Compagnie de l'Odet (EPA:ODET) Has A Pretty Healthy Balance Sheet

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Compagnie de l'Odet (EPA:ODET) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Compagnie de l'Odet

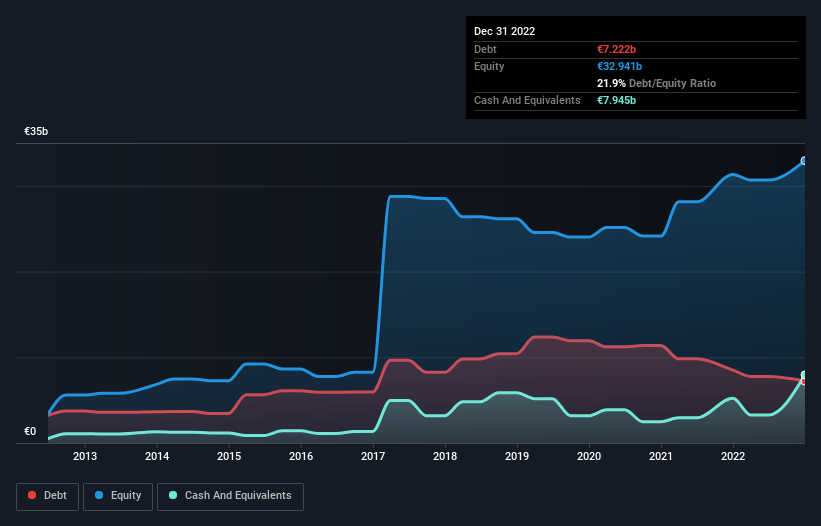

What Is Compagnie de l'Odet's Debt?

As you can see below, Compagnie de l'Odet had €7.22b of debt at December 2022, down from €8.50b a year prior. However, its balance sheet shows it holds €7.95b in cash, so it actually has €723.1m net cash.

How Healthy Is Compagnie de l'Odet's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Compagnie de l'Odet had liabilities of €12.1b due within 12 months and liabilities of €8.93b due beyond that. Offsetting these obligations, it had cash of €7.95b as well as receivables valued at €6.81b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €6.31b.

This is a mountain of leverage relative to its market capitalization of €6.44b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. Despite its noteworthy liabilities, Compagnie de l'Odet boasts net cash, so it's fair to say it does not have a heavy debt load!

Better yet, Compagnie de l'Odet grew its EBIT by 158% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Compagnie de l'Odet's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Compagnie de l'Odet has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Compagnie de l'Odet actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While Compagnie de l'Odet does have more liabilities than liquid assets, it also has net cash of €723.1m. And it impressed us with free cash flow of €1.2b, being 212% of its EBIT. So we don't have any problem with Compagnie de l'Odet's use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Compagnie de l'Odet you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:ODET

Compagnie de l'Odet

Operates transportation and logistics, communication, and industry business in France, Africa, the Americas, the Asia-Pacific, and other European countries.

Flawless balance sheet and fair value.