Advertisement

- Finland

- /

- Capital Markets

- /

- HLSE:ALEX

Results: Alexandria Group Oyj Exceeded Expectations And The Consensus Has Updated Its Estimates

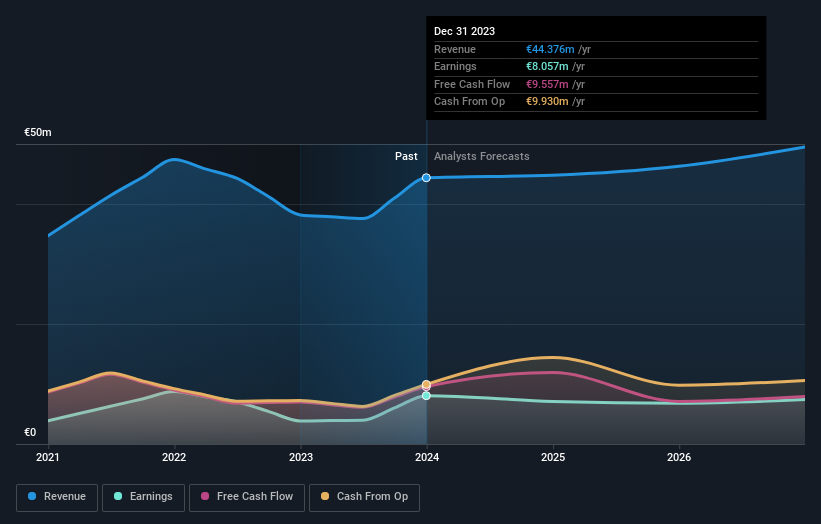

Alexandria Group Oyj (HEL:ALEX) just released its latest full-year results and things are looking bullish. Alexandria Group Oyj delivered a significant beat to revenue and earnings per share (EPS) expectations, hitting €44m-10% above indicated-and€0.77-45% above forecasts- respectively Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analyst has changed their mind on Alexandria Group Oyj after the latest results.

Check out our latest analysis for Alexandria Group Oyj

Following last week's earnings report, Alexandria Group Oyj's one analyst are forecasting 2024 revenues to be €44.8m, approximately in line with the last 12 months. Yet prior to the latest earnings, the analyst had been anticipated revenues of €44.6m and earnings per share (EPS) of €0.56 in 2024. Overall, while the analyst has reconfirmed their revenue estimates, the consensus now no longer provides an EPS estimate. This implies that the market believes revenue is more important after these latest results.

There's been no real change to the consensus price target of €7.00, with Alexandria Group Oyj seemingly executing in line with expectations.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Alexandria Group Oyj's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 1.0% growth on an annualised basis. This is compared to a historical growth rate of 6.0% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 6.7% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Alexandria Group Oyj.

The Bottom Line

The most important thing to take away is that the analyst reconfirmed their revenue estimates for next year, suggesting that the business is performing in line with expectations. Fortunately, the analyst also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Alexandria Group Oyj's revenue is expected to perform worse than the wider industry. The consensus price target held steady at €7.00, with the latest estimates not enough to have an impact on their price target.

One Alexandria Group Oyj broker/analyst has provided estimates out to 2026, which can be seen for free on our platform here.

Even so, be aware that Alexandria Group Oyj is showing 3 warning signs in our investment analysis , and 1 of those is potentially serious...

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:ALEX

Alexandria Group Oyj

Provides investment and saving solutions in Finland.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|24.5% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|24.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|97.7% undervalued

RO

Community Contributor