- United Kingdom

- /

- Trade Distributors

- /

- LSE:DPLM

Here's Why Diploma (LON:DPLM) Has Caught The Eye Of Investors

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

In contrast to all that, many investors prefer to focus on companies like Diploma (LON:DPLM), which has not only revenues, but also profits. While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

View our latest analysis for Diploma

Diploma's Earnings Per Share Are Growing

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That means EPS growth is considered a real positive by most successful long-term investors. Over the last three years, Diploma has grown EPS by 17% per year. That's a pretty good rate, if the company can sustain it.

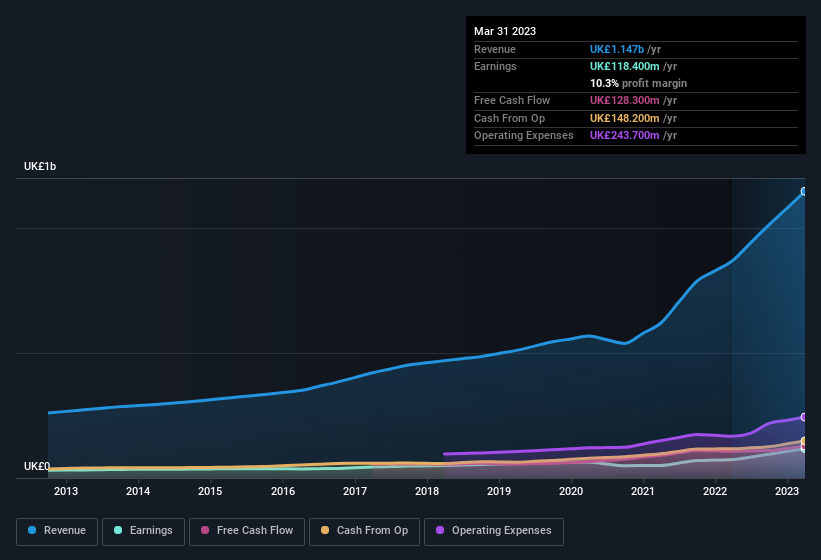

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Diploma maintained stable EBIT margins over the last year, all while growing revenue 32% to UK£1.1b. That's encouraging news for the company!

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Diploma's forecast profits?

Are Diploma Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

With strong conviction, Diploma insiders have stood united by refusing to sell shares over the last year. But more importantly, Chairman of the Board David Lowden spent UK£64k acquiring shares, doing so at an average price of UK£25.76. Strong buying like that could be a sign of opportunity.

Is Diploma Worth Keeping An Eye On?

One positive for Diploma is that it is growing EPS. That's nice to see. While some companies are struggling to grow EPS, Diploma seems free from that morose affliction. The cherry on top is that we have an insider buying shares. A further encouragement to keep an eye on this stock. You should always think about risks though. Case in point, we've spotted 1 warning sign for Diploma you should be aware of.

Keen growth investors love to see insider buying. Thankfully, Diploma isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:DPLM

Diploma

Supplies specialized technical products and services in the United Kingdom, Europe, North America, and internationally.

Moderate growth potential with acceptable track record.