Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Innate Pharma S.A. (EPA:IPH) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Innate Pharma

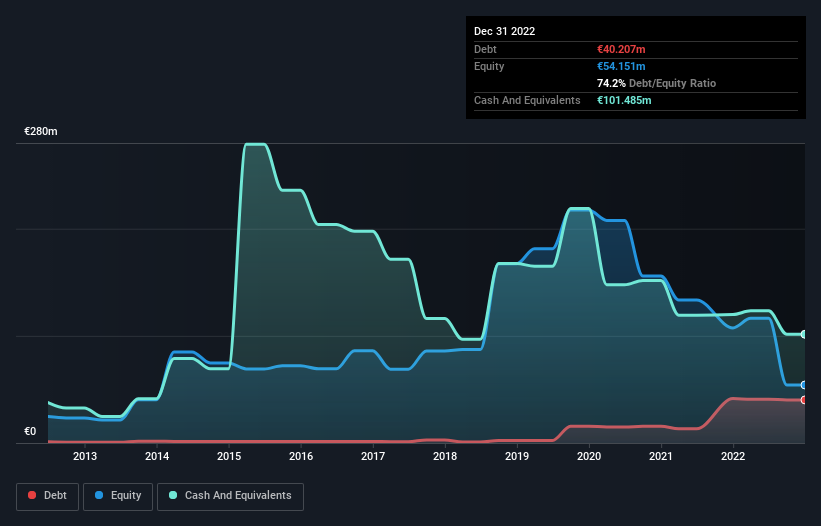

What Is Innate Pharma's Net Debt?

The chart below, which you can click on for greater detail, shows that Innate Pharma had €40.2m in debt in December 2022; about the same as the year before. But on the other hand it also has €101.5m in cash, leading to a €61.3m net cash position.

How Healthy Is Innate Pharma's Balance Sheet?

According to the last reported balance sheet, Innate Pharma had liabilities of €41.3m due within 12 months, and liabilities of €112.4m due beyond 12 months. Offsetting these obligations, it had cash of €101.5m as well as receivables valued at €31.0m due within 12 months. So it has liabilities totalling €21.2m more than its cash and near-term receivables, combined.

Since publicly traded Innate Pharma shares are worth a total of €245.4m, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Innate Pharma also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Innate Pharma can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Innate Pharma wasn't profitable at an EBIT level, but managed to grow its revenue by 133%, to €58m. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Innate Pharma?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Innate Pharma had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of €20m and booked a €58m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of €61.3m. That means it could keep spending at its current rate for more than two years. The good news for shareholders is that Innate Pharma has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Innate Pharma that you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:IPH

Innate Pharma

Operates as a biotechnology company that develops immunotherapies for cancer patients in France and internationally.

Adequate balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor