Sopra Steria Group Full Year 2024 Earnings: EPS Misses Expectations

Sopra Steria Group (EPA:SOP) Full Year 2024 Results

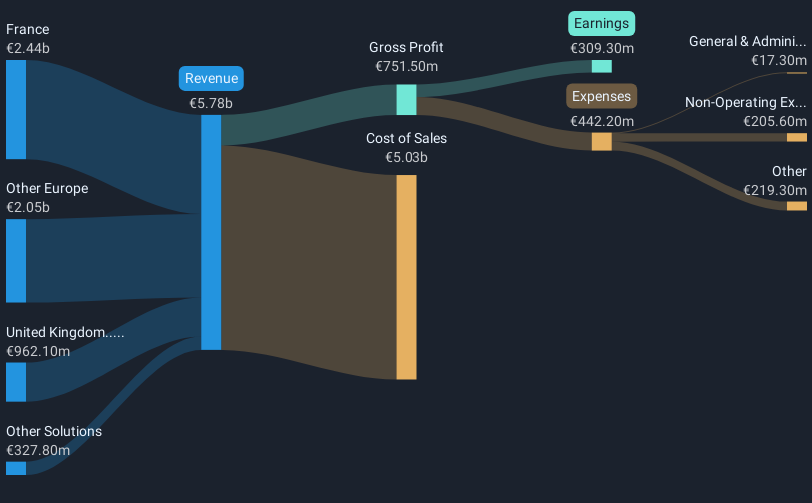

Key Financial Results

- Revenue: €5.78b (flat on FY 2023).

- Net income: €309.3m (up 68% from FY 2023).

- Profit margin: 5.4% (up from 3.2% in FY 2023).

- EPS: €15.36 (up from €9.09 in FY 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

Sopra Steria Group EPS Misses Expectations

Revenue was in line with analyst estimates. Earnings per share (EPS) missed analyst estimates by 11%.

The primary driver behind last 12 months revenue was the France segment contributing a total revenue of €2.44b (42% of total revenue). Notably, cost of sales worth €5.03b amounted to 87% of total revenue thereby underscoring the impact on earnings. The most substantial expense, totaling €205.6m were related to Non-Operating costs. This indicates that a significant portion of the company's costs is related to non-core activities. Explore how SOP's revenue and expenses shape its earnings.

Looking ahead, revenue is forecast to grow 1.9% p.a. on average during the next 3 years, compared to a 4.7% growth forecast for the IT industry in France.

Performance of the French IT industry.

The company's shares are down 14% from a week ago.

Risk Analysis

We don't want to rain on the parade too much, but we did also find 1 warning sign for Sopra Steria Group that you need to be mindful of.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:SOP

Sopra Steria Group

Provides consulting, digital, and software development services in France and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026