Advertisement

- United Kingdom

- /

- Industrials

- /

- LSE:DCC

DCC plc Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

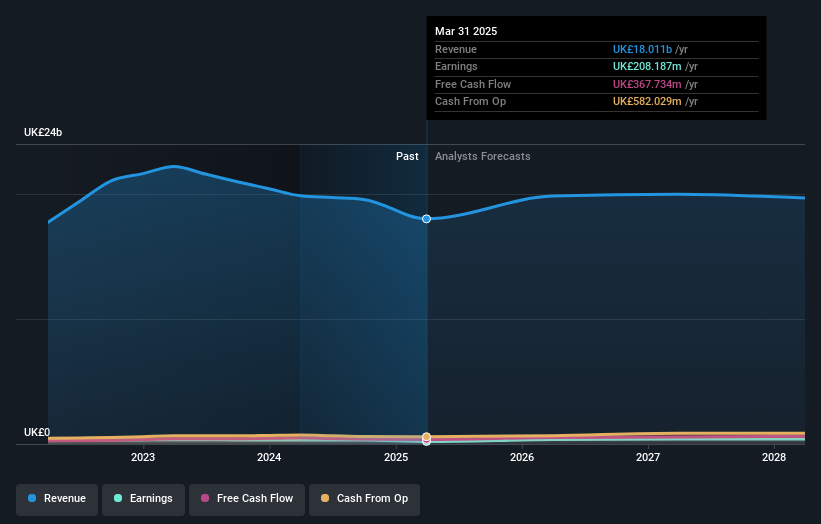

DCC plc (LON:DCC) just released its latest annual report and things are not looking great. It wasn't a great result overall - while revenue fell marginally short of analyst estimates at UK£18b, statutory earnings missed forecasts by an incredible 43%, coming in at just UK£2.08 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Our free stock report includes 2 warning signs investors should be aware of before investing in DCC. Read for free now.

Following the latest results, DCC's twelve analysts are now forecasting revenues of UK£19.8b in 2026. This would be a solid 10% improvement in revenue compared to the last 12 months. Per-share earnings are expected to shoot up 89% to UK£3.97. In the lead-up to this report, the analysts had been modelling revenues of UK£20.1b and earnings per share (EPS) of UK£4.03 in 2026. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

Check out our latest analysis for DCC

It will come as no surprise then, to learn that the consensus price target is largely unchanged at UK£66.70. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values DCC at UK£90.00 per share, while the most bearish prices it at UK£54.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of DCC'shistorical trends, as the 10% annualised revenue growth to the end of 2026 is roughly in line with the 9.2% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 6.3% per year. So although DCC is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at UK£66.70, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for DCC going out to 2028, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 2 warning signs for DCC you should know about.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:DCC

DCC

Engages in the sales, marketing, and distribution of carbon energy solutions in the Republic of Ireland, the United Kingdom, France, the United States, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor