Fellow Finance Oyj (HEL:FELLOW) Consensus Forecasts Have Become A Little Darker Since Its Latest Report

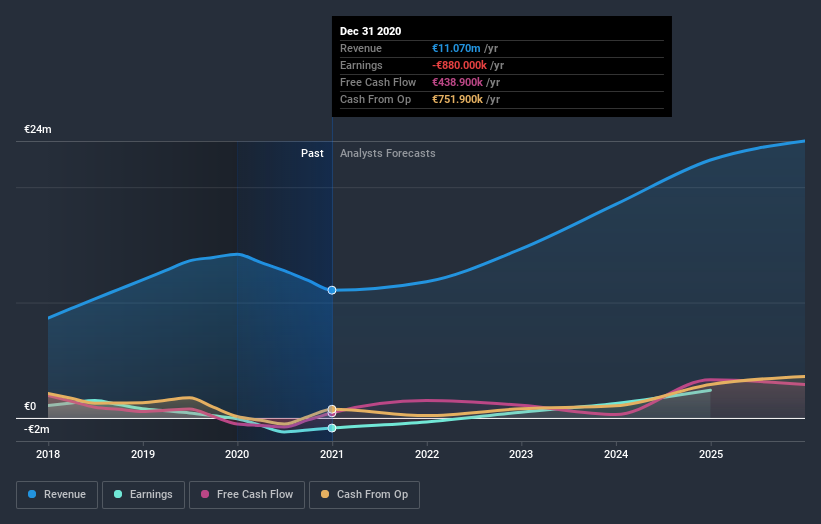

It's been a good week for Fellow Finance Oyj (HEL:FELLOW) shareholders, because the company has just released its latest full-year results, and the shares gained 5.6% to €2.84. The statutory results were mixed overall, with revenues of €11m in line with analyst forecasts, but losses of €0.12 per share, some 9.1% larger than the analysts were predicting. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Fellow Finance Oyj

Taking into account the latest results, the most recent consensus for Fellow Finance Oyj from twin analysts is for revenues of €11.8m in 2021 which, if met, would be a reasonable 6.6% increase on its sales over the past 12 months. Per-share statutory losses are expected to explode, reaching €0.05 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of €13.6m and earnings per share (EPS) of €0.015 in 2021. So we can see that the consensus has become notably more bearish on Fellow Finance Oyj's outlook following these results, with a substantial drop in next year's revenue estimates. Furthermore, they expect the business to be loss-making next year, compared to their previous calls for a profit.

The average price target was broadly unchanged at €3.00, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that Fellow Finance Oyj's revenue growth is expected to slow, with forecast 6.6% increase next year well below the historical 17%p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 18% per year. Factoring in the forecast slowdown in growth, it seems obvious that Fellow Finance Oyj is also expected to grow slower than other industry participants.

The Bottom Line

The biggest low-light for us was that the forecasts for Fellow Finance Oyj dropped from profits to a loss next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. The consensus price target held steady at €3.00, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have analyst estimates for Fellow Finance Oyj going out as far as 2025, and you can see them free on our platform here.

It is also worth noting that we have found 2 warning signs for Fellow Finance Oyj (1 doesn't sit too well with us!) that you need to take into consideration.

When trading Fellow Finance Oyj or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Alisa Pankki Oyj, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About HLSE:ALISA

Alisa Pankki Oyj

Provides various banking and financial services to personal and business consumers in Finland, Denmark, and Germany.

Moderate growth potential and slightly overvalued.

Market Insights

Community Narratives