- Spain

- /

- Electric Utilities

- /

- BME:ELE

Why You Might Be Interested In Endesa, S.A. (BME:ELE) For Its Upcoming Dividend

It looks like Endesa, S.A. (BME:ELE) is about to go ex-dividend in the next four days. The ex-dividend date generally occurs two days before the record date, which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. In other words, investors can purchase Endesa's shares before the 27th of June in order to be eligible for the dividend, which will be paid on the 1st of July.

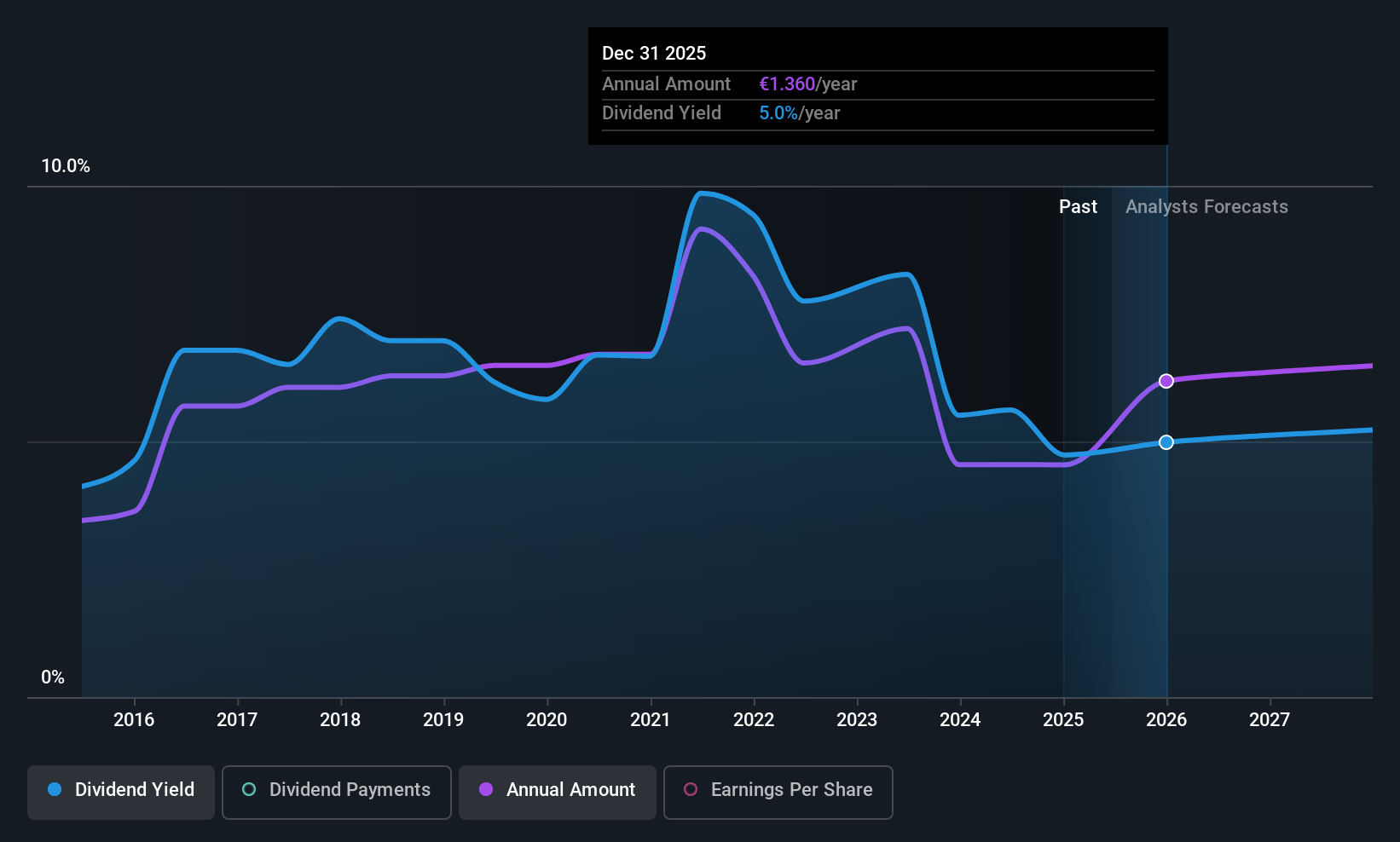

The company's next dividend payment will be €0.662337 per share, and in the last 12 months, the company paid a total of €1.32 per share. Based on the last year's worth of payments, Endesa stock has a trailing yield of around 4.8% on the current share price of €27.29. If you buy this business for its dividend, you should have an idea of whether Endesa's dividend is reliable and sustainable. As a result, readers should always check whether Endesa has been able to grow its dividends, or if the dividend might be cut.

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Endesa paid out more than half (64%) of its earnings last year, which is a regular payout ratio for most companies. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Fortunately, it paid out only 38% of its free cash flow in the past year.

It's positive to see that Endesa's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Check out our latest analysis for Endesa

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. It's encouraging to see Endesa has grown its earnings rapidly, up 66% a year for the past five years. The current payout ratio suggests a good balance between rewarding shareholders with dividends, and reinvesting in growth. Earnings per share have been growing quickly and in combination with some reinvestment and a middling payout ratio, the stock may have decent dividend prospects going forwards.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past 10 years, Endesa has increased its dividend at approximately 5.6% a year on average. It's good to see both earnings and the dividend have improved - although the former has been rising much quicker than the latter, possibly due to the company reinvesting more of its profits in growth.

Final Takeaway

Is Endesa an attractive dividend stock, or better left on the shelf? We like Endesa's growing earnings per share and the fact that - while its payout ratio is around average - it paid out a lower percentage of its cash flow. It's a promising combination that should mark this company worthy of closer attention.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. For instance, we've identified 3 warning signs for Endesa (1 is a bit unpleasant) you should be aware of.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Endesa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:ELE

Endesa

Engages in the generation, distribution, and sale of electricity in Spain, Portugal, France, Germany, the United Kingdom, Switzerland, Luxembourg, the Netherlands, Singapore, Italy, Morocco, and internationally.

Solid track record average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)