Advertisement

As European markets navigate the complexities of political turmoil in France and international trade tensions, the pan-European STOXX Europe 600 Index has recently experienced a slight decline after reaching record highs. Despite these challenges, opportunities may arise for investors seeking potential growth in under-the-radar stocks that demonstrate resilience and adaptability to shifting economic landscapes.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Dekpol | 64.28% | 9.75% | 13.77% | ★★★★★☆ |

| Sparta | NA | nan | nan | ★★★★★☆ |

| Grenobloise d'Electronique et d'Automatismes Société Anonyme | 0.01% | 7.01% | -1.81% | ★★★★★☆ |

| Inmocemento | 28.68% | 4.15% | 33.84% | ★★★★★☆ |

| Freetrailer Group | 0.01% | 22.96% | 31.56% | ★★★★★☆ |

| Inversiones Doalca SOCIMI | 13.10% | 6.72% | 3.11% | ★★★★★☆ |

| va-Q-tec | 43.54% | 8.03% | -34.33% | ★★★★★☆ |

| Zespól Elektrocieplowni Wroclawskich KOGENERACJA | 13.23% | 20.22% | 17.99% | ★★★★★☆ |

| ABG Sundal Collier Holding | 46.02% | -6.02% | -15.62% | ★★★★☆☆ |

| Practic | NA | 4.86% | 6.64% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

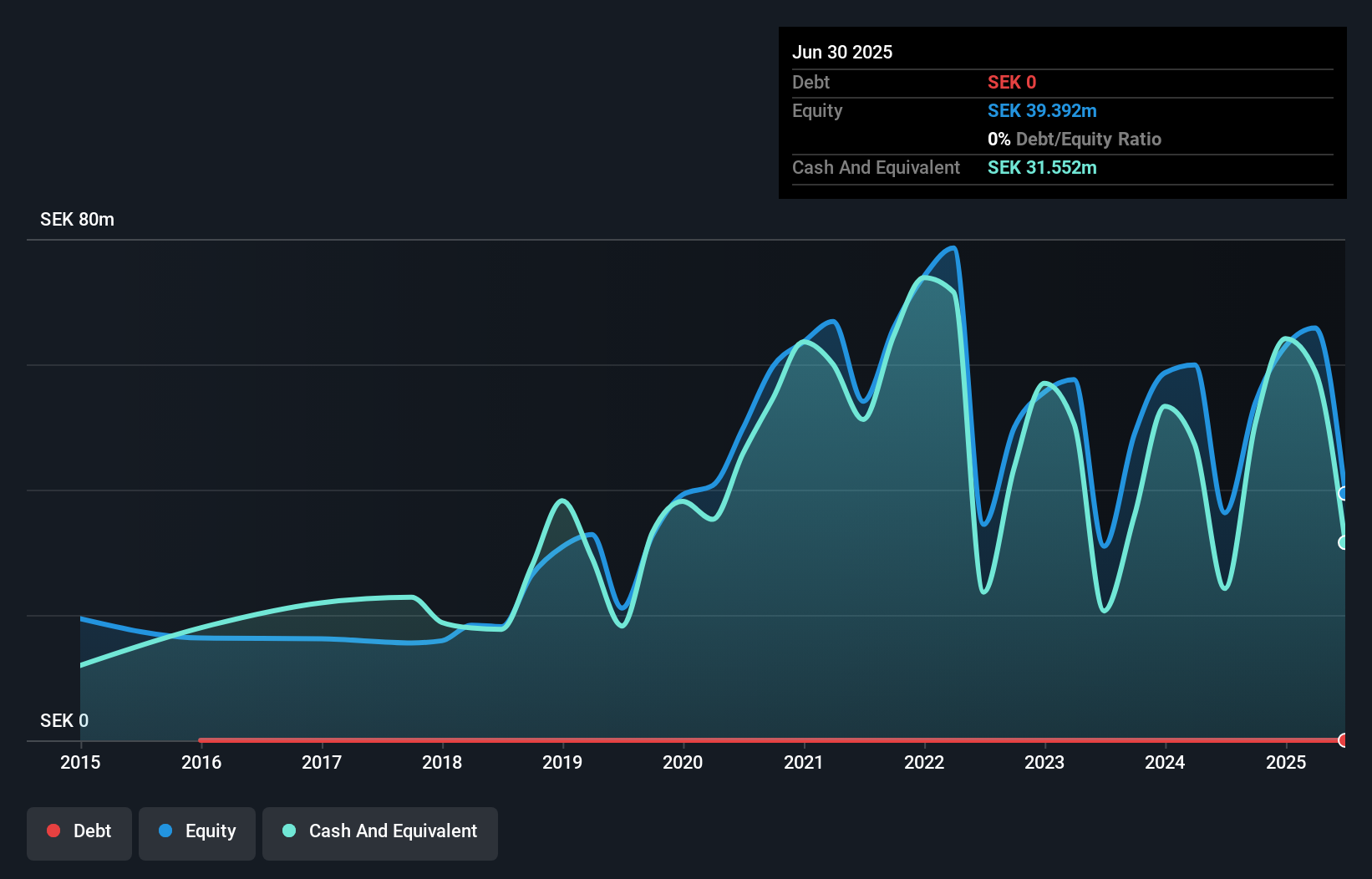

Veteranpoolen (DB:QI5)

Simply Wall St Value Rating: ★★★★★★

Overview: Veteranpoolen AB (publ) operates as a staffing company with a market cap of €984.91 million.

Operations: The company generates revenue primarily from its Staffing & Outsourcing Services, totaling SEK 594.46 million.

Veteranpoolen, a promising player in the European market, is capturing attention with its robust financial health and growth trajectory. The company stands debt-free for five years, showcasing high-quality earnings that outpace industry norms. Recent reports highlight a 9.3% earnings growth over the past year, surpassing the Professional Services industry's 2.7%. Trading at a significant discount of 52.4% below estimated fair value adds to its allure as an undervalued investment opportunity. In Q2 2025, Veteranpoolen reported sales of SEK 188.99 million and net income of SEK 18.63 million, reflecting solid operational performance and profitability improvements from last year’s figures.

- Click here to discover the nuances of Veteranpoolen with our detailed analytical health report.

Explore historical data to track Veteranpoolen's performance over time in our Past section.

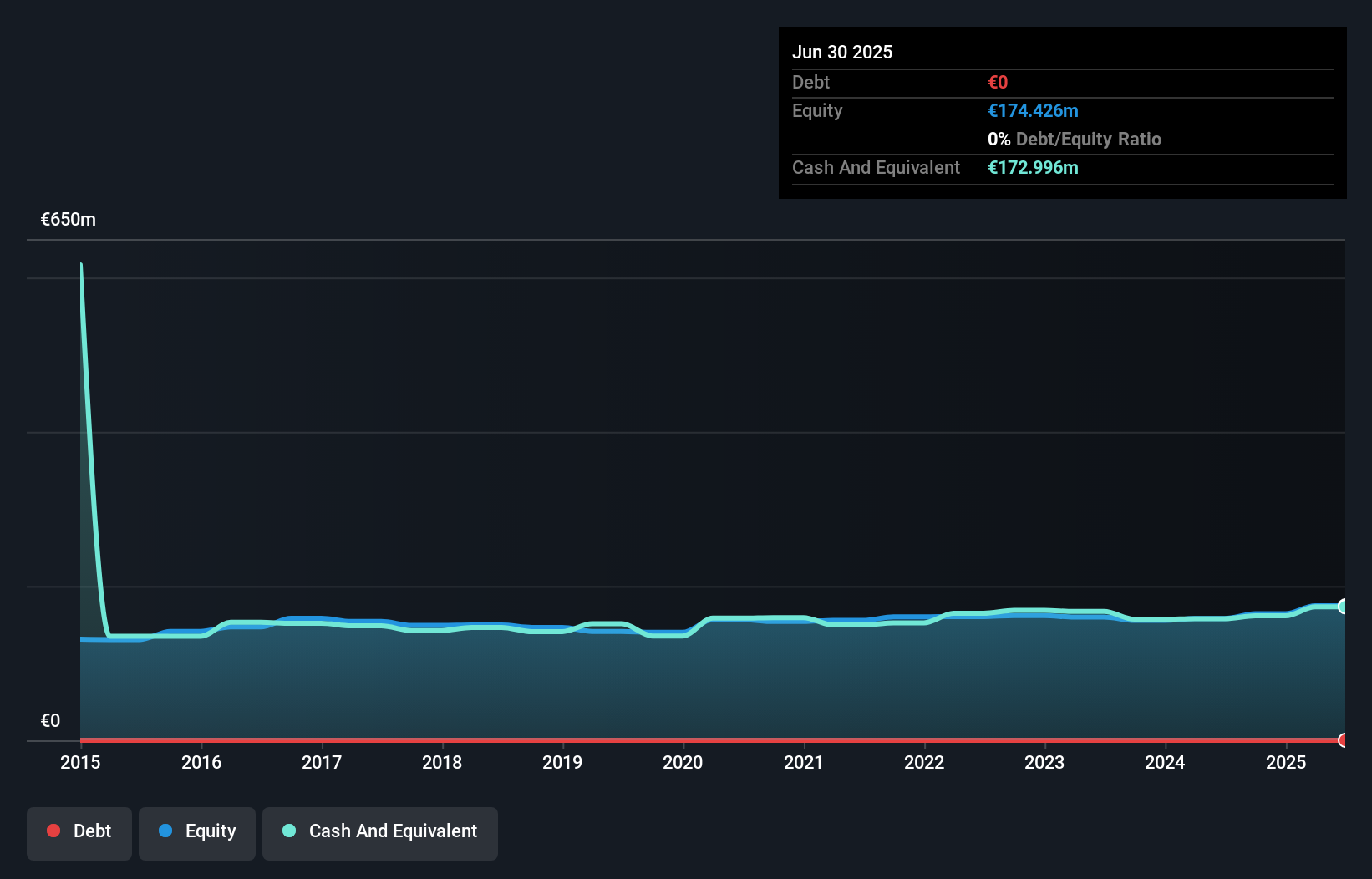

ABC arbitrage (ENXTPA:ABCA)

Simply Wall St Value Rating: ★★★★★★

Overview: ABC arbitrage SA, along with its subsidiaries, specializes in developing arbitrage strategies for liquid assets across Europe, North America, Asia, and other international markets, with a market cap of €331.65 million.

Operations: ABC arbitrage generates revenue primarily from its arbitrage trading activities, amounting to €65.13 million. The company has a market capitalization of €331.65 million.

ABC arbitrage, a nimble player in the financial sector, demonstrates strong fundamentals with no debt on its books over the past five years. The company is trading at 30.6% below its estimated fair value, offering potential upside for investors. Recent earnings results show net income of €17.67 million for the first half of 2025, up from €8.86 million a year prior, indicating robust performance despite forecasted earnings declines averaging 18.6% annually over the next three years. With high-quality non-cash earnings and positive free cash flow, ABC arbitrage seems well-positioned to navigate future challenges in its industry landscape.

- Get an in-depth perspective on ABC arbitrage's performance by reading our health report here.

Evaluate ABC arbitrage's historical performance by accessing our past performance report.

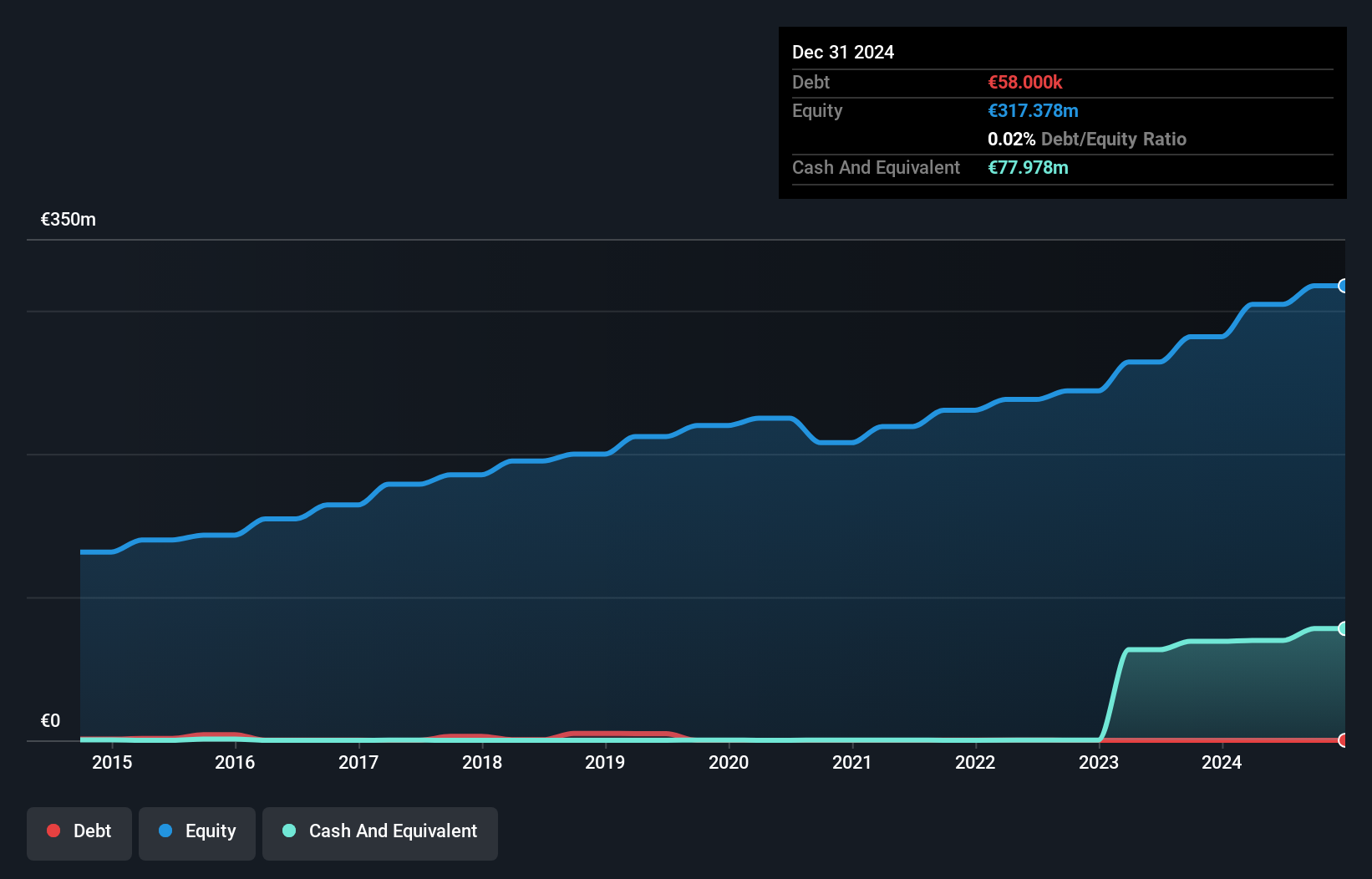

Malteries Franco-Belges Société Anonyme (ENXTPA:MALT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Malteries Franco-Belges Société Anonyme is involved in the production and sale of malt for brewers both in France and internationally, with a market capitalization of approximately €436.47 million.

Operations: Malteries Franco-Belges generates revenue primarily from its malt factory, amounting to €140.20 million. The company's market capitalization stands at approximately €436.47 million.

With earnings growth of 12.4% over the past year, Malteries Franco-Belges outpaced the Food industry's -15% performance, highlighting its resilience. The company holds more cash than total debt, indicating a solid financial footing and ensuring interest payments are well-covered. However, its debt-to-equity ratio has slightly increased from 0.01% to 0.02% over five years, suggesting a cautious approach to leverage. Trading at approximately 34.7% below fair value estimates presents potential upside for investors seeking undervalued opportunities in this niche sector. Despite these strengths, recent financial data is outdated by over six months, which may affect timely analysis and decision-making.

Where To Now?

- Click this link to deep-dive into the 330 companies within our European Undiscovered Gems With Strong Fundamentals screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:MALT

Malteries Franco-Belges Société Anonyme

Engages in the production and sale of malt primarily for brewers in France and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor