Advertisement

Assessing Bankinter (BME:BKT) Valuation After Strong Multi‑Year Shareholder Returns

Assessing Bankinter after recent share performance

Bankinter (BME:BKT) has drawn fresh attention after recent share price moves, prompting investors to reassess how its current valuation lines up with reported profitability and the bank’s role across Spain and selected European markets.

See our latest analysis for Bankinter.

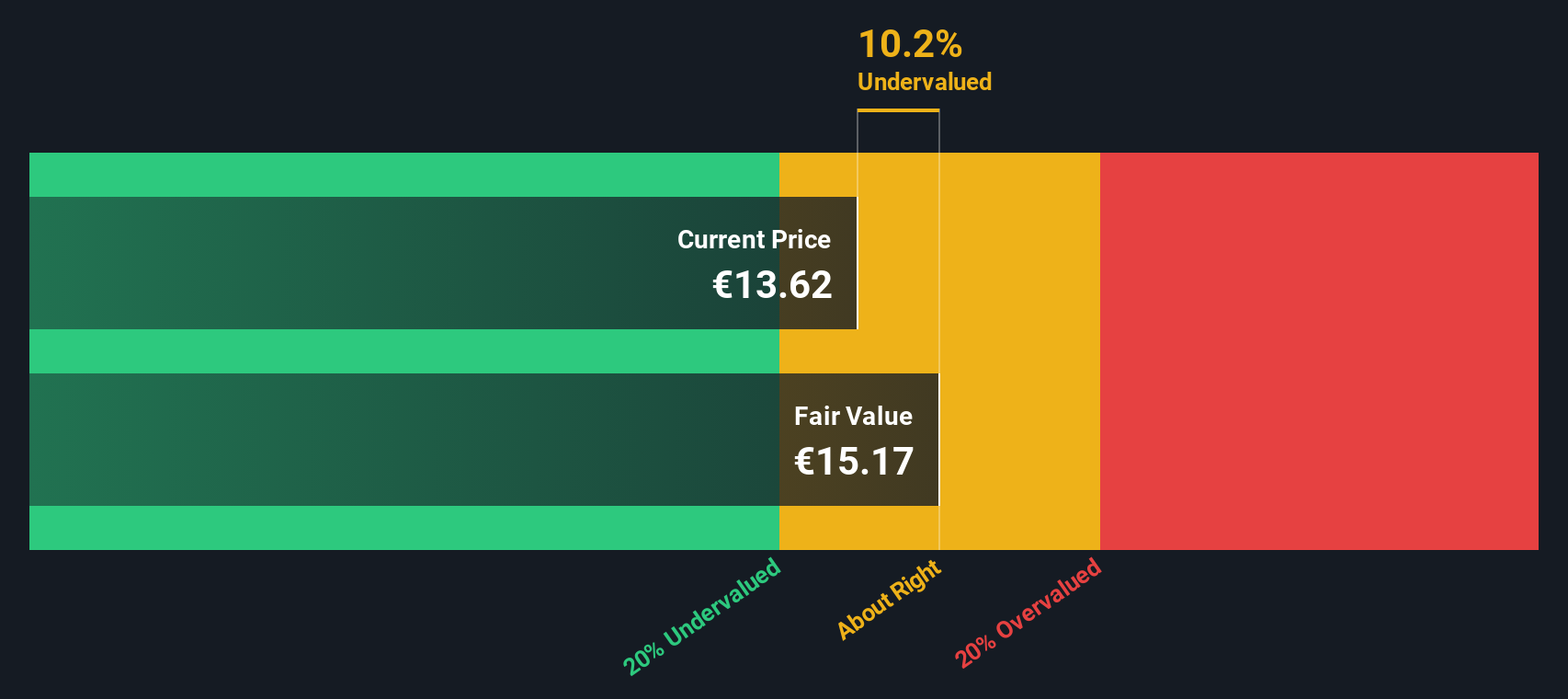

At a share price of €14.21, Bankinter’s recent share price return has been mixed in the short term, with a slight 1-day decline set against an 8.93% 90-day gain. Its 1-year total shareholder return of 79.81% and very large 5-year total shareholder return suggest that momentum has been building over time as investors reassess growth potential and risk around the bank’s earnings profile.

If Bankinter’s long run performance has caught your eye, it can be useful to see what else is out there, including fast growing stocks with high insider ownership that might sit on your research list next.

So with Bankinter trading around €14.21, an intrinsic discount screen suggesting roughly 28% upside, and a modest premium to the latest analyst target, you have to ask: is there a genuine opportunity here, or is the market already baking in future growth?

Most Popular Narrative: 2.1% Overvalued

With Bankinter closing at €14.21 against a narrative fair value of €13.92, the current price sits slightly above that widely followed estimate, which leans on detailed assumptions about growth, profitability and required returns.

Recent research suggests a broadly constructive backdrop around Bankinter, with several firms adjusting their price targets higher and one major house upgrading its stance on the shares. Here is how the Street commentary broadly lines up for you as an investor.

Curious what is supporting that fair value so close to today’s price? The narrative focuses on measured revenue growth, firm profit margins and a higher future earnings multiple. Want to see which specific earnings and valuation assumptions sit under that €13.92 figure, and how they tie together over the next few years?

Result: Fair Value of €13.92 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value story can break if Spain stumbles or regulation tightens, which could hit loan quality, capital needs and the earnings path analysts are assuming.

Find out about the key risks to this Bankinter narrative.

Another Angle: SWS DCF Points to Upside

While the narrative fair value of €13.92 frames Bankinter as slightly overvalued at €14.21, our DCF model paints a different picture, with a fair value estimate of €19.68 and a 27.8% discount. These are two valuation tools with two very different messages, so which one do you lean toward?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bankinter for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bankinter Narrative

If you look at these numbers and reach a different conclusion, or just prefer to test your own assumptions, you can build a custom view in under three minutes with Do it your way.

A great starting point for your Bankinter research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for your next investment idea?

If Bankinter is on your radar, do not stop there, widen your watchlist with a few focused stock ideas that could sharpen your overall portfolio thinking.

- Spot potential bargains with these 870 undervalued stocks based on cash flows that line up current prices against underlying cash flows so you can focus on ideas that may merit a closer look.

- Scan these 24 AI penny stocks for businesses that are tying their growth stories to artificial intelligence use cases.

- Explore income opportunities through these 12 dividend stocks with yields > 3% and quickly see which companies offer yields above 3% to support a steady return profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bankinter might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BME:BKT

Bankinter

Provides various banking products and services to individuals, corporates, and small- and medium-sized enterprises in Spain, Luxembourg, Portugal, and Ireland.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7063.2% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.5% undervalued

46 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15121.8% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Investigator Silver ·

Investigator Silver, Leverage Exposed: $1/oz Move = $42M Cash for This ASX Developer

Fair Value:AU$2.3997.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.5% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3239.7% undervalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.3% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1929.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative