- France

- /

- Aerospace & Defense

- /

- ENXTPA:HO

Declining Stock and Decent Financials: Is The Market Wrong About Thales S.A. (EPA:HO)?

With its stock down 12% over the past three months, it is easy to disregard Thales (EPA:HO). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Thales' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Thales

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Thales is:

12% = €909m ÷ €7.4b (Based on the trailing twelve months to June 2024).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each €1 of shareholders' capital it has, the company made €0.12 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Thales' Earnings Growth And 12% ROE

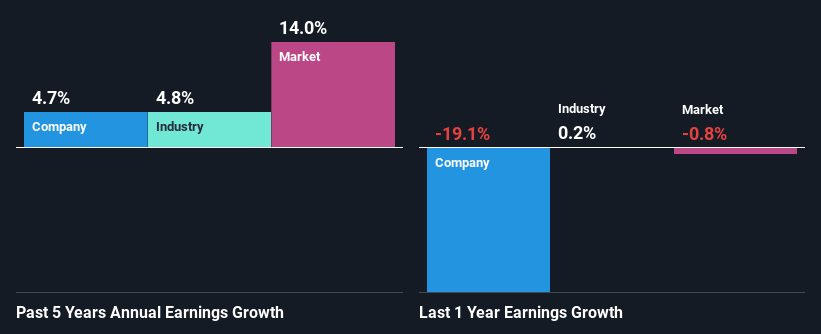

At first glance, Thales seems to have a decent ROE. And on comparing with the industry, we found that the the average industry ROE is similar at 12%. Thales' decent returns aren't reflected in Thales'mediocre five year net income growth average of 4.7%. A few likely reasons that could be keeping earnings growth low are - the company has a high payout ratio or the business has allocated capital poorly, for instance.

We then performed a comparison between Thales' net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 4.8% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Thales is trading on a high P/E or a low P/E, relative to its industry.

Is Thales Making Efficient Use Of Its Profits?

With a high three-year median payout ratio of 56% (or a retention ratio of 44%), most of Thales' profits are being paid to shareholders. This definitely contributes to the low earnings growth seen by the company.

Additionally, Thales has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 40% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 22%, over the same period.

Conclusion

Overall, we feel that Thales certainly does have some positive factors to consider. Its earnings growth is decent, and the high ROE does contribute to that growth. However, investors could have benefitted even more from the high ROE, had the company been reinvesting more of its earnings. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Thales might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:HO

Thales

Provides various solutions in the defence and security, aerospace and space, digital identity and security, and transport markets worldwide.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives