- Spain

- /

- Electric Utilities

- /

- BME:RED

We Think Red Eléctrica Corporación (BME:REE) Can Stay On Top Of Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Red Eléctrica Corporación, S.A. (BME:REE) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Red Eléctrica Corporación

How Much Debt Does Red Eléctrica Corporación Carry?

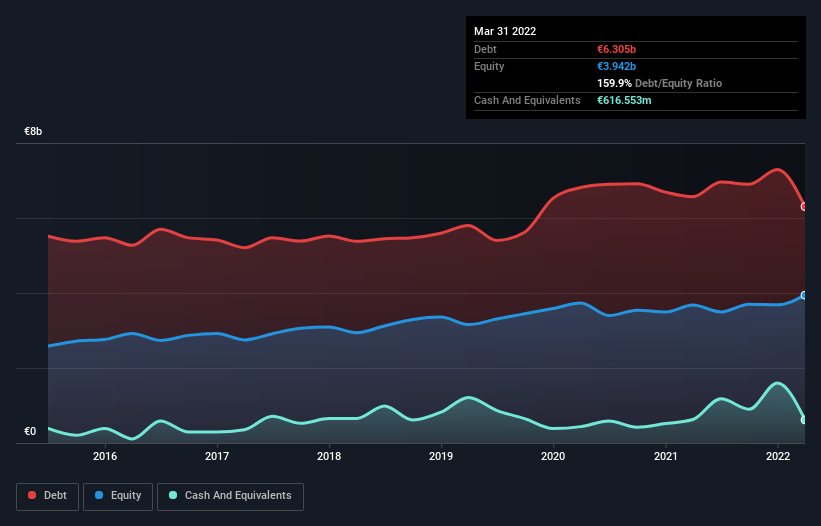

The image below, which you can click on for greater detail, shows that Red Eléctrica Corporación had debt of €6.30b at the end of March 2022, a reduction from €6.57b over a year. On the flip side, it has €616.6m in cash leading to net debt of about €5.69b.

How Strong Is Red Eléctrica Corporación's Balance Sheet?

According to the last reported balance sheet, Red Eléctrica Corporación had liabilities of €1.88b due within 12 months, and liabilities of €7.39b due beyond 12 months. Offsetting these obligations, it had cash of €616.6m as well as receivables valued at €1.41b due within 12 months. So it has liabilities totalling €7.24b more than its cash and near-term receivables, combined.

This is a mountain of leverage even relative to its gargantuan market capitalization of €10.3b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Red Eléctrica Corporación has net debt to EBITDA of 3.9 suggesting it uses a fair bit of leverage to boost returns. But the high interest coverage of 9.2 suggests it can easily service that debt. Sadly, Red Eléctrica Corporación's EBIT actually dropped 3.2% in the last year. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Red Eléctrica Corporación's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Red Eléctrica Corporación recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On our analysis Red Eléctrica Corporación's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For example, its net debt to EBITDA makes us a little nervous about its debt. We would also note that Electric Utilities industry companies like Red Eléctrica Corporación commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Red Eléctrica Corporación's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Red Eléctrica Corporación (1 is significant!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:RED

Redeia Corporación

Engages in the electricity transmission, and system operation and management of the transmission network for the electricity system in Spain and internationally.

Excellent balance sheet average dividend payer.