Advertisement

- France

- /

- Healthcare Services

- /

- ENXTPA:GDS

These 4 Measures Indicate That Ramsay Générale de Santé (EPA:GDS) Is Using Debt Extensively

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Ramsay Générale de Santé SA (EPA:GDS) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Ramsay Générale de Santé

What Is Ramsay Générale de Santé's Net Debt?

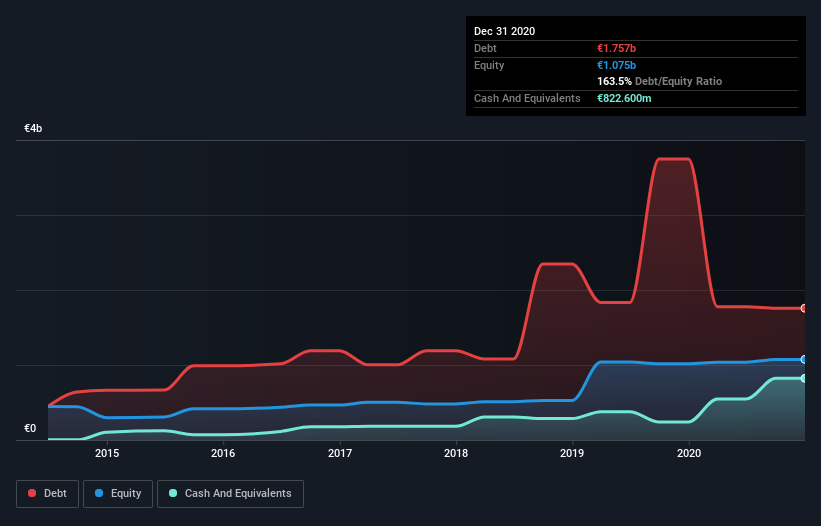

As you can see below, Ramsay Générale de Santé had €1.76b of debt at December 2020, down from €3.75b a year prior. However, because it has a cash reserve of €822.6m, its net debt is less, at about €934.4m.

A Look At Ramsay Générale de Santé's Liabilities

We can see from the most recent balance sheet that Ramsay Générale de Santé had liabilities of €1.60b falling due within a year, and liabilities of €4.10b due beyond that. Offsetting these obligations, it had cash of €822.6m as well as receivables valued at €281.3m due within 12 months. So its liabilities total €4.60b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the €2.13b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Ramsay Générale de Santé would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Ramsay Générale de Santé's debt to EBITDA ratio (5.0) suggests that it uses some debt, its interest cover is very weak, at 1.9, suggesting high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. On a lighter note, we note that Ramsay Générale de Santé grew its EBIT by 23% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. When analysing debt levels, the balance sheet is the obvious place to start. But it is Ramsay Générale de Santé's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Ramsay Générale de Santé actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

While Ramsay Générale de Santé's level of total liabilities has us nervous. To wit both its conversion of EBIT to free cash flow and EBIT growth rate were encouraging signs. It's also worth noting that Ramsay Générale de Santé is in the Healthcare industry, which is often considered to be quite defensive. Taking the abovementioned factors together we do think Ramsay Générale de Santé's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Ramsay Générale de Santé .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade Ramsay Générale de Santé, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:GDS

Ramsay Générale de Santé

Operates healthcare facilities in France, Sweden, Norway, Denmark, and Italy.

Good value with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor