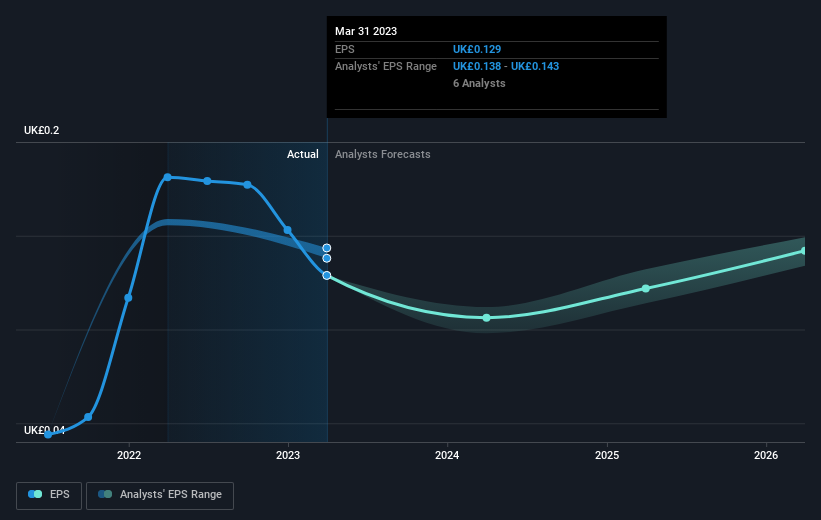

Unhappily, Dr. Martens had to report a 29% decline in EPS over the last year. This reduction in EPS is not as bad as the 46% share price fall. Unsurprisingly, given the lack of EPS growth, the market seems to be more cautious about the stock. The less favorable sentiment is reflected in its current P/E ratio of 11.03.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

It's good to see that there was some significant insider buying in the last three months. That's a positive. That said, we think earnings and revenue growth trends are even more important factors to consider. This free interactive report on Dr. Martens' earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. We note that for Dr. Martens the TSR over the last 1 year was -43%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

A Different Perspective

Given that the market gained 1.5% in the last year, Dr. Martens shareholders might be miffed that they lost 43% (even including dividends). While the aim is to do better than that, it's worth recalling that even great long-term investments sometimes underperform for a year or more. The share price decline has continued throughout the most recent three months, down 13%, suggesting an absence of enthusiasm from investors. Basically, most investors should be wary of buying into a poor-performing stock, unless the business itself has clearly improved. It's always interesting to track share price performance over the longer term. But to understand Dr. Martens better, we need to consider many other factors. For example, we've discovered 3 warning signs for Dr. Martens (1 is a bit concerning!) that you should be aware of before investing here.

Dr. Martens is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on British exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:DOCS

Dr. Martens

Engages in the design, development, procurement, marketing, sale, and distribution of footwear.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

LE

lexdrew1 on GE Vernova ·

GE Vernova revenue will grow by 13% with a future PE of 64.7x

Fair Value:US$824.5724.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GI

Gil263 on Butterfly Network ·

A buy recommendation

Fair Value:US$1.872.2% overvalued

2 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1157.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8685.8% undervalued

76 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative