If EPS Growth Is Important To You, Alma Media Oyj (HEL:ALMA) Presents An Opportunity

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

In contrast to all that, many investors prefer to focus on companies like Alma Media Oyj (HEL:ALMA), which has not only revenues, but also profits. While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for Alma Media Oyj

How Quickly Is Alma Media Oyj Increasing Earnings Per Share?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. That makes EPS growth an attractive quality for any company. It certainly is nice to see that Alma Media Oyj has managed to grow EPS by 25% per year over three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

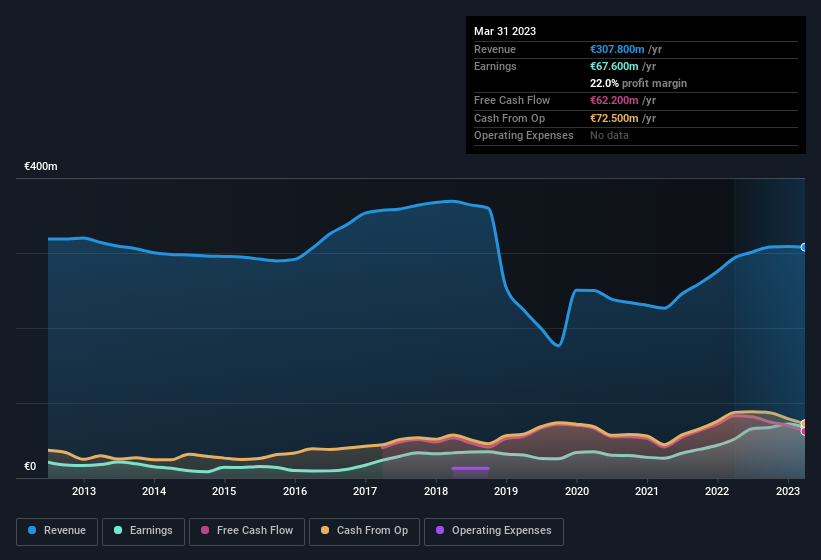

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While we note Alma Media Oyj achieved similar EBIT margins to last year, revenue grew by a solid 4.9% to €308m. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Alma Media Oyj's forecast profits?

Are Alma Media Oyj Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Insider selling of Alma Media Oyj shares was insignificant compared to the one buyer, over the last twelve months. Namely, CEO & President Kai Telanne out-laid €716k for shares, at about €9.21 per share. That can definitely be seen as a sign of conviction.

On top of the insider buying, it's good to see that Alma Media Oyj insiders have a valuable investment in the business. As a matter of fact, their holding is valued at €27m. This considerable investment should help drive long-term value in the business. Despite being just 3.5% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Is Alma Media Oyj Worth Keeping An Eye On?

For growth investors, Alma Media Oyj's raw rate of earnings growth is a beacon in the night. Moreover, the management and board of the company hold a significant stake in the company, with one party adding to this total. So it's fair to say that this stock may well deserve a spot on your watchlist. It is worth noting though that we have found 4 warning signs for Alma Media Oyj (1 shouldn't be ignored!) that you need to take into consideration.

Keen growth investors love to see insider buying. Thankfully, Alma Media Oyj isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:ALMA

Alma Media Oyj

A media company, focuses on digital services and journalistic media content in Finland and the rest of Europe.

Good value average dividend payer.

Market Insights

Community Narratives