Advertisement

- France

- /

- Professional Services

- /

- ENXTPA:CEN

Discovering Three European Small Caps with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As the European market navigates a landscape of mixed economic indicators and geopolitical uncertainties, the pan-European STOXX Europe 600 Index has managed to edge higher, buoyed by hopes of increased government spending despite concerns over impending U.S. tariffs. In this environment, identifying small-cap stocks with strong potential requires a focus on companies that exhibit robust fundamentals and resilience to external pressures, making them well-positioned to capitalize on emerging opportunities in this complex market setting.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| AB Traction | NA | 3.81% | 3.66% | ★★★★★★ |

| Nederman Holding | 69.60% | 11.43% | 16.35% | ★★★★★★ |

| Martifer SGPS | 123.58% | -2.38% | 5.61% | ★★★★★★ |

| Mirbud | 16.01% | 27.19% | 26.48% | ★★★★★★ |

| Intellego Technologies | 11.59% | 68.05% | 72.76% | ★★★★★★ |

| Moury Construct | 2.93% | 10.50% | 27.28% | ★★★★★☆ |

| Onde | 21.84% | 8.04% | 2.79% | ★★★★★☆ |

| Infinity Capital Investments | NA | 9.92% | 22.16% | ★★★★★☆ |

| ABG Sundal Collier Holding | 0.61% | -1.57% | -8.96% | ★★★★☆☆ |

| Castellana Properties Socimi | 53.49% | 6.64% | 21.96% | ★★★★☆☆ |

We'll examine a selection from our screener results.

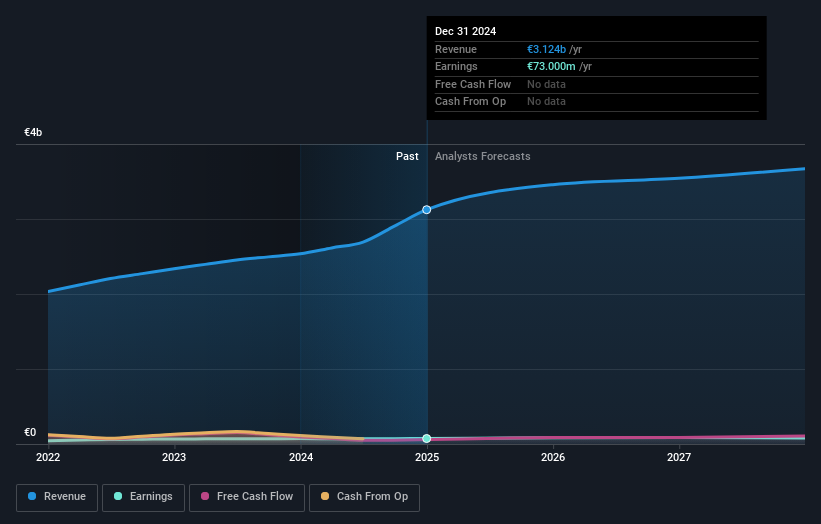

Groupe CRIT (ENXTPA:CEN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Groupe CRIT SA offers temporary work and recruitment services both in France and internationally, with a market capitalization of €699.69 million.

Operations: Groupe CRIT generates revenue primarily from its temporary work and recruitment services. The company operates in various international markets, with a market capitalization of €699.69 million.

Groupe CRIT, a notable player in the European staffing industry, reported sales of €3.12 billion for 2024, up from €2.54 billion the previous year. Their net income slightly increased to €73 million from €72.8 million, suggesting stable profitability despite market challenges. The company's earnings growth of 0.3% outpaced the professional services industry's -18.3%, highlighting resilience in a tough sector environment. With debt well-covered by EBIT at 324 times and trading at nearly 70% below estimated fair value, Groupe CRIT appears undervalued relative to peers while maintaining high-quality earnings and positive free cash flow.

- Click here to discover the nuances of Groupe CRIT with our detailed analytical health report.

Assess Groupe CRIT's past performance with our detailed historical performance reports.

Arendals Fossekompani (OB:AFK)

Simply Wall St Value Rating: ★★★★★★

Overview: Arendals Fossekompani ASA is an industrial investment company that owns and operates hydropower plants across Norway, Europe, Asia, and North America with a market cap of NOK7.15 billion.

Operations: Arendals Fossekompani generates revenue primarily from segments like ENRX (NOK1.91 billion) and NSSL Global (NOK1.40 billion), with additional contributions from Tekna, Property, Alytic, and AFK Vannkraft.

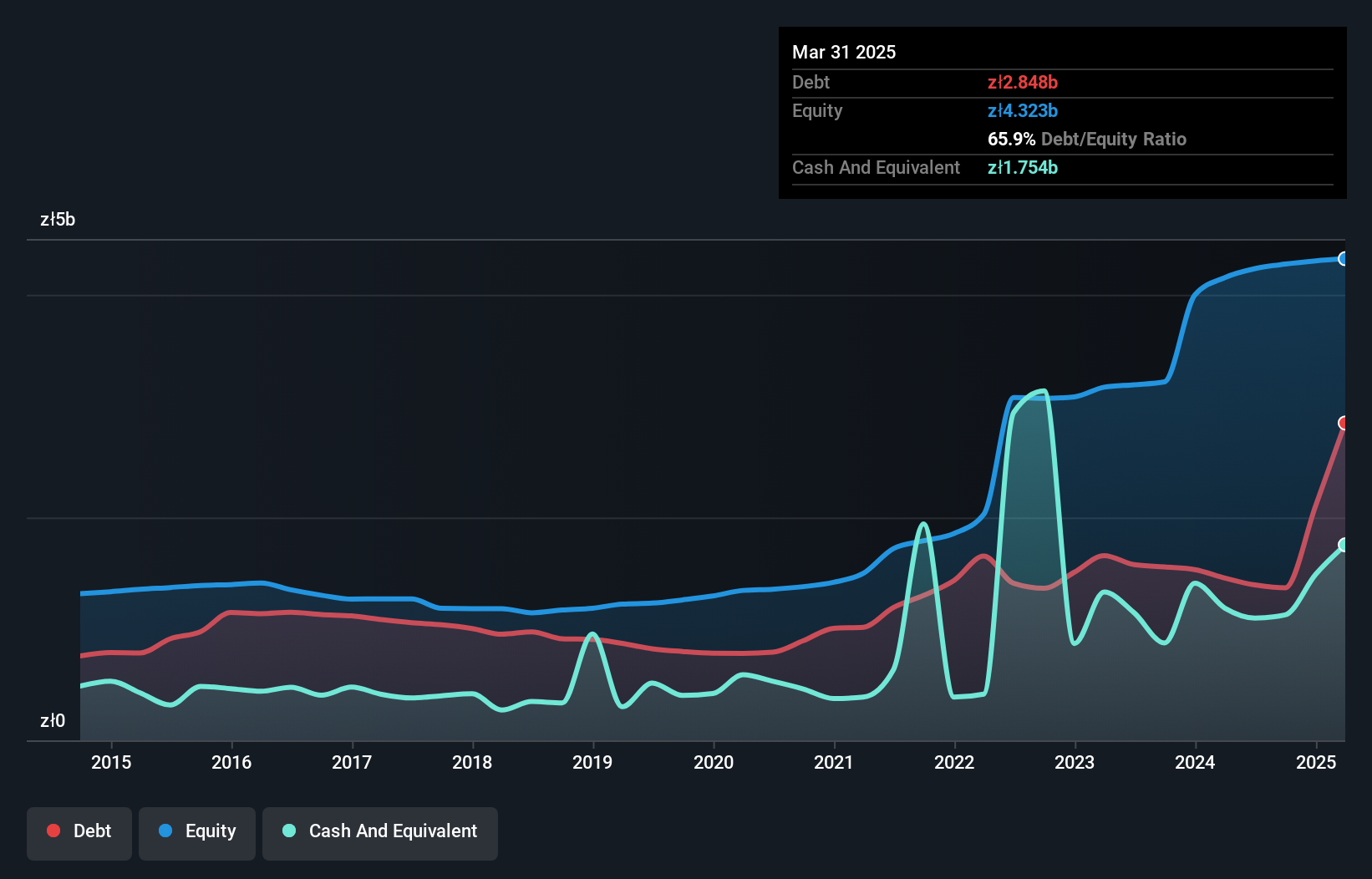

Arendals Fossekompani, a nimble player in the European market, has shown impressive financial resilience. Over the past year, its earnings skyrocketed by 910%, vastly outpacing the Industrials sector's 5.7% growth. The company’s debt to equity ratio improved from 30% to 28% over five years, with interest payments comfortably covered at 3.2 times by EBIT. Trading at a significant discount of 45% below estimated fair value suggests potential for investors seeking undervalued opportunities. Recently, Arendals announced a NOK 1 per share dividend and reported net income of NOK 2.62 billion for the full year ending December 2024.

- Navigate through the intricacies of Arendals Fossekompani with our comprehensive health report here.

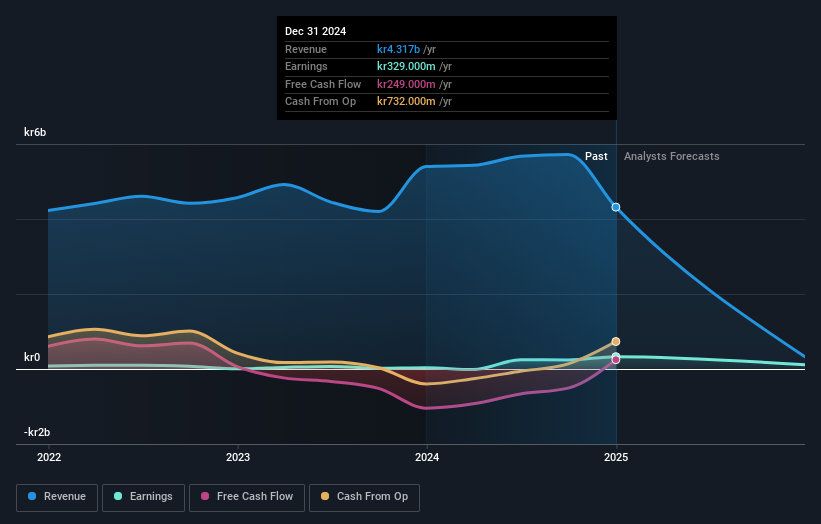

Polenergia (WSE:PEP)

Simply Wall St Value Rating: ★★★★★☆

Overview: Polenergia S.A. operates in the generation, distribution, trading, and sale of electricity both in Poland and internationally, with a market capitalization of PLN5.45 billion.

Operations: Revenue primarily stems from electricity generation, distribution, trading, and sales activities. The company has a market capitalization of PLN5.45 billion.

Polenergia, a notable player in the renewable energy sector, reported a net income of PLN 301.17 million for 2024, up from PLN 263.59 million the previous year. Despite revenue dipping to PLN 4,320.53 million from PLN 5,615.41 million, earnings per share improved slightly to PLN 3.9. The company has shown resilience with its earnings growth of 14%, outpacing the industry average decline of -6%. Polenergia's debt-to-equity ratio has decreased over five years from 60% to around 49%, indicating better financial health and interest coverage is strong at a multiple of over six times EBIT compared to interest obligations.

- Delve into the full analysis health report here for a deeper understanding of Polenergia.

Examine Polenergia's past performance report to understand how it has performed in the past.

Key Takeaways

- Click through to start exploring the rest of the 348 European Undiscovered Gems With Strong Fundamentals now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:CEN

Groupe CRIT

Provides temporary staffing and recruitment services in France and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor