Advertisement

- United Kingdom

- /

- Aerospace & Defense

- /

- AIM:PEN

Here's Why Pennant International Group (LON:PEN) Can Afford Some Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Pennant International Group plc (LON:PEN) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Our free stock report includes 3 warning signs investors should be aware of before investing in Pennant International Group. Read for free now.What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Pennant International Group Carry?

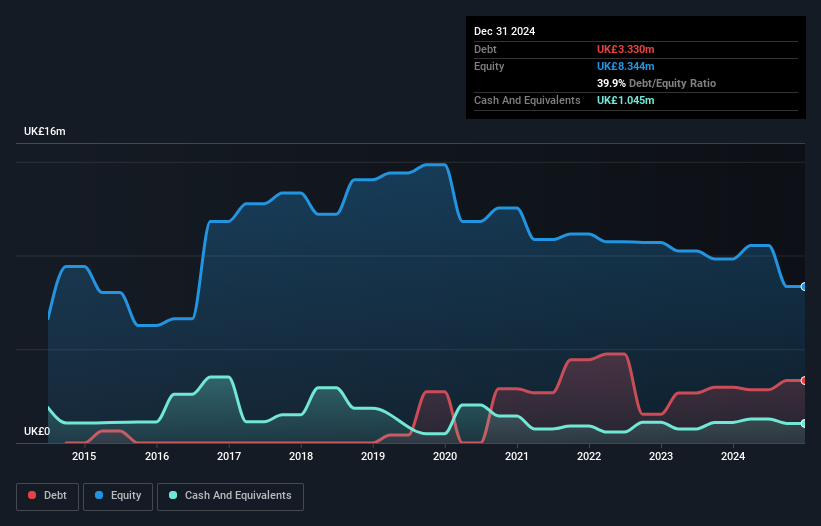

You can click the graphic below for the historical numbers, but it shows that as of December 2024 Pennant International Group had UK£3.33m of debt, an increase on UK£2.98m, over one year. On the flip side, it has UK£1.05m in cash leading to net debt of about UK£2.29m.

A Look At Pennant International Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Pennant International Group had liabilities of UK£7.03m due within 12 months and liabilities of UK£560.0k due beyond that. Offsetting this, it had UK£1.05m in cash and UK£2.58m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by UK£3.97m.

Pennant International Group has a market capitalization of UK£13.1m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Pennant International Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

View our latest analysis for Pennant International Group

Over 12 months, Pennant International Group made a loss at the EBIT level, and saw its revenue drop to UK£14m, which is a fall of 11%. That's not what we would hope to see.

Caveat Emptor

While Pennant International Group's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost UK£918k at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through UK£1.4m of cash over the last year. So in short it's a really risky stock. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Pennant International Group that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:PEN

Pennant International Group

Provides integrated training and support software solutions, products, and services in the United Kingdom, rest of Europe, North America, and Asia-Pacific region.

Good value with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor