It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in NatWest Group (LON:NWG). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide NatWest Group with the means to add long-term value to shareholders.

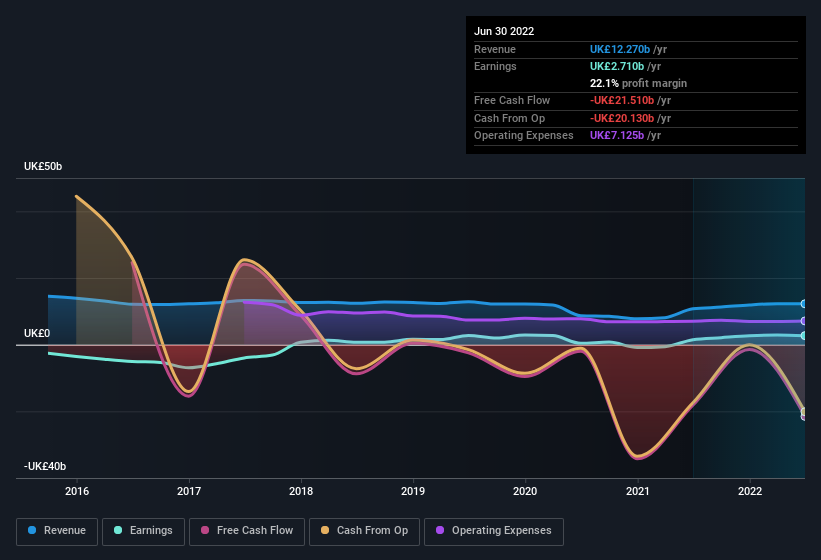

Check out our latest analysis for NatWest Group

NatWest Group's Earnings Per Share Are Growing

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. NatWest Group managed to grow EPS by 4.5% per year, over three years. That might not be particularly high growth, but it does show that per-share earnings are moving steadily in the right direction.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. Our analysis has highlighted that NatWest Group's revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. While we note NatWest Group achieved similar EBIT margins to last year, revenue grew by a solid 14% to UK£12b. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of NatWest Group's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are NatWest Group Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a UK£25b company like NatWest Group. But we are reassured by the fact they have invested in the company. As a matter of fact, their holding is valued at UK£12m. That's a lot of money, and no small incentive to work hard. While their ownership only accounts for 0.05%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. A brief analysis of the CEO compensation suggests they are. The median total compensation for CEOs of companies similar in size to NatWest Group, with market caps over UK£7.1b, is around UK£4.6m.

NatWest Group offered total compensation worth UK£3.6m to its CEO in the year to December 2021. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add NatWest Group To Your Watchlist?

One positive for NatWest Group is that it is growing EPS. That's nice to see. Earnings growth might be the main attraction for NatWest Group, but the fun does not stop there. Boasting both modest CEO pay and considerable insider ownership, you'd argue this one is worthy of the watchlist, at least. Still, you should learn about the 1 warning sign we've spotted with NatWest Group.

Although NatWest Group certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see insider buying, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if NatWest Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:NWG

NatWest Group

Provides banking and financial products and services to personal, commercial, corporate, and institutional customers in the United Kingdom and internationally.

Undervalued with excellent balance sheet.