- United Kingdom

- /

- Trade Distributors

- /

- LSE:RS1

There's A Lot To Like About Electrocomponents' (LON:ECM) Upcoming UK£0.061 Dividend

Electrocomponents plc (LON:ECM) is about to trade ex-dividend in the next four days. This means that investors who purchase shares on or after the 7th of January will not receive the dividend, which will be paid on the 29th of January.

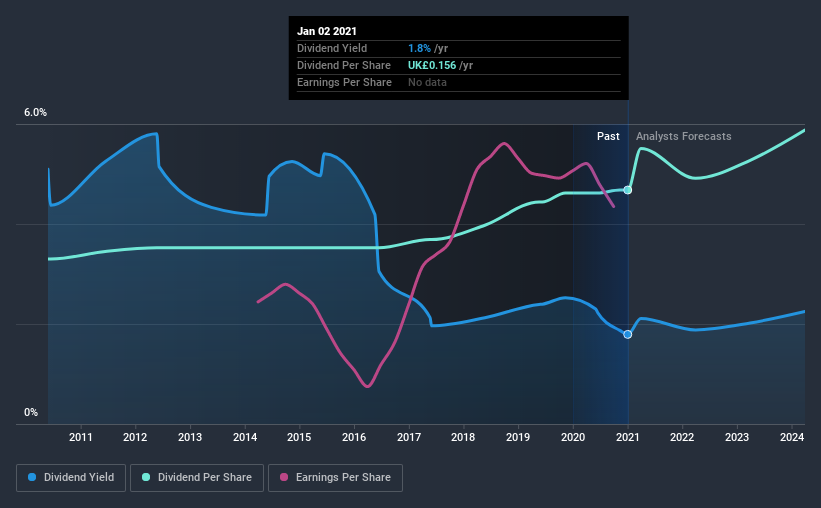

Electrocomponents's upcoming dividend is UK£0.061 a share, following on from the last 12 months, when the company distributed a total of UK£0.16 per share to shareholders. Calculating the last year's worth of payments shows that Electrocomponents has a trailing yield of 1.8% on the current share price of £8.705. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether Electrocomponents can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Electrocomponents

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Electrocomponents paid out 54% of its earnings to investors last year, a normal payout level for most businesses. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. What's good is that dividends were well covered by free cash flow, with the company paying out 18% of its cash flow last year.

It's positive to see that Electrocomponents's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings fall far enough, the company could be forced to cut its dividend. For this reason, we're glad to see Electrocomponents's earnings per share have risen 13% per annum over the last five years. Electrocomponents is paying out a bit over half its earnings, which suggests the company is striking a balance between reinvesting in growth, and paying dividends. Given the quick rate of earnings per share growth and current level of payout, there may be a chance of further dividend increases in the future.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, Electrocomponents has lifted its dividend by approximately 3.6% a year on average. It's good to see both earnings and the dividend have improved - although the former has been rising much quicker than the latter, possibly due to the company reinvesting more of its profits in growth.

To Sum It Up

Should investors buy Electrocomponents for the upcoming dividend? We like Electrocomponents's growing earnings per share and the fact that - while its payout ratio is around average - it paid out a lower percentage of its cash flow. It's a promising combination that should mark this company worthy of closer attention.

So while Electrocomponents looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. To help with this, we've discovered 1 warning sign for Electrocomponents that you should be aware of before investing in their shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Electrocomponents or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade RS Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:RS1

RS Group

Engages in the distribution of maintenance, repair, and operations products and service solutions in the United Kingdom, the United States, France, Germany, Italy, Mexico, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives