Unfortunately for shareholders, when Urbas Grupo Financiero, S.A. (BME:UBS) reported results for the period to December 2020, its auditors, Baker Tilly, expressed uncertainty about whether it can continue as a going concern. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

Given its situation, it may not be in a good position to raise capital on favorable terms. So current risks on the balance sheet could have a big impact on how shareholders fare from here. The biggest concern we would have is the company's debt, since its lenders might force the company into administration if it cannot repay them.

See our latest analysis for Urbas Grupo Financiero

How Much Debt Does Urbas Grupo Financiero Carry?

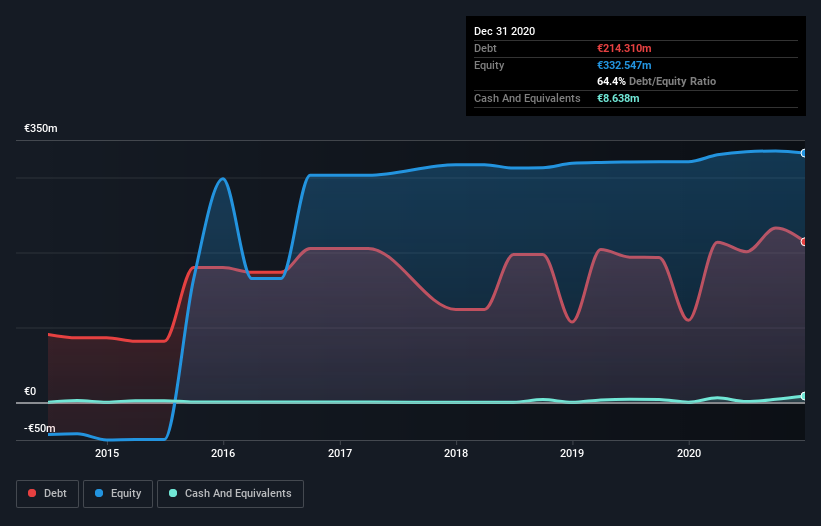

The image below, which you can click on for greater detail, shows that at December 2020 Urbas Grupo Financiero had debt of €214.3m, up from €109.5m in one year. However, because it has a cash reserve of €8.64m, its net debt is less, at about €205.7m.

A Look At Urbas Grupo Financiero's Liabilities

The latest balance sheet data shows that Urbas Grupo Financiero had liabilities of €236.3m due within a year, and liabilities of €41.5m falling due after that. Offsetting these obligations, it had cash of €8.64m as well as receivables valued at €26.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €242.3m.

This deficit isn't so bad because Urbas Grupo Financiero is worth €609.7m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Urbas Grupo Financiero will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Urbas Grupo Financiero wasn't profitable at an EBIT level, but managed to grow its revenue by 260%, to €22m. That's virtually the hole-in-one of revenue growth!

Caveat Emptor

While we can certainly appreciate Urbas Grupo Financiero's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at €5.3m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled €26m in negative free cash flow over the last twelve months. So suffice it to say we do consider the stock to be risky. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because companies should always make sure the auditor has confidence that the company will continue as a going concern, in our view. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 4 warning signs with Urbas Grupo Financiero (at least 2 which don't sit too well with us) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Urbas Grupo Financiero, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BME:UBS

Urbas Grupo Financiero

Engages in the real estate business in Spain, Portugal, Algeria, and Latin America.

Adequate balance sheet low.

Market Insights

Community Narratives