- France

- /

- Healthcare Services

- /

- ENXTPA:BLC

It Looks Like Bastide Le Confort Médical SA's (EPA:BLC) CEO May Expect Their Salary To Be Put Under The Microscope

Key Insights

- Bastide Le Confort Médical to hold its Annual General Meeting on 19th of December

- Salary of €200.0k is part of CEO Vincent Bastide's total remuneration

- The total compensation is similar to the average for the industry

- Bastide Le Confort Médical's EPS declined by 41% over the past three years while total shareholder loss over the past three years was 32%

The results at Bastide Le Confort Médical SA (EPA:BLC) have been quite disappointing recently and CEO Vincent Bastide bears some responsibility for this. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 19th of December. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. We present the case why we think CEO compensation is out of sync with company performance.

View our latest analysis for Bastide Le Confort Médical

Comparing Bastide Le Confort Médical SA's CEO Compensation With The Industry

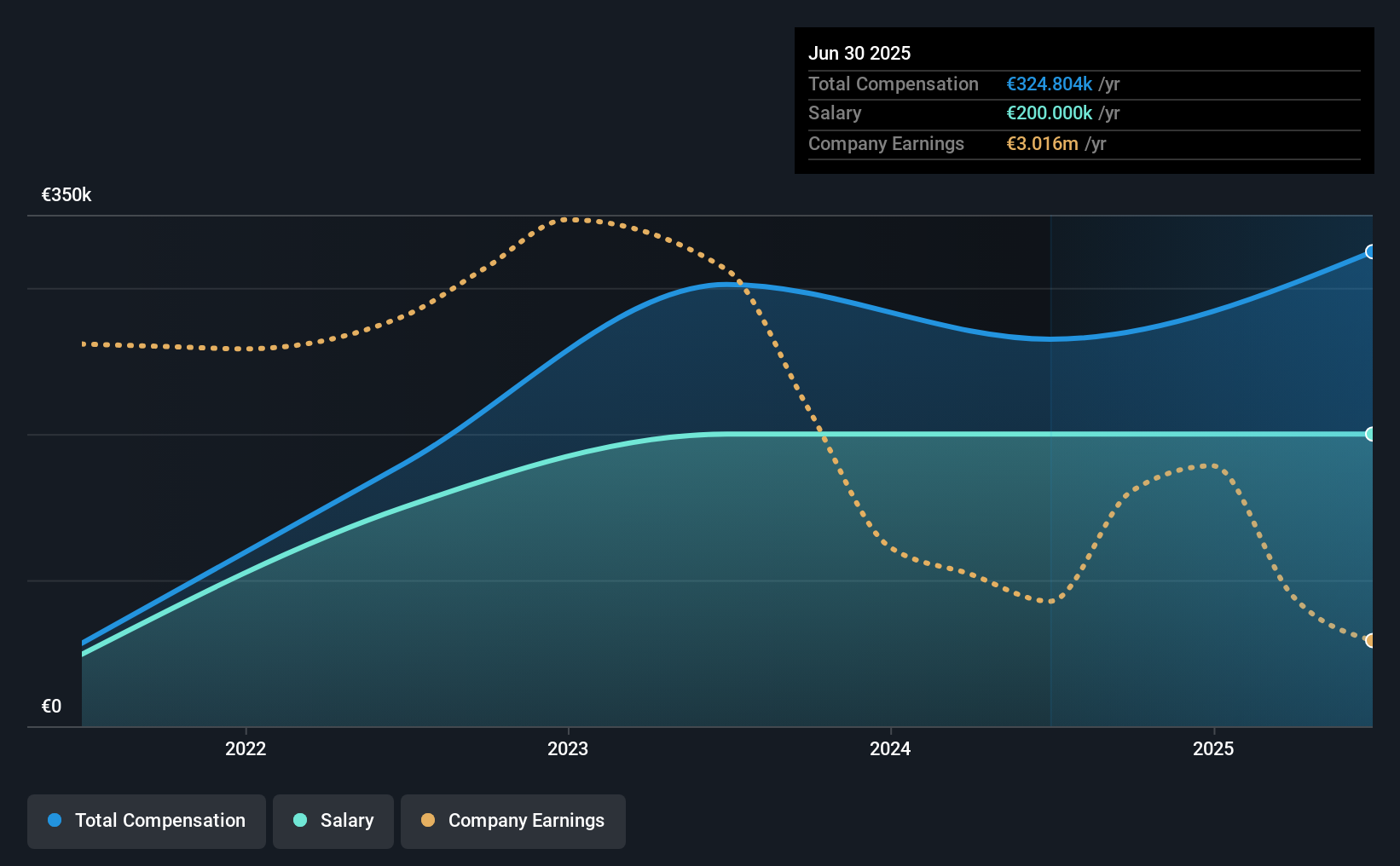

At the time of writing, our data shows that Bastide Le Confort Médical SA has a market capitalization of €183m, and reported total annual CEO compensation of €325k for the year to June 2025. We note that's an increase of 23% above last year. Notably, the salary which is €200.0k, represents most of the total compensation being paid.

In comparison with other companies in the France Healthcare industry with market capitalizations ranging from €85m to €341m, the reported median CEO total compensation was €340k. From this we gather that Vincent Bastide is paid around the median for CEOs in the industry. What's more, Vincent Bastide holds €2.9m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | €200k | €200k | 62% |

| Other | €125k | €65k | 38% |

| Total Compensation | €325k | €265k | 100% |

Speaking on an industry level, nearly 53% of total compensation represents salary, while the remainder of 47% is other remuneration. Bastide Le Confort Médical is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Bastide Le Confort Médical SA's Growth

Over the last three years, Bastide Le Confort Médical SA has shrunk its earnings per share by 41% per year. Its revenue is up 6.3% over the last year.

Overall this is not a very positive result for shareholders. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Bastide Le Confort Médical SA Been A Good Investment?

The return of -32% over three years would not have pleased Bastide Le Confort Médical SA shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We did our research and identified 3 warning signs (and 1 which doesn't sit too well with us) in Bastide Le Confort Médical we think you should know about.

Important note: Bastide Le Confort Médical is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Bastide Le Confort Médical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:BLC

Bastide Le Confort Médical

Engages in the sale and rental of medical equipment in France, the United Kingdom, Belgium, Spain, Canada, the Netherlands, and Italy.

Reasonable growth potential and fair value.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)