- France

- /

- Diversified Financial

- /

- ENXTPA:WLN

Worldline (ENXTPA:WLN) Eyes Recovery with AI Alliances Despite Index Exclusions and Revenue Challenges

Reviewed by Simply Wall St

Worldline (ENXTPA:WLN) is navigating a period of strategic transformation, marked by innovative payment solutions and a new leadership under interim CEO Marc-Henri Desportes. Despite recent index exclusions and profitability challenges, the company's strategic alliances and technological advancements, such as AI-powered lending solutions, position it for potential recovery and growth. As Worldline aims to enhance its market offerings, readers should expect a detailed analysis of its financial outlook and strategic initiatives in the following discussion.

Take a closer look at Worldline's potential here.

Unique Capabilities Enhancing Worldline's Market Position

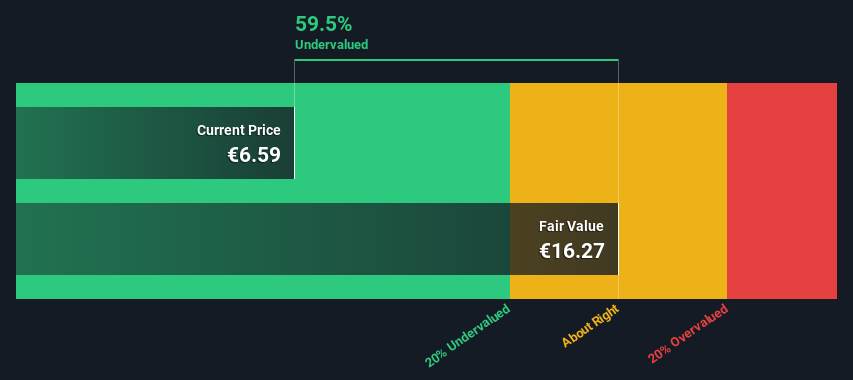

Worldline's strategic initiatives, including the rollout of innovative payment solutions, underscore its commitment to leading industry trends. The leadership's experience, particularly Marc-Henri Desportes' interim CEO role, ensures strategic continuity and operational efficiency. The company's trading at €6.36, significantly below the estimated fair value of €16.84, presents an attractive investment opportunity. This is further supported by a favorable SWS Price-To-Sales Ratio of 0.4x, compared to industry averages.

To dive deeper into how Worldline's valuation metrics are shaping its market position, check out our detailed analysis of Worldline's Valuation.Internal Limitations Hindering Worldline's Growth

Despite a seasoned management team, Worldline faces challenges with profitability, reflected in a negative Return on Equity of -11.28%. The company's revenue growth forecast of 3.3% lags behind market benchmarks, indicating potential hurdles in maintaining competitive momentum. Additionally, the absence of dividend payouts raises concerns about financial sustainability. These factors highlight the need for strategic adjustments to align with industry standards.

Learn about Worldline's dividend strategy and how it impacts shareholder returns and financial stability.Areas for Expansion and Innovation for Worldline

Anticipated profitability within three years and projected earnings growth of 70.92% per year position Worldline for significant recovery. Strategic alliances, such as the AI-powered lending solutions collaboration, enhance its market offerings and client engagement. These initiatives are poised to strengthen Worldline's market position, leveraging technological advancements to capture emerging opportunities.

See what the latest analyst reports say about Worldline's future prospects and potential market movements.Key Risks and Challenges That Could Impact Worldline's Success

Worldline's recent exclusion from major indices like the S&P EUROPE 350 and FTSE All-World Index signifies potential market perception challenges. The volatility in share price and lack of consensus among analysts on target pricing further underscore market uncertainties. Additionally, ongoing supply chain disruptions and regulatory changes pose external threats that could impact operational stability and growth.

To gain deeper insights into Worldline's historical performance, explore our detailed analysis of past performance.Conclusion

Worldline's strategic initiatives, including innovative payment solutions and leadership under Marc-Henri Desportes, position the company to capitalize on industry trends and operational efficiency. Current challenges, such as a negative Return on Equity and slow revenue growth, are countered by the company's anticipated earnings growth of 70.92% per year and strategic alliances that suggest a promising recovery trajectory. Trading at €6.36, significantly below its estimated fair value of €16.84, Worldline presents a compelling investment opportunity, especially as it navigates market perception challenges and external threats. The company's focus on technological advancements and strategic adjustments is crucial for enhancing profitability and sustaining growth in the long term.

Next Steps

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

If you're looking to trade Worldline, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Worldline might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ENXTPA:WLN

Worldline

Provides payments and transactional services for financial institutions, merchants, corporations, and government agencies in Northern Europe, Central and Eastern Europe, Southern Europe, and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives