- United Kingdom

- /

- Consumer Durables

- /

- LSE:BWY

Should You Investigate Bellway p.l.c. (LON:BWY) At UK£23.94?

Bellway p.l.c. (LON:BWY), is not the largest company out there, but it saw a double-digit share price rise of over 10% in the past couple of months on the LSE. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, could the stock still be trading at a relatively cheap price? Let’s take a look at Bellway’s outlook and value based on the most recent financial data to see if the opportunity still exists.

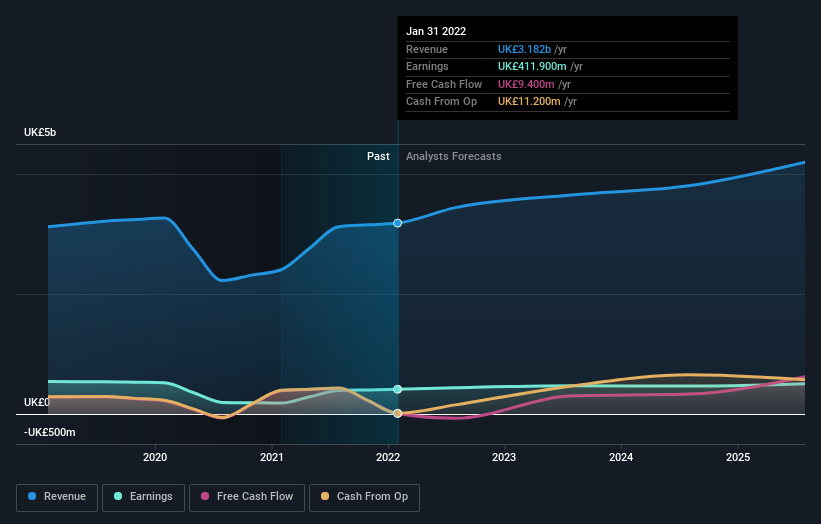

Check out our latest analysis for Bellway

Is Bellway Still Cheap?

According to my price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average, the stock price seems to be justfied. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that Bellway’s ratio of 7.17x is trading slightly below its industry peers’ ratio of 9.46x, which means if you buy Bellway today, you’d be paying a decent price for it. And if you believe Bellway should be trading in this range, then there isn’t much room for the share price to grow beyond the levels of other industry peers over the long-term. So, is there another chance to buy low in the future? Given that Bellway’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us an opportunity to buy later on. This is based on its high beta, which is a good indicator for share price volatility.

Can we expect growth from Bellway?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by a double-digit 17% over the next couple of years, the outlook is positive for Bellway. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What This Means For You

Are you a shareholder? BWY’s optimistic future growth appears to have been factored into the current share price, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the track record of its management team. Have these factors changed since the last time you looked at BWY? Will you have enough conviction to buy should the price fluctuate below the industry PE ratio?

Are you a potential investor? If you’ve been keeping an eye on BWY, now may not be the most advantageous time to buy, given it is trading around industry price multiples. However, the optimistic forecast is encouraging for BWY, which means it’s worth further examining other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

So while earnings quality is important, it's equally important to consider the risks facing Bellway at this point in time. At Simply Wall St, we found 1 warning sign for Bellway and we think they deserve your attention.

If you are no longer interested in Bellway, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Valuation is complex, but we're here to simplify it.

Discover if Bellway might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BWY

Good value with reasonable growth potential.