- France

- /

- Metals and Mining

- /

- ENXTPA:ERA

Here's What Analysts Are Forecasting For ERAMET S.A. (EPA:ERA) After Its Interim Results

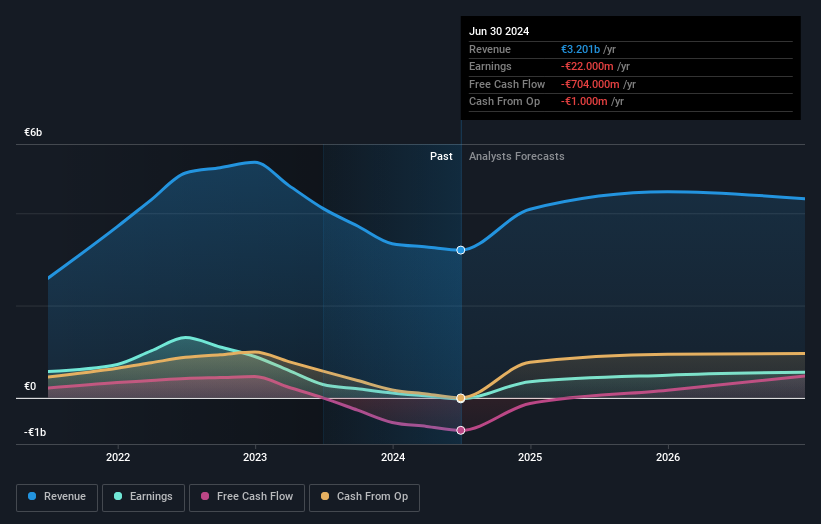

It's been a sad week for ERAMET S.A. (EPA:ERA), who've watched their investment drop 14% to €82.20 in the week since the company reported its half-year result. Revenues came in 3.8% below expectations, at €1.5b. Statutory earnings per share were relatively better off, with a per-share profit of €3.79 being roughly in line with analyst estimates. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on ERAMET after the latest results.

View our latest analysis for ERAMET

After the latest results, the five analysts covering ERAMET are now predicting revenues of €4.09b in 2024. If met, this would reflect a huge 28% improvement in revenue compared to the last 12 months. ERAMET is also expected to turn profitable, with statutory earnings of €12.18 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of €3.91b and earnings per share (EPS) of €11.67 in 2024. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

Despite these upgrades,the analysts have not made any major changes to their price target of €154, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic ERAMET analyst has a price target of €178 per share, while the most pessimistic values it at €107. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that ERAMET's rate of growth is expected to accelerate meaningfully, with the forecast 63% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 2.2% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 2.1% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that ERAMET is expected to grow much faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around ERAMET's earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target held steady at €154, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for ERAMET going out to 2026, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 1 warning sign for ERAMET you should know about.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if ERAMET might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:ERA

ERAMET

Produces and sells manganese and nickel metals in Asia, Europe, North America, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion

Thanks for sharing these. They really help when I pick what dividend stocks to invest in