Advertisement

- France

- /

- Basic Materials

- /

- ENXTPA:NK

Imerys S.A. (EPA:NK) Just Reported, And Analysts Assigned A €28.40 Price Target

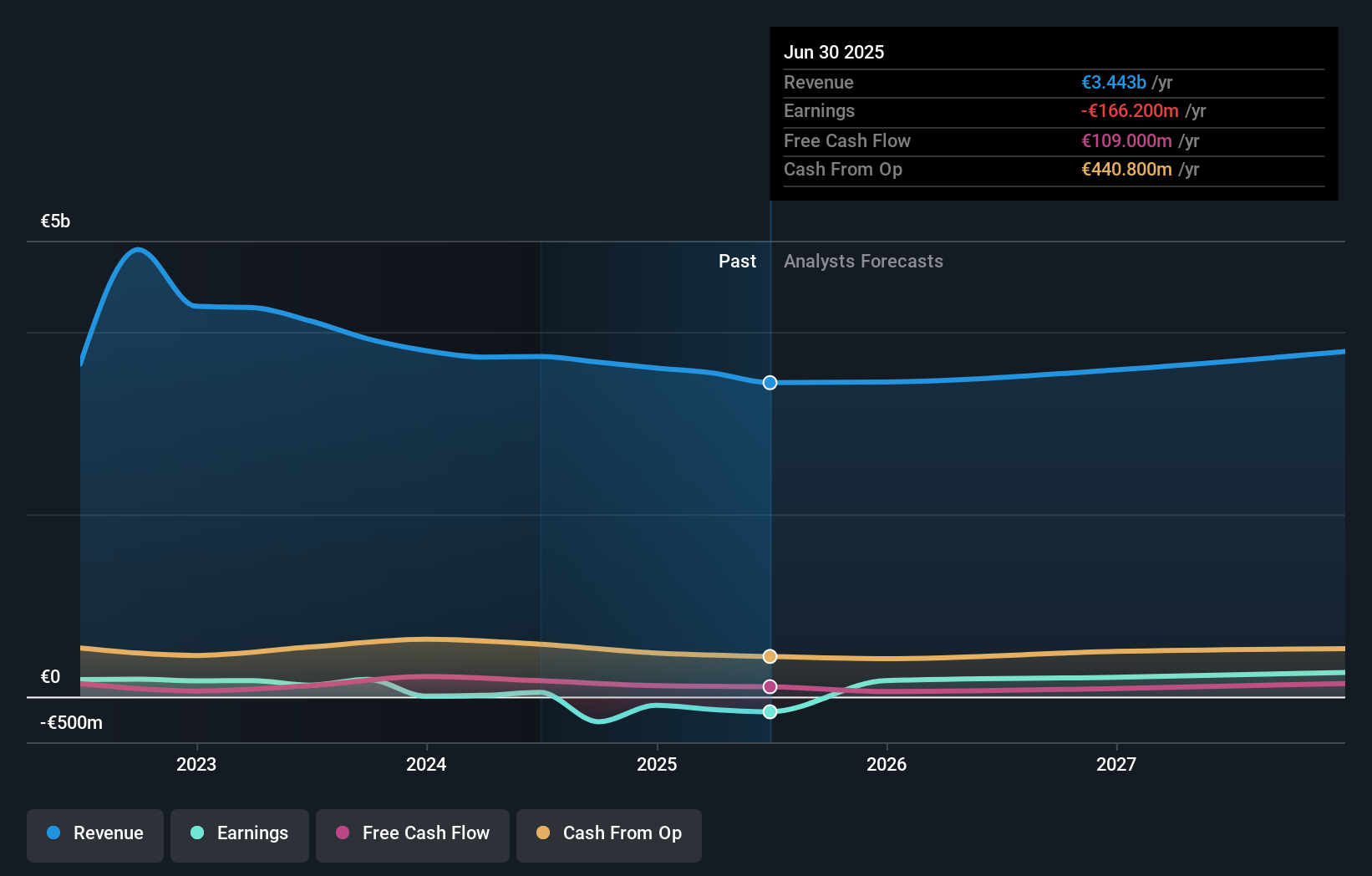

There's been a notable change in appetite for Imerys S.A. (EPA:NK) shares in the week since its interim report, with the stock down 17% to €21.76. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Taking into account the latest results, Imerys' five analysts currently expect revenues in 2025 to be €3.45b, approximately in line with the last 12 months. Imerys is also expected to turn profitable, with statutory earnings of €1.94 per share. In the lead-up to this report, the analysts had been modelling revenues of €3.54b and earnings per share (EPS) of €2.29 in 2025. From this we can that sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a real cut to earnings per share estimates.

Check out our latest analysis for Imerys

The consensus price target fell 15% to €28.40, with the weaker earnings outlook clearly leading valuation estimates. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Imerys analyst has a price target of €38.00 per share, while the most pessimistic values it at €22.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Of course, another way to look at these forecasts is to place them into context against the industry itself. From these estimates it looks as though the analysts expect the years of declining revenue to come to an end, given the flat forecast out to 2025. That would be a definite improvement, given that the past five years have seen revenue shrink 2.1% annually. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 1.2% annually. Although Imerys' revenues are expected to improve, it seems that it is still expected to grow slower than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Imerys. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Imerys going out to 2027, and you can see them free on our platform here..

Plus, you should also learn about the 2 warning signs we've spotted with Imerys (including 1 which is potentially serious) .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:NK

Imerys

Engages in the supply of specialty minerals for various industries across Europe, the Middle East, Africa, Asia Pacific, and America.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor