Advertisement

- United Kingdom

- /

- Machinery

- /

- LSE:MGAM

Exploring 3 Undervalued Small Caps In The European Market With Insider Action

Simply Wall St

Reviewed by Simply Wall St

The European market has recently experienced fluctuations, with the pan-European STOXX Europe 600 Index ending 1.92% lower amid escalating trade tensions, although a rebound followed after a temporary delay in U.S. tariffs. In this environment of heightened volatility and economic uncertainty, identifying small-cap stocks that are potentially undervalued can be particularly appealing to investors seeking opportunities for growth amidst broader market challenges.

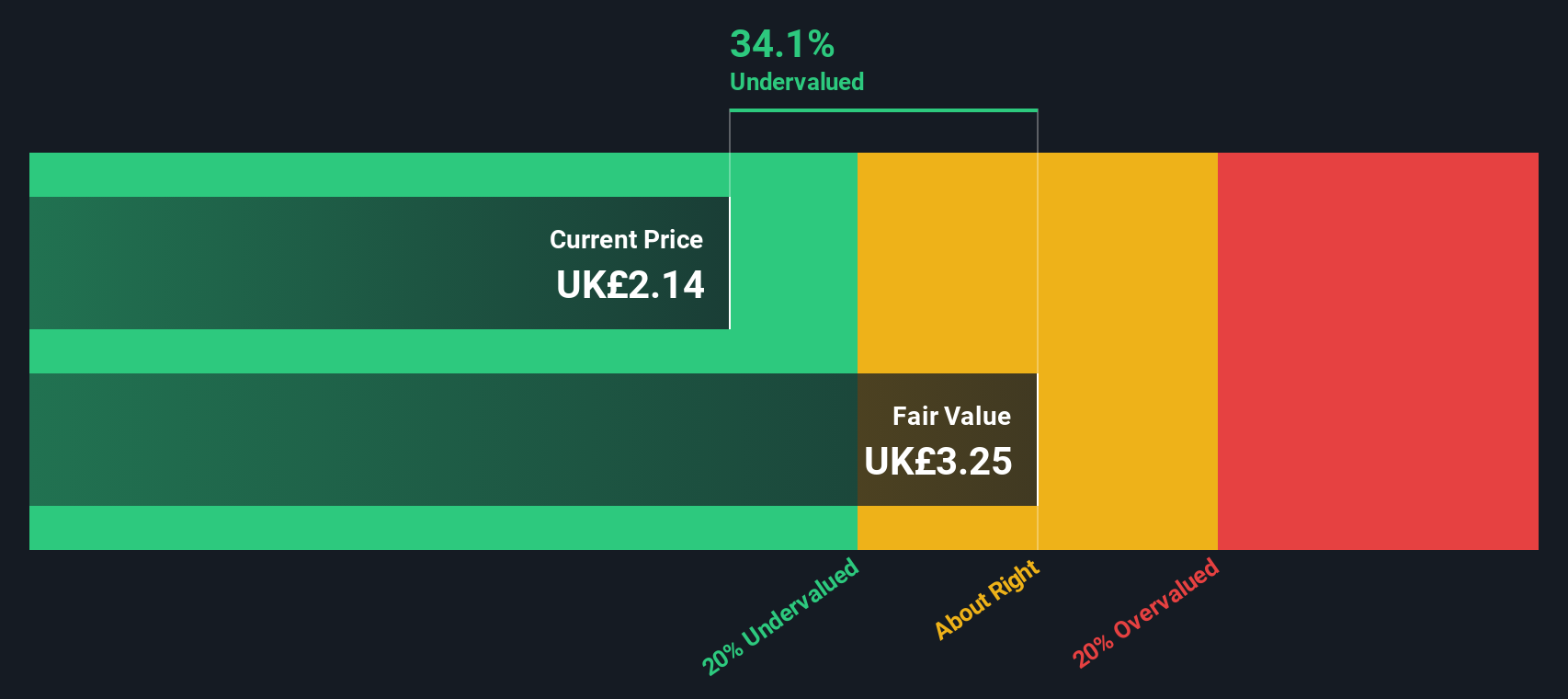

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Morgan Advanced Materials | 10.3x | 0.5x | 44.13% | ★★★★★★ |

| Tristel | 24.7x | 3.5x | 34.68% | ★★★★★★ |

| Bytes Technology Group | 22.7x | 5.8x | 8.35% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 28.24% | ★★★★★☆ |

| Savills | 23.1x | 0.5x | 43.97% | ★★★★☆☆ |

| Norcros | 22.9x | 0.5x | 31.44% | ★★★☆☆☆ |

| FRP Advisory Group | 12.2x | 2.2x | 11.91% | ★★★☆☆☆ |

| Italmobiliare | 10.6x | 1.4x | -248.61% | ★★★☆☆☆ |

| Arendals Fossekompani | 21.2x | 1.6x | 47.36% | ★★★☆☆☆ |

| Exsitec Holding | 23.5x | 1.7x | 47.33% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

James Halstead (AIM:JHD)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: James Halstead is a company engaged in the manufacture and distribution of flooring products, with a market cap of £1.05 billion.

Operations: The company generates revenue primarily from the manufacture and distribution of flooring products, with recent figures showing £268.52 million in revenue. The cost structure includes significant expenses for cost of goods sold (COGS) at £153.76 million, leading to a gross profit of £114.76 million as of the latest period ending December 31, 2024. Notably, the net income margin has recently been recorded at 15.79%.

PE: 13.7x

James Halstead, a smaller European company, recently increased its interim dividend by 10% to 2.75 pence per share, signaling confidence in its financial health. Despite sales dipping to £130.09 million for the half year ending December 2024 from £136.45 million the previous year, net income rose slightly to £20.97 million. Insider confidence is evident with recent share purchases over the past few months, suggesting potential growth as earnings are projected to grow annually by nearly 4%.

- Get an in-depth perspective on James Halstead's performance by reading our valuation report here.

Review our historical performance report to gain insights into James Halstead's's past performance.

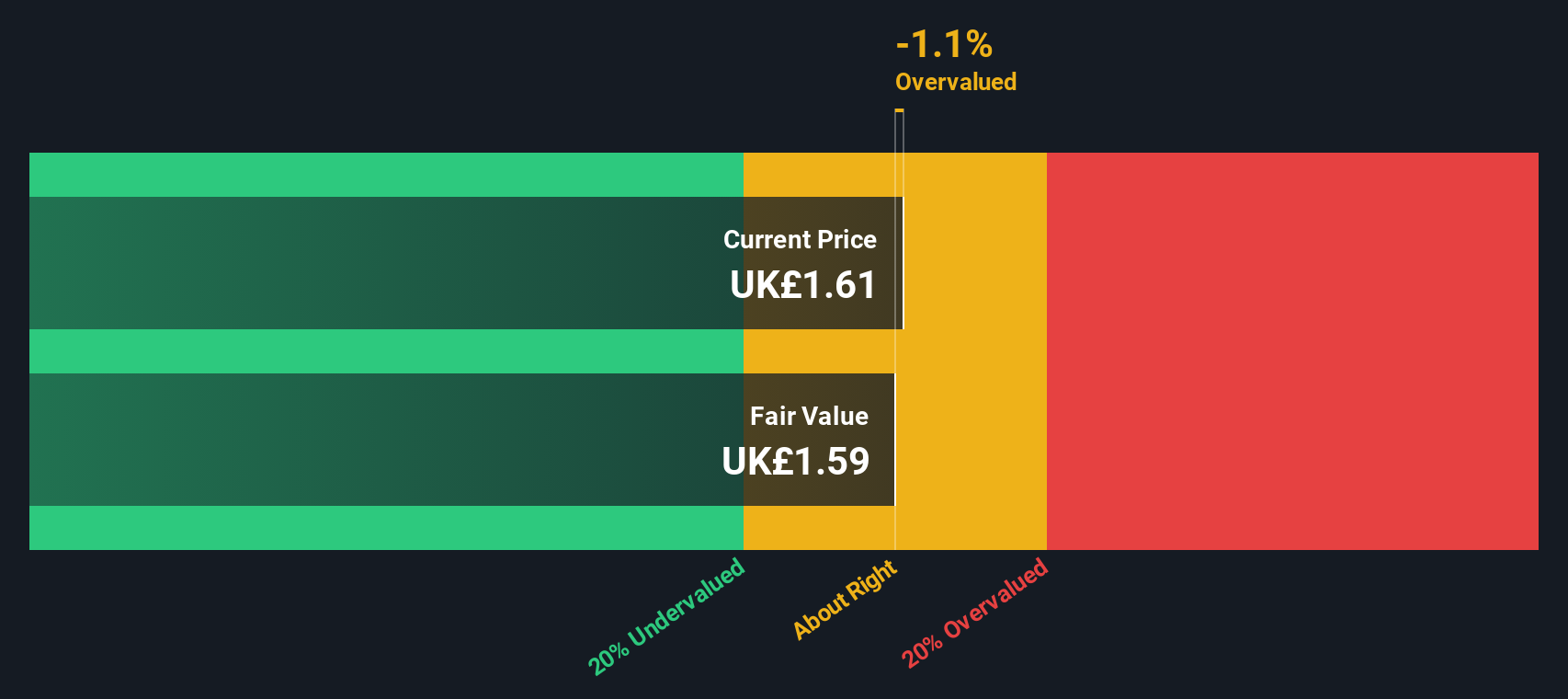

Morgan Advanced Materials (LSE:MGAM)

Simply Wall St Value Rating: ★★★★★★

Overview: Morgan Advanced Materials operates in the thermal products and performance carbon sectors, with additional involvement in technical ceramics, and has a market capitalization of approximately £1.03 billion.

Operations: Morgan Advanced Materials generates revenue primarily from its Thermal Products (£419.90 million), Performance Carbon (£345.70 million), and Technical Ceramics (£337.80 million) segments. The company's cost of goods sold (COGS) consistently impacts its gross profit, which shows a declining trend with the most recent gross profit margin at 11.79%. Operating expenses have been decreasing over time, reaching £2.3 million in the latest period, while non-operating expenses have fluctuated, recently recorded at £75.9 million.

PE: 10.3x

Morgan Advanced Materials, a smaller player in the European market, has shown signs of being undervalued. Despite reporting a slight decline in sales to £1.1 billion for 2024, net income increased to £50.3 million. The company completed a share buyback of 1,825,090 shares for £4.7 million between November and December 2024, reflecting strategic financial management amidst high debt levels and reliance on external borrowing. Upcoming leadership changes could influence its growth trajectory as earnings are projected to grow by nearly 20% annually.

- Navigate through the intricacies of Morgan Advanced Materials with our comprehensive valuation report here.

Understand Morgan Advanced Materials' track record by examining our Past report.

FastPartner (OM:FPAR A)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: FastPartner is a real estate company focused on property management across multiple regions, with a market capitalization of approximately SEK 10.53 billion.

Operations: The company's revenue streams are primarily derived from property management across three regions, with Region 1 contributing the highest at SEK 1.10 billion. The cost of goods sold (COGS) has been increasing over time, impacting the gross profit margin which fluctuated between 68.64% and 71.44% in recent periods. Operating expenses have remained relatively stable compared to revenue growth, while non-operating expenses have shown significant volatility, affecting net income outcomes significantly in recent years.

PE: 15.1x

FastPartner, a smaller player in the European market, recently reported improved financial results with fourth-quarter sales rising to SEK 566.2 million and a net income of SEK 159.2 million, reversing last year's loss. Their full-year performance also saw sales increase to SEK 2.29 billion and net income at SEK 648 million. Insider confidence is evident as a founder purchased 50,000 shares for approximately SEK 3.55 million in early February, indicating potential belief in future growth despite reliance on higher-risk external funding sources.

- Dive into the specifics of FastPartner here with our thorough valuation report.

Gain insights into FastPartner's historical performance by reviewing our past performance report.

Where To Now?

- Unlock our comprehensive list of 58 Undervalued European Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:MGAM

Morgan Advanced Materials

Manufactures and sells various carbon and ceramic products.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor