Advertisement

- France

- /

- Renewable Energy

- /

- ENXTPA:HDF

Is Hydrogène de France Société anonyme (EPA:HDF) In A Good Position To Invest In Growth?

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So, the natural question for Hydrogène de France Société anonyme (EPA:HDF) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for Hydrogène de France Société anonyme

When Might Hydrogène de France Société anonyme Run Out Of Money?

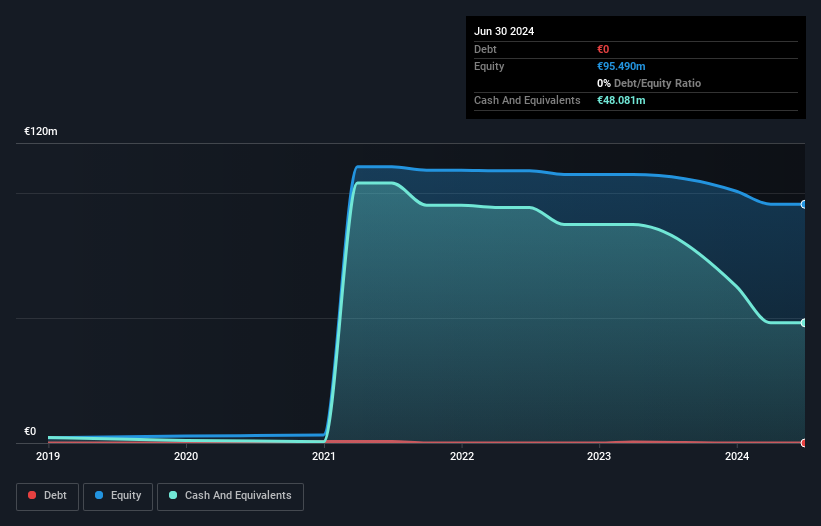

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In June 2024, Hydrogène de France Société anonyme had €48m in cash, and was debt-free. Looking at the last year, the company burnt through €29m. So it had a cash runway of approximately 20 months from June 2024. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Hydrogène de France Société anonyme Growing?

Hydrogène de France Société anonyme actually ramped up its cash burn by a whopping 65% in the last year, which shows it is boosting investment in the business. As if that's not bad enough, the operating revenue also dropped by 2.7%, making us very wary indeed. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Hydrogène de France Société anonyme Raise More Cash Easily?

Hydrogène de France Société anonyme seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of €60m, Hydrogène de France Société anonyme's €29m in cash burn equates to about 48% of its market value. That's high expenditure relative to the value of the entire company, so if it does have to issue shares to fund more growth, that could end up really hurting shareholders returns (through significant dilution).

Is Hydrogène de France Société anonyme's Cash Burn A Worry?

On this analysis of Hydrogène de France Société anonyme's cash burn, we think its cash runway was reassuring, while its cash burn relative to its market cap has us a bit worried. Summing up, we think the Hydrogène de France Société anonyme's cash burn is a risk, based on the factors we mentioned in this article. Taking a deeper dive, we've spotted 5 warning signs for Hydrogène de France Société anonyme you should be aware of, and 1 of them is significant.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies with significant insider holdings, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if Hydrogène de France Société anonyme might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:HDF

Hydrogène de France Société anonyme

Focuses on developing hydrogen infrastructure and multi-megawatt fuel cell technology.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor