Lloyds Banking Group (LSE:LLOY) stock has quietly delivered steady returns over the past year. Shares have climbed 90% in 12 months, easily outpacing the broader market and drawing attention from long-term investors.

Lloyds Banking Group’s rally has picked up real momentum in recent months, with a 7-day share price return of 10.35% and a year-to-date gain of 74.67%. After a solid stretch, the bank’s 1-year total shareholder return of 90% stands out as one of the strongest among major UK lenders. This suggests sentiment and growth expectations are building, not fading.

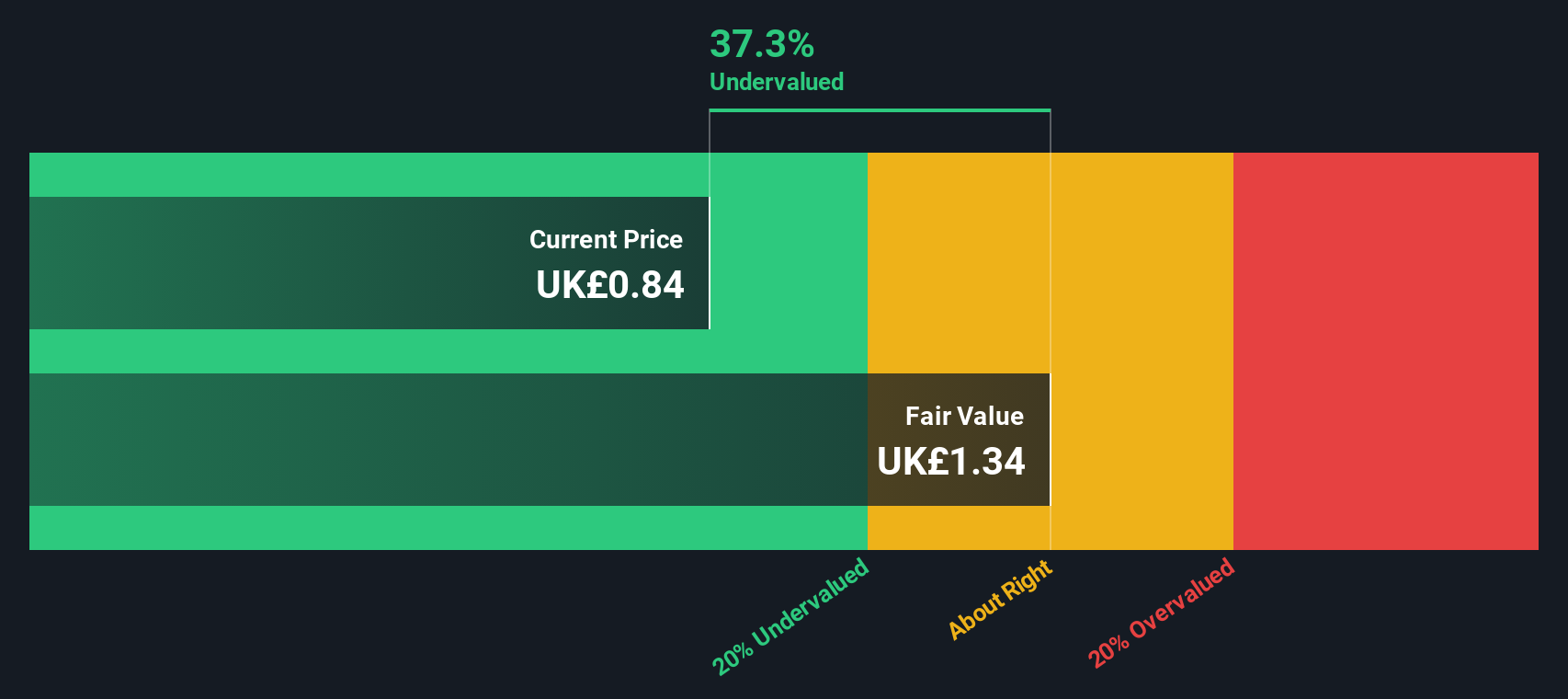

With shares near recent highs and investor optimism building, the big question now is whether Lloyds Banking Group stock remains undervalued or if the market has already priced in further growth from this point.

Advertisement

Most Popular Narrative: 2% Overvalued

Lloyds Banking Group’s last close price of £0.96 slightly overshoots the most-followed narrative’s fair value estimate of £0.94. The narrative pricing signals high conviction in stable future growth, but points to limited upside from here.

Lloyds' significant progress in digital transformation, including expanding mobile-first services for 21 million users, rolling out a new digital remortgage journey, and leveraging AI innovation, continues to drive operating cost reductions and enhance efficiency. This positions the company to support sustained long-term margin expansion and higher earnings.

Just how ambitious are analysts' expectations for Lloyds’ growth and profitability? The core narrative banks on powerful margin expansion and impressive earnings strength. Uncover the future profit assumptions and financial forecasts that could surprise you. Are they bold, or too bullish?

However, Lloyds' heavy reliance on the UK economy and risks from digital disruption could quickly challenge the optimistic outlook that analysts currently expect.

While most analyst narratives and market multiples consider Lloyds Banking Group modestly overvalued at present, our DCF model presents a strikingly different picture. According to the SWS DCF model, the stock is trading 33% below its intrinsic fair value, highlighting significant upside that market multiples might be missing. Could these discount-driven estimates point to hidden value, or are they just too optimistic?

If the current perspective doesn’t quite align with your own, you can dive into the data and build your own Lloyds Banking Group narrative in just minutes. Do it your way

A great starting point for your Lloyds Banking Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Uncover powerful trends, promising sectors, and hidden gems beyond the obvious. This is your chance to get ahead of the crowd.

Ride the wave of revolutionary health tech by selecting these 30 healthcare AI stocks for exposure to companies shaking up the medical field with AI-driven breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies