- United Kingdom

- /

- Industrials

- /

- LSE:DCC

Shareholders Will Most Likely Find DCC plc's (LON:DCC) CEO Compensation Acceptable

Key Insights

- DCC to hold its Annual General Meeting on 11th of July

- Salary of UK£809.0k is part of CEO Donal Murphy's total remuneration

- The total compensation is similar to the average for the industry

- DCC's total shareholder return over the past three years was 6.0% while its EPS grew by 3.6% over the past three years

Under the guidance of CEO Donal Murphy, DCC plc (LON:DCC) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 11th of July. Based on our analysis of the data below, we think CEO compensation seems reasonable for now.

View our latest analysis for DCC

How Does Total Compensation For Donal Murphy Compare With Other Companies In The Industry?

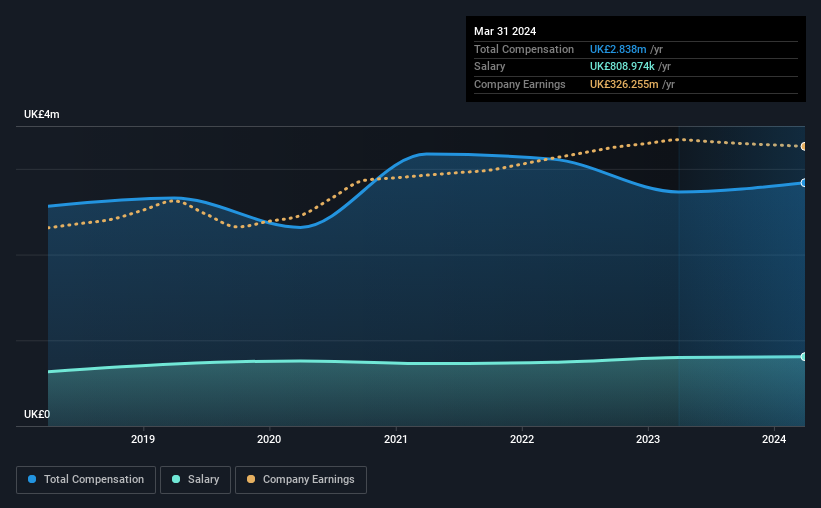

At the time of writing, our data shows that DCC plc has a market capitalization of UK£5.6b, and reported total annual CEO compensation of UK£2.8m for the year to March 2024. That's a fairly small increase of 3.9% over the previous year. While we always look at total compensation first, our analysis shows that the salary component is less, at UK£809k.

On examining similar-sized companies in the the United Kingdom Industrials industry with market capitalizations between UK£3.1b and UK£9.4b, we discovered that the median CEO total compensation of that group was UK£2.5m. This suggests that DCC remunerates its CEO largely in line with the industry average. What's more, Donal Murphy holds UK£1.2m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£809k | UK£800k | 29% |

| Other | UK£2.0m | UK£1.9m | 71% |

| Total Compensation | UK£2.8m | UK£2.7m | 100% |

Speaking on an industry level, nearly 58% of total compensation represents salary, while the remainder of 42% is other remuneration. In DCC's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

DCC plc's Growth

DCC plc's earnings per share (EPS) grew 3.6% per year over the last three years. In the last year, its revenue is down 11%.

We would argue that the lack of revenue growth in the last year is less than ideal, but the modest EPS growth gives us some relief. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has DCC plc Been A Good Investment?

DCC plc has not done too badly by shareholders, with a total return of 6.0%, over three years. It would be nice to see that metric improve in the future. In light of that, investors might probably want to see an improvement on their returns before they feel generous about increasing the CEO remuneration.

In Summary...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

Shareholders may want to check for free if DCC insiders are buying or selling shares.

Important note: DCC is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking to trade DCC, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:DCC

DCC

Engages in the sales, marketing, and distribution of carbon energy solutions worldwide.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives