- Finland

- /

- Healthcare Services

- /

- HLSE:OKDBV

Oriola Oyj (HEL:OKDBV) Is Finding It Tricky To Allocate Its Capital

When researching a stock for investment, what can tell us that the company is in decline? A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. This reveals that the company isn't compounding shareholder wealth because returns are falling and its net asset base is shrinking. On that note, looking into Oriola Oyj (HEL:OKDBV), we weren't too upbeat about how things were going.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Oriola Oyj is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

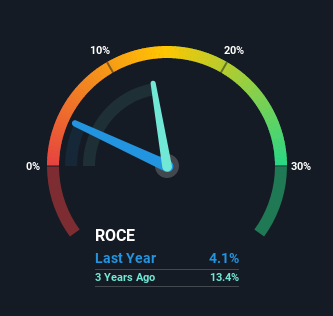

0.041 = €13m ÷ (€1.1b - €824m) (Based on the trailing twelve months to March 2021).

Thus, Oriola Oyj has an ROCE of 4.1%. In absolute terms, that's a low return and it also under-performs the Healthcare industry average of 8.2%.

See our latest analysis for Oriola Oyj

In the above chart we have measured Oriola Oyj's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Oriola Oyj.

What The Trend Of ROCE Can Tell Us

We are a bit worried about the trend of returns on capital at Oriola Oyj. To be more specific, the ROCE was 22% five years ago, but since then it has dropped noticeably. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. If these trends continue, we wouldn't expect Oriola Oyj to turn into a multi-bagger.

On a separate but related note, it's important to know that Oriola Oyj has a current liabilities to total assets ratio of 72%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

In summary, it's unfortunate that Oriola Oyj is generating lower returns from the same amount of capital. Investors haven't taken kindly to these developments, since the stock has declined 47% from where it was five years ago. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

Oriola Oyj does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those is significant...

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About HLSE:OKDBV

Oriola Oyj

Provides healthcare and wellbeing products primarily in Sweden and Finland.

Undervalued with excellent balance sheet.

Market Insights

Community Narratives