Advertisement

- United Kingdom

- /

- Trade Distributors

- /

- AIM:FLO

What Do The Returns On Capital At Flowtech Fluidpower (LON:FLO) Tell Us?

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after briefly looking over the numbers, we don't think Flowtech Fluidpower (LON:FLO) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Flowtech Fluidpower is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

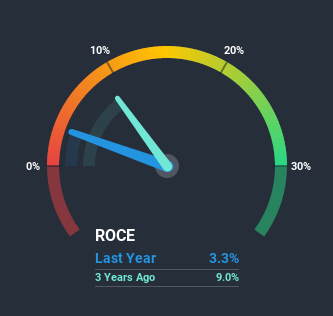

0.033 = UK£3.2m ÷ (UK£135m - UK£36m) (Based on the trailing twelve months to June 2020).

So, Flowtech Fluidpower has an ROCE of 3.3%. Ultimately, that's a low return and it under-performs the Trade Distributors industry average of 12%.

View our latest analysis for Flowtech Fluidpower

In the above chart we have measured Flowtech Fluidpower's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Flowtech Fluidpower here for free.

How Are Returns Trending?

When we looked at the ROCE trend at Flowtech Fluidpower, we didn't gain much confidence. Around five years ago the returns on capital were 9.0%, but since then they've fallen to 3.3%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 27%, which has impacted the ROCE. Without this increase, it's likely that ROCE would be even lower than 3.3%. While the ratio isn't currently too high, it's worth keeping an eye on this because if it gets particularly high, the business could then face some new elements of risk.Our Take On Flowtech Fluidpower's ROCE

We're a bit apprehensive about Flowtech Fluidpower because despite more capital being deployed in the business, returns on that capital and sales have both fallen. Investors must expect better things on the horizon though because the stock has risen 6.7% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

If you want to continue researching Flowtech Fluidpower, you might be interested to know about the 2 warning signs that our analysis has discovered.

While Flowtech Fluidpower isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade Flowtech Fluidpower, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About AIM:FLO

Flowtech Fluidpower

Distributes engineering components and assemblies in the areas of fluid power industry in the United Kingdom, rest of Europe, internationally.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor