Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

Barratt Developments plc's (LON:BDEV) Share Price Is Matching Sentiment Around Its Earnings

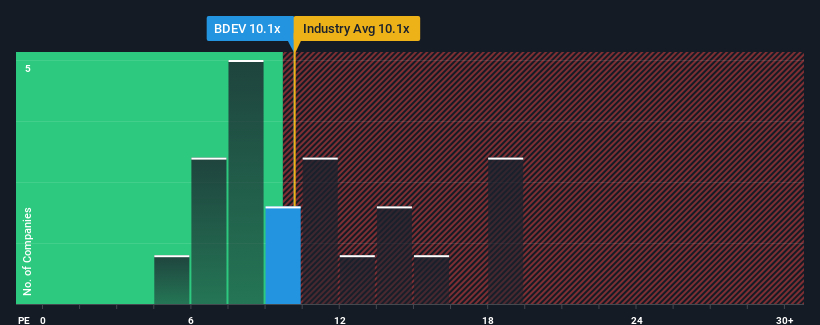

Barratt Developments plc's (LON:BDEV) price-to-earnings (or "P/E") ratio of 10.1x might make it look like a buy right now compared to the market in the United Kingdom, where around half of the companies have P/E ratios above 16x and even P/E's above 29x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Barratt Developments as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Barratt Developments

Is There Any Growth For Barratt Developments?

In order to justify its P/E ratio, Barratt Developments would need to produce sluggish growth that's trailing the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 5.3% last year. Pleasingly, EPS has also lifted 39% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings growth is heading into negative territory, declining 8.0% each year over the next three years. Meanwhile, the broader market is forecast to expand by 12% per year, which paints a poor picture.

In light of this, it's understandable that Barratt Developments' P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Barratt Developments' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for Barratt Developments you should be aware of, and 1 of them is potentially serious.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.550.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58015.7% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8813.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

GE

Germaine on Sern Kou Resources Berhad ·

Sern Kou Resource Stands to Benefit from Supply Chain Tightness and Pricing Power

Fair Value:RM 0.4972.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HM

Hmdlsk on Circus ·

Circus SE's AI-driven food systems will revolutionize global food service

Fair Value:€3072.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Kuya Silver ·

Peru/Canada 15 Baggers Near-Producer Silver Play

Fair Value:CA$16.2294.0% undervalued

2 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.8% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5727.9% undervalued

1377 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GT

GT1 on Gulf Keystone Petroleum ·

Have been in and out of this one and Genel for years. I think that delayed and non payments are a bi...

0

|0